Wolverine World Wide, Inc. WWW is trading at a notable low price-to-earnings (P/E) multiple, which is below the Zacks Shoes and Retail Apparel industry and the broader Consumer Discretionary sector’s averages. WWW's forward 12-month P/E ratio is 13.64, lower than the industry's and the sector’s ratios of 26.53 and 18.93, respectively.

This stock is undervalued than its industry peers, offering compelling value to investors looking for exposure to the sector. WWW's Value Score of A underscores its appeal as an investment option.

Image Source: Zacks Investment Research

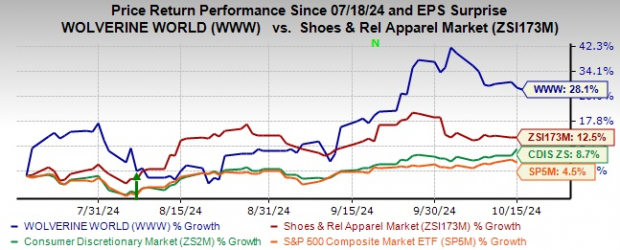

Shares of the company have seen a decent price increase over the past three months, climbing 28.1% and surpassing the industry’s 12.5% growth. This resulted from its enhanced operational efficiency and product initiatives, which have also helped it outperform the sector and the S&P 500 index’s respective growth of 8.7% and 4.5% in the same period.

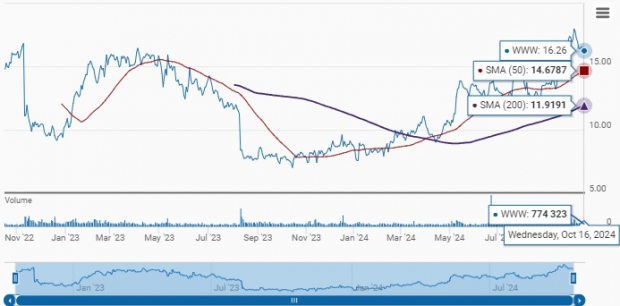

WWW closed yesterday’s trading session at $16.26, which is 12.2% below its 52-week high of $18.51 attained on Oct. 4, 2024. WWW is currently trading above its 200-day simple moving average (SMA) of $11.92 and 50-day SMA of $14.68. This technical strength, coupled with continued momentum, signals positive market sentiment and increasing investor confidence in WWW's financial health and growth potential.

Image Source: Zacks Investment Research

Investments Boost Wolverine’s Growth & Stability

Wolverine has made substantial investments in demand generation, especially in marketing and advertising, which have significantly boosted brand visibility, enhanced customer loyalty and driven sales growth. The company’s emphasis on delivering innovative, trend-oriented products has resonated well with consumers, demonstrating its commitment to remaining relevant in the marketplace.

Saucony, one of Wolverine's leading brands, exemplifies the effectiveness of this strategy with product launches like the Triumph 22 and Hurricane 24, both of which have seen strong consumer demand.

In the second quarter of 2024, Saucony's revenue contribution rose year over year by 900 basis points, with e-commerce sales achieving more than 20% growth. Other brands, such as Merrell and Sweaty Betty, have solidified their market positions through product enhancements and targeted consumer engagement.

Wolverine has also made considerable strides in reducing its debt, resulting in a healthier balance sheet. By the end of the second quarter, the company's net debt stood at $666 million, reflecting a $270-million decrease from the previous year. This proactive debt-reduction strategy enhances the company's financial flexibility and supports investments in growth initiatives.

In the second quarter, Wolverine recorded a 400-basis-point increase in the adjusted gross margin to 43.1%. This improvement highlights the company’s robust profitability, driven by effective cost management, efficient inventory control and targeted pricing strategies, reinforcing its path toward long-term financial stability.

Image Source: Zacks Investment Research

WWW's Optimistic Outlook for 2024

Wolverine is well-positioned for significant growth in 2024, leveraging its strong market presence to boost profitability. The company anticipates a notable increase in its gross margin, projecting an adjusted figure of 44.5% at the mid-point, indicating a year-over-year rise of 460 basis points.

Adjusted selling and general administrative expenses are expected to decline to $640 million, or 37.5% of sales, implying a decline from the $716 million reported in 2023. The adjusted operating margin is also projected to improve to 7.4%, suggesting a 350-basis-point year-over-year increase.

