The average credit card interest rate is 24.10%, according to Forbes Advisor’s weekly credit card rates report.

The Federal Reserve keeps tabs on the average interest rate that U.S. consumers pay for a variety of different financial products—credit cards included. In November 2022, the average credit card interest rate in the U.S. on accounts with balances that assessed interest was 20.40%, according to The Federal Reserve.

Of course, the annual percentage rates (APR) you pay on your own credit cards might not match up with the national average. Credit card APRs can vary widely based on a number of factors, from your credit score to your debt-to-income ratio and beyond.

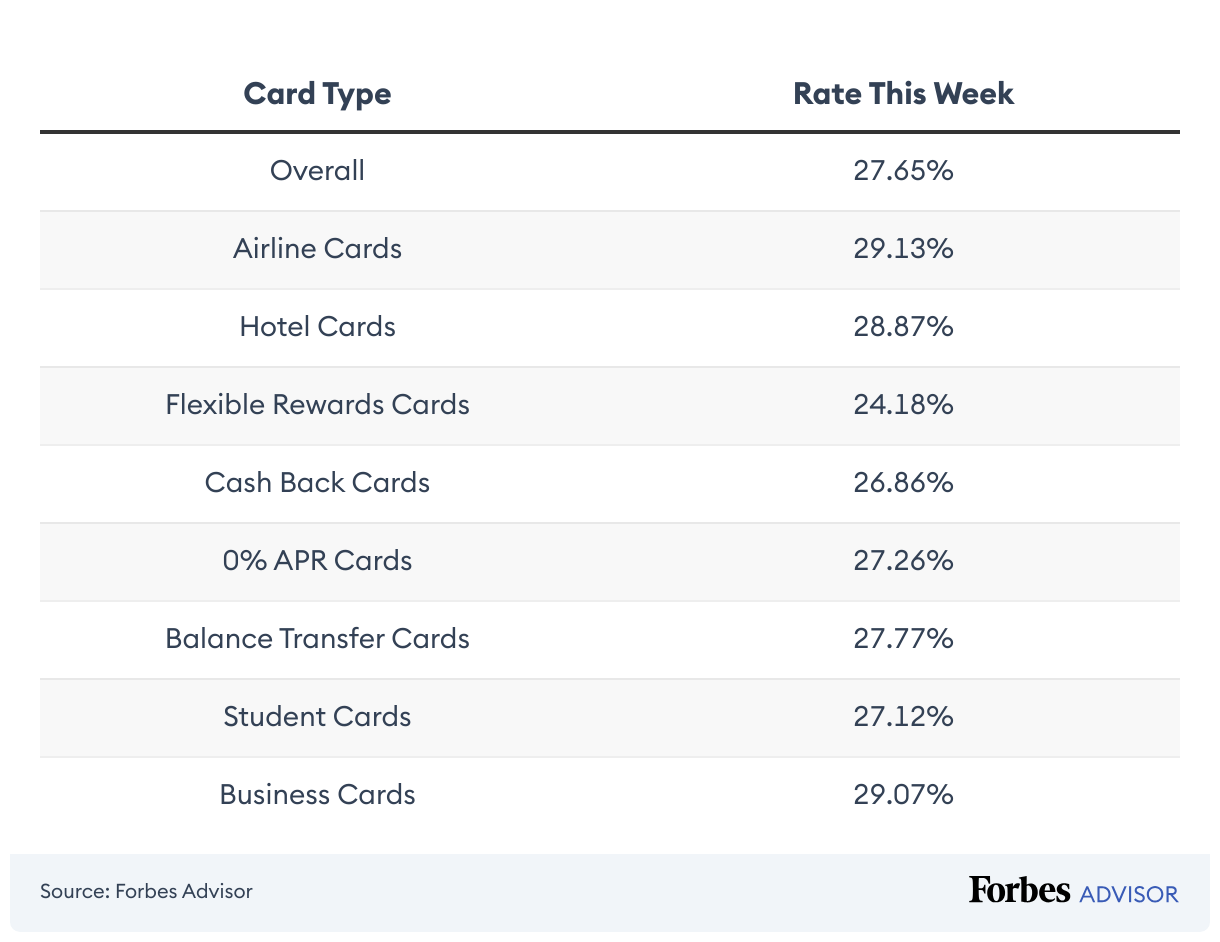

Average Credit Card Interest Rate by Card Type

The average overall APR across credit cards we track in our database is 24.10% this week, up from last week. Our overall average calculation includes airline, hotel, flexible rewards, cash back, 0% APR, balance transfer, student and business credit cards.

Methodology

Average credit card interest rates are calculated from a dataset of over 250 credit cards in the U.S. market. To calculate the average overall credit card interest rate, we use a subset of those cards—excluding business, student, secured and corporate cards. We calculate average rates for other card types using smaller, category-specific subsets.

Average Credit Card Interest Rate By Credit Score

Higher credit scores have the potential to help you qualify for lower interest rates on credit cards, loans, and other types of financing. As a result, a good credit score has the potential to save you money.

Bad credit scores, on the other hand, indicate higher risk for the credit card company. This status tends to translate into higher APRs for you as a cardholder. It’s not unheard of to encounter credit cards with APRs as high as 25% to 30%.

Exact interest rates on credit cards can differ from one company to another, and among individual cardholders as well. The type of credit card you open can play a role in your APR as well, with rewards credit cards often featuring higher interest rates than other types of credit card products.

