Things can go sour in life, but there's often a way to make those situations better. That's why insurance upstart Lemonade (NYSE: LMND) chose its quirky name.

Lemonade shareholders should be feeling a bit sweeter these days. After three quarters of ups and downs, the stock is now up 180% year to date as we get close to the end of 2024. However, it's still 74% off of its all-time highs. Here's what's happening now, and how to think about this growth stock going into the new year.

No more sour lemons

Lemonade electrified the market when it went public in July 2020 -- but many other tech stocks did too during that period's bull market. Valuations went through the roof in the excitement, Lemonade's along with them. Then came the 2022 tech slump, and the stock was quickly and deeply humbled, falling by more than 90% from its peak. Since then, the stock has plodded along, largely moving sideways. But recently, its business has displayed incredible momentum, and that has translated into fantastic share price gains.

The market's new enthusiasm stems from Lemonade's improving loss ratio and profitability. For years, the company has touted its artificial intelligence (AI) and machine learning algorithms, claiming that its system gave it significant advantages over legacy insurers. But as it produced unexceptional results and mounting losses, that was starting to look like wishful thinking. Now, it's finally beginning to deliver on the hype.

It's still reporting robust growth, with in-force premiums up 24% year over year in the third quarter, and a 17% increase in customer count. But its loss ratio went down by 10 percentage points to 73% -- a level within Lemonade's target long-term range. It also generated $16 million in cash from operations and $48 million in net cash flow.

Stocks tend to move based on quarterly reports, but something Lemonade noted in the latest report was that its trailing-12-month loss ratio was 77%, down 11 percentage points, and it was the fifth consecutive decrease in the trailing-12-month figure. That's a more telling metric, signaling that the quarterly improvement was not a fluke.

However, loss ratios are down for the entire industry as inflation eases, and Lemonade's loss ratio movement is still something for investors to keep an eye on.

Sweetening the deal

Lemonade just had its first investor meeting in two years, and while there were many highlights, the most exciting part was that management is expecting to 10x its business, boosting its in force premiums to $10 billion, in the same amount of time it took to reach $1 billion -- about 10 years.

It made a compelling argument. The company noted that insurance is one of the biggest industries there is, and disrupters have a meaningful shot at becoming its new leaders. Since the industry is dominated by centuries-old companies, Lemonade -- built around new digital systems -- has a structural advantage. From the beginning, it maintained that it would take time for its platform to get enough data and perform enough modeling to start demonstrating superior results. The company is just getting into that phase, and as its revenue growth exceeds its expenses, it expects to become not just profitable, but massively profitable.

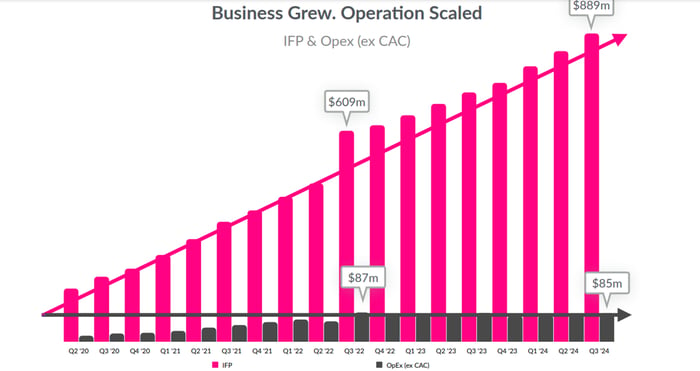

This chart offers investors a sense of how this is playing out. IFP is the average total premium in-force in a given period of time, Opex refers to operating expense, and CAC is customer-acquisition costs.

Image source: Lemonade.

Lemonade has kept headcount flat even as it achieved steady growth. That's because it relies on technology to do the heavy lifting. But this chart is focused on fixed expenses and leaves out Lemonade's biggest expense, CAC. Lemonade will reach a level of scale when sales outdo expenses, including CAC. Management is expecting growth to accelerate over the next two years and for the company to report positive net income in 2027.

The stock's recent jump already reflects the improved performance and confidence in the future. But if one tries to peer far into the future -- say, 20 years -- it's easy to imagine that Lemonade's platform could be completely outperforming the models of traditional insurance companies.

Is there more upside?

After a share price run-up like the one Lemonade has enjoyed in the past few months, investors might be worried that there's not much more upside potential. No one can know what will happen in the near term, but the long-term opportunity looks very exciting.

Lemonade's valuation might still be called reasonable. It's not a regular insurance company because it has the tech element and it's a growth stock, and it's not profitable, so it's not easy to value. It trades at 5.5 book value, which is in line with some other insurance companies, although price-to-book value has soared along with Lemonade's price.

It's trading at 6 times trailing-12-month sales, which isn't objectively cheap, but it's nowhere near the astronomical ratios of more than 50 that it traded at back at the stock's peak.

Don't expect linear upward movement from this stock, but if you have some appetite for risk and a long-term investing horizon, Lemonade should be on your buy list.

Should you invest $1,000 in Lemonade right now?

Before you buy stock in Lemonade, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Lemonade wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $872,947!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of December 2, 2024

Jennifer Saibil has positions in Lemonade. The Motley Fool has positions in and recommends Lemonade. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.