Sometimes you just have to call it like you see it: 2024 was a terrible year for W.P. Carey (NYSE: WPC). But it's important to understand what that bad year was really about. For this real estate investment trust (REIT), it was about setting the stage for a brighter future. Indeed, that bad 2024 should make you want to buy W.P. Carey stock even more.

Getting off on the wrong foot at W.P. Carey

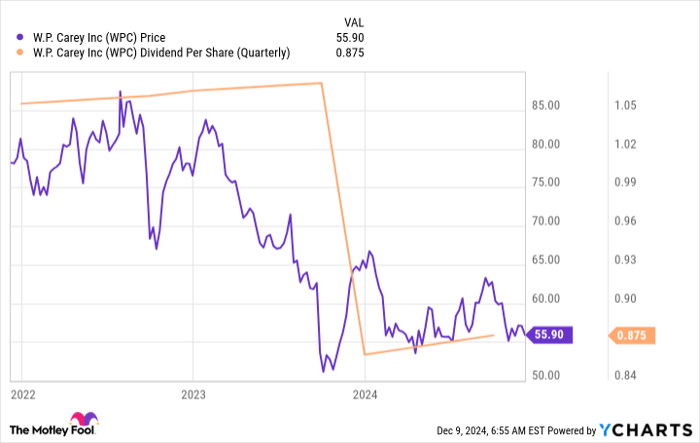

Essentially, the first thing that greeted W.P. Carey investors in 2024 was a dividend cut. Not only that, but the cut occurred after 24 consecutive annual dividend increases. So, just on the cusp of the REIT reaching a major milestone, management and the board chose to trim the dividend. That's not a good look but there's more to understand here.

Image source: Getty Images.

One of the biggest things is that management started hiking the payout again in the quarter after the cut. Further, it kept boosting it in every subsequent quarter, which is the same cadence for increases that the company had followed before the cut. That makes the dividend cut look more like a dividend reset, which is really what it was. But why reset the dividend lower?

At the end of 2023, W.P. Carey made the dramatic decision to exit the office sector. It had been slowly reducing its exposure to that property type, but the office real estate market was increasingly troubled and management came to the conclusion that it would be best to simply sell the remaining properties fast. Before this decision, office properties provided 16% of W.P. Carey's rents. That's simply too much income to lose without resetting the dividend.

What comes next for W.P. Carey

W.P. Carey's move out of the office segment was a calculated strategic shift that removed a troubled property type from its portfolio. So, despite the dividend cut, this REIT is in a stronger position today than it was a year or so ago. Wall Street, however, is still wary, so its dividend yield remains elevated at 6.2%. The S&P 500 index (SNPINDEX: ^GSPC) is yielding just 1.2% while the average REIT is yielding about 3.7%, using the Vanguard Real Estate Index ETF (NYSEMKT: VNQ) as an industry proxy.

Investors are getting paid well to own W.P. Carey right now. But what are they getting? Jettisoning its office properties gave W.P. Carey cash that it can invest in new properties that will, in turn, spur growth. A lot has already been spent, but it is likely that management will still be spending that cash at least into 2025, since buying assets usually takes longer than selling them. And, more to the point, the benefit of new acquisitions won't show up all at once. The new rents only arrive as the new buildings get added to the portfolio over time.

So, during the next year or two (or perhaps even three), W.P. Carey will likely see a boost in income from reinvestment of the cash it accumulated via the office exit. That growth will strengthen the company's portfolio because it will be in property types that management believes have strong long-term appeal -- largely industrial and retail. In other words, in 2025, its growth will resume as 2024 acquisitions drive the rent roll higher. And in 2026, the REIT will likely see further growth benefits from acquisitions that it closes throughout 2025 using the liquidity created by the office exit.

Hold your nose and think long term

It was a bit of a shock to Wall Street when W.P. Carey announced its plans to rapidly exit the office rental segment. The dividend reset was hard for investors to swallow too -- and it's understandable that they felt let down. But the negative sentiment around W.P. Carey is fairly extreme right now, and likely overdone. If you're an investor who's thinking in decades and not days, you might want to buy this out-of-favor REIT before the results of its new property acquisitions start to shine through in 2025 and beyond.

Should you invest $1,000 in W.P. Carey right now?

Before you buy stock in W.P. Carey, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and W.P. Carey wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $827,780!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of December 9, 2024

Reuben Gregg Brewer has positions in W.P. Carey. The Motley Fool has positions in and recommends Vanguard Real Estate ETF. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.