Below is a look at the approximate APR range you might encounter on a general purpose credit card, according to your credit score. You should always check with the individual credit card issuer to confirm which rates are offered on any account you’re considering.

Read More: Credit Cards For Bad Credit

How Your Credit Card Interest Rate Can Impact You

When it comes to interest rates, it’s always best to secure the lowest number possible. On paper the difference between a 15% APR and a 20% APR might not seem like that much. But if you revolve a balance on your credit card account, a lower interest rate has the potential to save you thousands of dollars. Below is an example.

As you can see above, your credit card interest rate can also impact how long it takes you to pay down your credit card debt. A lower APR can make debt elimination faster and easier.

Of course, the best way to manage credit cards is to pay off your balance in full each month. If you can develop this habit and avoid credit card debt in the first place, then the APR on your account shouldn’t have any impact on your budget. In fact, when you pay off your full statement balance on a monthly basis, you can avoid paying credit card interest altogether.

How to Reduce the Interest Rate on Your Credit Card

If you’re working to pay down credit card debt, securing a lower interest rate could help you save money and get out of debt faster. Below are several strategies you can use to try to lower your credit card APR.

- Balance Transfer: You might be able to open a new credit card to take advantage of a low-rate or 0% APR balance transfer offer. Low introductory interest rates on balance transfer credit cards don’t last forever (typically 12 to 18 months). But if you can afford to aggressively attack your debt while the introductory APR is in place, you might be able to take a big bite out of your credit card debt, or perhaps pay it off in full.

A balance transfer calculator can help you factor in balance transfer fees, introductory rates, and more to add up your potential savings. It’s also wise to compare multiple balance transfer credit card offers to make sure you find the best deal and best fit for your situation. Keep in mind, you’ll typically need good to excellent credit to qualify. - Consolidation Loan: Another way you may be able to find a lower interest rate for your existing credit card debt is to pay it off with a debt consolidation loan. Depending on your credit rating, debt-to-income (DTI) ratio, and other factors, you may be able to take out a new personal loan with a lower interest rate than you’re paying on your credit card accounts.

A low-rate debt consolidation loan could save you money and escalate the debt elimination process. Plus, by consolidating your revolving credit card debt with an installment loan, you could reduce your credit card utilization rate and potentially improve your credit score at the same time. - Ask Your Credit Card Issuer: Your credit card APR isn’t carved in stone. You can ask your credit card issuer if they’re willing to reduce your credit card interest rate, and in some cases you might have success.

Let the card issuer know if you’ve seen credit card offers with lower interest rates that you’re considering. Having a history of on-time payments on your account and a good credit score could also work in your favor when you make your request.

Quick Tips on How to Improve Your Credit

Whether you’re trying to secure a low interest rate on a new credit card account or you’re looking to lower the APR on an existing account, having a good credit score can give you an advantage. Good credit improves your odds of qualifying for new accounts and getting the best interest rates and terms that credit card companies have to offer.

In truth, it can take some time to go from bad or even fair credit to a good credit score. But there are actions you can take that might help you see some credit score improvement sooner rather than later.

- Check your credit reports. Knowing where you stand is a critical step when you’re trying to improve your credit. The good news is that checking your three credit reports from the major credit bureaus (Equifax, TransUnion, and Experian) is easy and free. Visit AnnualCreditReport.com to claim a free credit report from each bureau once every 12 months. During the pandemic, you can enjoy free weekly access to your credit reports through the same website.

- Make a note of derogatory credit information. Once you have your reports in hand, go through them from top to bottom. Make a note of any negative information you find that might be hurting your credit scores. You might not be able to do anything about these issues until they age off your credit report eventually. But you can make a point to avoid repeating the same mistakes.

- Dispute credit errors. As you go through your credit reports, you should also list out credit reporting errors or signs of fraud you discover. The Fair Credit Reporting Act (FCRA) allows you to dispute any inaccurate information that shows up on your credit report with the appropriate credit bureau.

- Pay down your credit card balances. Lowering your credit card balances, and your credit utilization ratio by extension, can be one of the most actionable ways to improve your credit score. Credit utilization is a major credit score factor—largely responsible for 30% of your FICO Score. When you have a low credit utilization ratio, it indicates that you are a lower credit risk.

- Show positive payment history. The way you pay your credit obligations—on time or late—is the most important factor in determining your FICO Score. When you avoid late payments, you can set yourself up for success in terms of your credit score. Yet even the occasional delinquency on your credit report could potentially be a major setback.

- Consider opening new accounts. If you have a thin credit file or need to build credit for the first time, opening new credit accounts might benefit you. With no credit history, it can be challenging to qualify for certain loans or credit cards. But some options, like secured credit cards or credit-builder loans, might work well for you as long as you always pay on time. You can also think about asking a loved one to add you as an authorized user on an existing credit card account.

Bottom Line

Improving your credit can make it easier to qualify for attractive credit card interest rates. But don’t be too discouraged if you need to up your credit score before you can qualify for the best deals available. As long as you pay your statement balance in full each month, you can enjoy the many benefits that credit cards have to offer without paying any interest fees—regardless of the current APR on your credit card account.

More From Advisor

- What Is A Student Credit Card?

- American Eagle Credit Card: 4 Key Benefits and Alternatives

- Best Credit Cards Of March 2023

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.