For the third quarter, Wolverine forecasts a gross margin of 45%, indicating a 300-basis-point year-over-year rise. The company expects an adjusted operating margin of 7% and adjusted earnings per share of 20 cents for the third quarter.

Overall, adjusted earnings per share for the year are projected between 75 cents and 85 cents, an increase from the prior mentioned 65-85 cents, despite an anticipated 10-cent negative impact of foreign exchange fluctuations. Wolverine reported adjusted earnings of 5 cents per share in 2023.

Soft Consumer Demand Poses Challenges for Wolverine

WWW acknowledges the tough macroeconomic environment, which continues to exert pressure on consumer demand. The company is concerned about economic challenges and changing spending patterns, leading to revenue declines across most divisions and brands.

In the second quarter, total revenues fell 27.8% year over year to $425.2 million. Revenues from the Active Group dropped 20.2%, the Work Group declined 10.9% and the Other segment decreased 83.8%. Merrell's revenues fell 19.2%, Saucony's declined 28% and Wolverine's slipped 3.1%. The international business also saw a 19.3% decline.

Direct-to-consumer (DTC) revenues decreased 14.4% year over year as Wolverine continues to navigate a challenging global wholesale and DTC environment. Management forecasts a 13.2-14.2% revenue decline for 2024 to $1.71-$1.73 billion. It expects third-quarter revenues to decrease 11% year over year to $420 million.

Conclusion

Investors may find the WWW stock more attractive due to its undervaluation than industry peers, as reflected in its low P/E multiple. The company has shown operational improvements, with share prices recently outperforming its industry and the broader market. Its focus on effective marketing and innovative product launches, especially from its Saucony brand, has enhanced brand visibility and consumer loyalty.

Proactive debt reduction has strengthened Wolverine's balance sheet, allowing for greater financial flexibility. Despite these tailwinds, challenges related to soft consumer demand cannot be overlooked. Current investors may choose to remain invested but potential investors should be cautious about being drawn to this Zacks Rank #3 (Hold) stock's low valuation.

Stocks to Consider

Some better-ranked stocks are Abercrombie & Fitch Co. ANF, Steven Madden, Ltd. SHOO and Crocs, Inc. CROX.

Abercrombie is a specialty retailer of premium, high-quality casual apparel. It sports a Zacks Rank of 1 (Strong Buy) at present. ANF delivered a 16.8% earnings surprise in the last reported quarter. You can see the complete list of today’s Zacks #1 Rank stocks here.

The consensus estimate for Abercrombie’s fiscal 2025 earnings and sales indicates growth of 63.4% and 13%, respectively, from the fiscal 2024 reported levels. ANF has a trailing four-quarter average earnings surprise of 28%.

Steven Madden designs, sources, markets and sells fashion-forward name-brand and private-label footwear. It currently has a Zacks Rank of 2 (Buy).

The Zacks Consensus Estimate for Steven Madden’s 2024 earnings and sales indicates growth of 6.9% and 12.7%, respectively, from the 2023 reported levels. SHOO has a trailing four-quarter average earnings surprise of 9.5%.

Crocs offers a wide variety of footwear products, including sandals, wedges, flips and slides that cater to people of all ages. The company currently carries a Zacks Rank #2.

The Zacks Consensus Estimate for Crocs’ 2024 earnings and sales indicates growth of 7.1% and 4.2%, respectively, from the 2023 actuals. CROX has a trailing four-quarter average earnings surprise of 14.9%.

Only $1 to See All Zacks' Buys and Sells

We're not kidding.

Several years ago, we shocked our members by offering them 30-day access to all our picks for the total sum of only $1. No obligation to spend another cent.

Thousands have taken advantage of this opportunity. Thousands did not - they thought there must be a catch. Yes, we do have a reason. We want you to get acquainted with our portfolio services like Surprise Trader, Stocks Under $10, Technology Innovators,and more, that closed 228 positions with double- and triple-digit gains in 2023 alone.

See Stocks Now >>Abercrombie & Fitch Company (ANF) : Free Stock Analysis Report

Wolverine World Wide, Inc. (WWW) : Free Stock Analysis Report

Crocs, Inc. (CROX) : Free Stock Analysis Report

Steven Madden, Ltd. (SHOO) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.