Shares of Microsoft (NASDAQ: MSFT) have delivered steady gains of 41% in the past three years, edging the S&P 500 index's jump of 34% by a small margin, but the world's third-largest company by market cap has failed to gather any steam in 2024.

More specifically, Microsoft stock has delivered just 11% gains this year, underperforming the S&P 500 index by a big margin. The stock's underperformance may seem a tad surprising considering that it has been clocking healthy growth quarter after quarter. In this article, we will take a closer look at Microsoft's prospects for the next three years and check if the tech giant can overcome a disappointing 2024 to become a long-term winner.

AI has the potential to lift Microsoft's growth significantly

Microsoft's revenue in the recently concluded fiscal year 2024 (which ended on June 30) increased by 15% year over year in constant-currency terms to $245 billion. This healthy double-digit growth was driven by the growing demand for the company's Microsoft 365 office collaboration and productivity tools, an impressive jump in its Azure revenue, and a 9% jump in search and news-advertising revenue.

The Azure business was the cornerstone of Microsoft's growth in fiscal 2024. It recorded a 33% year-over-year increase in revenue from Azure and other cloud-services last year, of which nine percentage points were attributable to artificial intelligence (AI). It is worth noting that AI's contribution to Microsoft's Azure business increased throughout the year, jumping from five percentage points in the fiscal first quarter to 11 percentage points in fiscal Q4.

It is easy to see why Microsoft's Azure cloud service is getting a nice shot in the arm thanks to AI. After all, the demand for cloud-based AI services is growing at an incredible pace. Goldman Sachs estimates that the global cloud-computing market could generate $2 trillion in revenue by 2030 as compared to $496 billion in 2023. More importantly, generative AI is expected to account for 10% to 15% of global-cloud spending by the end of the decade.

Microsoft is already capitalizing on this lucrative trend by giving customers access to a big pool of large language models (LLMs) on its cloud platform with which they can develop and deploy AI models. As CEO Satya Nadella remarked on the July earnings-conference call:

With Azure AI, we are building out the app server for the AI wave providing access to the most diverse selection of models to meet customers' unique cost, latency, and design considerations. All up, we now have over 60,000 Azure AI customers up nearly 60% year over year and average spend per customer continues to grow.

Microsoft also points out that its models-as-a-service offering has also gained impressive traction, with the number of paid customers doubling quarter over quarter in fiscal Q4. The tech giant offers customers access to various kinds of models on rent so that they can develop and deploy AI applications. So, with the demand for AI services in the cloud set to grow substantially in the coming years, Microsoft should ideally witness further acceleration in its Azure revenue.

On the other hand, Microsoft's Office 365 business is also getting a nice lift thanks to AI. According to Nadella, "the number of people who use Copilot daily at work nearly doubled quarter over quarter" in fiscal Q4, with the number of customers using Copilot jumping 60% sequentially. Microsoft Copilot is a generative AI assistant that allows users to "complete tasks faster, hold more effective meetings and automate business workflows and processes."

Again, this could be a potentially lucrative market for Microsoft as the market for AI-powered productivity tools is expected to grow at an annual rate of almost 27% through the end of the decade, according to Grand View Research. The size of the market was worth an estimated $6.9 billion last year, but it could hit $36 billion in annual revenue by the end of the decade.

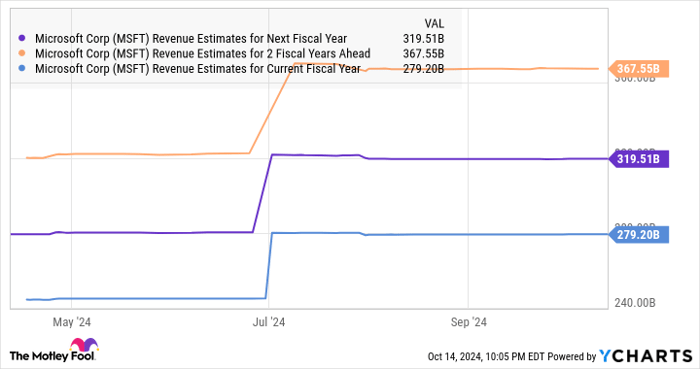

In all, the emergence of new growth opportunities for Microsoft thanks to AI should ideally help the company sustain its healthy levels of growth over the next three years. This is precisely what consensus estimates suggest, as the chart below shows.

MSFT Revenue Estimates for Next Fiscal Year data by YCharts.

Stronger earnings growth could send the stock on a nice bull run

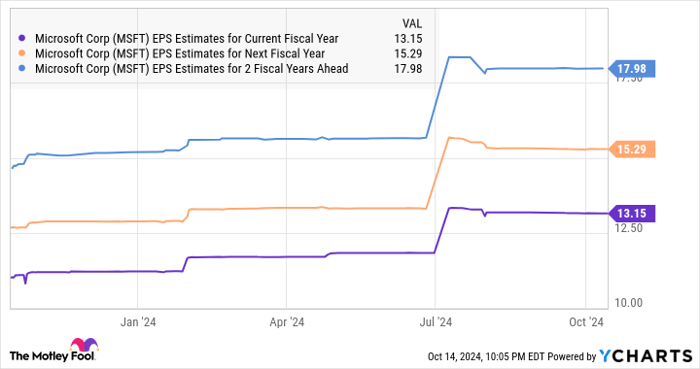

Microsoft reported a 20% year-over-year jump in non-GAAP earnings in fiscal 2024 to $11.80 per share. Though analysts are forecasting a smaller jump in the current fiscal year, Microsoft's earnings growth is expected to pick up pace in fiscal years 2026 and 2027.

MSFT EPS Estimates for Current Fiscal Year data by YCharts.

The smaller increase in Microsoft's fiscal 2025 earnings can be attributed to the company's aggressive capital spending. Last year, Microsoft's capital expenditure jumped 75% from the preceding year to $55.7 billion, and it is on track to increase its capex once again in fiscal 2025 thanks to its focus on building out its cloud and AI infrastructure.

While the elevated levels of spending will weigh on Microsoft's bottom-line growth in the short run, the company believes that it should help it monetize the growing demand for AI over the next 15 years and longer. That's why investors would do well to look at the bigger picture.

Moreover, it's clear that Microsoft's earnings growth is forecasted to accelerate over the next couple of years. Assuming its earnings indeed jump to $17.98 per share in fiscal 2027 and it trades at 30 times earnings at that time -- in line with the Nasdaq-100 index's price-to-earnings ratio -- its stock price could hit $540. That would represent a 29% jump from current levels.

However, if Microsoft is able to achieve stronger levels of growth and the market decides to reward it with a higher-earnings multiple, it could deliver stronger gains over the next three years. So, investors would do well to add this tech giant to their portfolios even though it has underperformed so far in 2024 as its AI-fueled growth could help it step on the gas.

Should you invest $1,000 in Microsoft right now?

Before you buy stock in Microsoft, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Microsoft wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $839,122!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of October 14, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Goldman Sachs Group and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.