Per a Bloomberg report, Qualcomm Incorporated’s QCOM modems are likely to be replaced in the upcoming iPhone models as Apple Inc. AAPL is in the final stages of developing an in-house modem. Although representatives of both companies have declined to comment on the grapevines, the buzz has cast a shadow on Qualcomm’s future revenue-generating opportunities.

A modem functions as an integral part of smartphones and laptops, enabling seamless Internet connectivity within the devices. Qualcomm modems have been a key feature in iPhone models, connecting the device to cellular networks for fast web browsing and instant app access. Built on indigenous technology that requires specialized engineering expertise and broad industry know-how, these modems have been the hallmark of impeccable performance standards.

Apple acquired Intel Corporation’s INTC modem business in 2019 to gain a foothold in this highly technical domain. This helped the iPhone manufacturer to gradually develop a core team of skilled technicians to sow the seeds of its own cellular modems. Despite several hiccups during the various stages of product development, Apple is reportedly set to introduce its in-house modem very soon.

Will This Hurt QCOM Stock?

The news has raised questions about an earlier patent truce agreement between the two parties. Drawing curtains to prolonged patent litigations, the former allies turned antagonists decided to call a truce in April 2019, with Apple paying an undisclosed amount to Qualcomm. The agreement also included a six-year license agreement effective April 1, 2019, along with a two-year extension option and a multi-year chipset supply agreement.

Consequently, Apple licensed the chips directly from Qualcomm instead of relying on original equipment manufacturers (OEMs) to do it on its behalf, generating recurring payments to the tune of 20% of QCOM’s total revenues.

Qualcomm had long been preparing for this divorce by focusing on a diversified revenue stream. The company is well-positioned to meet its long-term revenue targets driven by solid 5G traction and greater visibility. Qualcomm is increasingly focusing on the seamless transition from a wireless communications firm for the mobile industry to a connected processor company for the intelligent edge. This is likely to expand its total addressable market to approximately $900 billion by 2030.

Qualcomm is witnessing healthy traction in EDGE networking, which helps transform connectivity in cars, business enterprises, homes, smart factories, next-generation PCs, wearables and tablets. The company intends to harness artificial intelligence (AI) to meet increased demands for essential products and services that are the building blocks of digital transformation in a cloud economy.

With the accelerated rollout of 5G technology, Qualcomm is benefiting from investments toward building a licensing program in mobile. In addition, the chip manufacturer envisions solid growth opportunities within the mobile space, driven by the strength of its Snapdragon portfolio. As a result, QCOM stock appears to be relatively well-placed to weather the Apple storm.

QCOM Rides on Snapdragon, Automotive Businesses

Over the years, Qualcomm has witnessed a relatively healthy revenue growth curve. Leveraging processors with multi-core CPUs with cutting-edge features, amazing graphics and worldwide network connectivity, Qualcomm Snapdragon mobile platforms are fast and have superb power efficiency. Smartphones and mobile devices built with Snapdragon mobile platforms enable immersive augmented reality and virtual reality experiences, brilliant camera capabilities, superior 4G LTE and 5G connectivity with state-of-the-art security solutions.

The automotive telematics and connectivity platforms, digital cockpit and C-V2X solutions are fueling emerging automotive industry trends such as the growth of connected vehicles, the transformation of the in-car experience and vehicle electrification. Qualcomm believes it is on track to become the largest smartphone radio frequency front-end supplier by revenue in the near future.

Automotive revenues surged 68% to a record high of $899 million in fourth-quarter fiscal 2024, driven by increased content in new vehicle launches with its Snapdragon Digital Chassis platform. This was the 16th consecutive quarter in which Qualcomm recorded double-digit growth in automotive revenues. The company expects automotive revenues to increase to more than $4 billion in fiscal 2026.

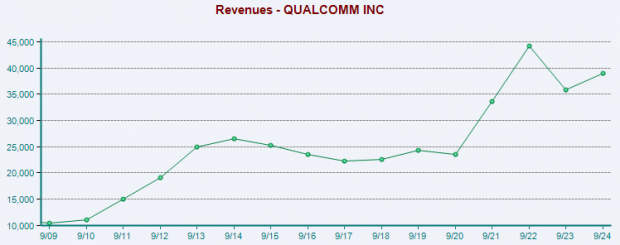

Image Source: Zacks Investment Research

Stock Price Performance of QCOM

Buoyed by a holistic growth model, QCOM shares have gained 14.4% over the past year compared with the wireless equipment industry’s growth of 33.8%, lagging peers like Hewlett Packard Enterprise Company HPE and Broadcom Inc. AVGO.

One-Year QCOM Stock Price Performance

Image Source: Zacks Investment Research

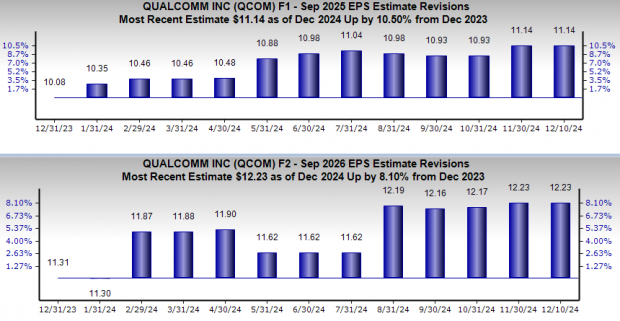

Earnings Estimate Revision Trend for QCOM

Earnings estimates for Qualcomm for fiscal 2024 have moved up 10.5% to $11.14 over the past year, while the same for fiscal 2025 has jumped 8.1% to $12.23. The positive estimate revision depicts bullish sentiments for the stock.

Image Source: Zacks Investment Research

End Note

With solid fundamentals and healthy revenue-generating potential driven by robust demand trends, Qualcomm appears to be a solid investment proposition. A strong emphasis on quality, diligent execution of operational plans and continuous portfolio enhancements are driving more value for customers. With improving earnings estimates, the stock is witnessing a positive investor perception. Although Qualcomm’s revenues will likely be hurt by Apple’s purported move to develop in-house modem, it has a diversified revenue stream to cushion from the apparent setback.

The stock delivered a trailing four-quarter average earnings surprise of 7.6%. It has a VGM Score of A. Qualcomm currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Riding on a robust earnings surprise history and favorable Zacks Rank, it appears primed for further price appreciation. Hence, investors are likely to profit if they bet on this high-flying stock now.

Only $1 to See All Zacks' Buys and Sells

We're not kidding.

Several years ago, we shocked our members by offering them 30-day access to all our picks for the total sum of only $1. No obligation to spend another cent.

Thousands have taken advantage of this opportunity. Thousands did not - they thought there must be a catch. Yes, we do have a reason. We want you to get acquainted with our portfolio services like Surprise Trader, Stocks Under $10, Technology Innovators,and more, that closed 228 positions with double- and triple-digit gains in 2023 alone.

See Stocks Now >>Intel Corporation (INTC) : Free Stock Analysis Report

QUALCOMM Incorporated (QCOM) : Free Stock Analysis Report

Apple Inc. (AAPL) : Free Stock Analysis Report

Broadcom Inc. (AVGO) : Free Stock Analysis Report

Hewlett Packard Enterprise Company (HPE) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.