We are rapidly approaching the end of 2021 but policymakers are not letting up in terms of their approach to crypto. Last week’s letter to stablecoin issuers is yet another step in this ongoing story.

You’re reading State of Crypto, a CoinDesk newsletter looking at the intersection of cryptocurrency and government. Click here to sign up for future editions.

When stablecoin rules?

The narrative

Last week, U.S. Sen. Sherrod Brown (D-Ohio) sent letters to a handful of stablecoin issuers asking for more information about their issuances, governance, consumer protection policies and more. It’s the latest move in an escalating effort by lawmakers, particularly the Senate Banking Committee chairman, to understand and evaluate stablecoins.

Why it matters

Lawmakers are grappling with stablecoins worldwide, but we’re starting to see movement from just asking questions to the beginnings of actual policy proposals and potential laws. In that light, the questions Brown is asking stablecoin issuers could identify what issues might fall into the explicitly defined regulatory landscape.

Breaking it down

Brown sent letters to Circle, Coinbase, Gemini, Paxos, TrustToken, Binance.US, the Centre Consortium (which Coinbase and Circle jointly operate) and Tether, asking for information about the respective stablecoins they issue.

Roughly summarized, the questions ask:

- How customers can acquire the stablecoins;

- How customers can redeem the stablecoin;

- How much of the stablecoin has been issued;

- What might prevent a customer from purchasing the stablecoin;

- Whether any trading platforms have “special arrangements” with respect to the stablecoin;

- How specific levels of redemption might impact the issuer;

- How an exchange might evaluate forks.

Some letters had more questions than others, such as those to Coinbase and Gemini.

“I have significant concerns with the non-standardized terms applicable to redemption of particular stablecoins, how those terms differ from traditional assets, and how those terms may not be consistent across digital asset trading platforms,” Brown wrote in several of the letters.

The letters came a month after Brown, with a handful of other Democrat senators, wrote to Facebook, ordering it to halt its announced Novi pilot program as well as any work on the diem stablecoin project.

At the time, the lawmakers wrote that Facebook could not be trusted with customer data although, interestingly, this was not an issue discussed in last week’s letters.

Brown’s letter referenced the President’s Working Group on Financial Markets’ report on stablecoins, which the group published at the beginning of November.

In a similar vein, the Office of the Comptroller of the Currency, Federal Deposit Insurance Corporation and Federal Reserve published their joint sprint team timeline last week, announcing when they plan to announce further clarity around bank interactions with crypto, including stablecoin issuance.

Given a) the PWG’s recommendation that stablecoin issuers be regulated similarly to national banks and b) the PWG’s recommendation that Congress cement this proposal through legislation, it’s very possible that last week’s letters are a first step toward this regulation.

Biden’s rule

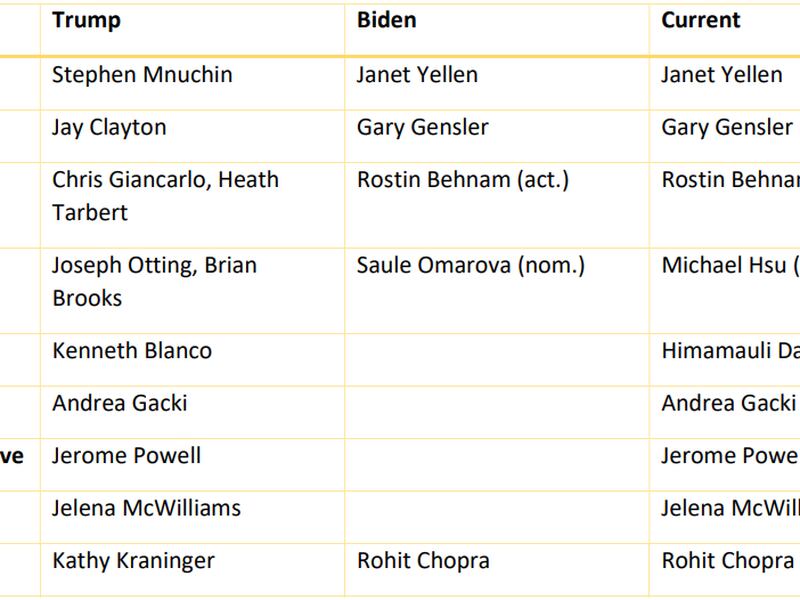

Changing of the guard

Five Democrat senators have expressed their opposition to OCC nominee Saule Omarova, Axios reported last week. The already contentious nomination has faced headwinds since being announced, and this state of affairs doesn’t look likely to change.

Elsewhere:

- European Council Takes One Step Closer to Ratifying Landmark Crypto Regulation: The European Council has adopted its stance on the Markets in Crypto Assets (MiCA) framework, bringing this landmark European Union-wide regulatory proposal closer to implementation. My colleague Sandali Handagama has the details.

- ConsenSys Suddenly Bars Iranian Students From Ethereum Coding Class: ConsenSys Academy touted scholarships for Iranian students earlier this year. Earlier this month, the education branch of the Ethereum software incubator told about 50 Iranian students it would remove them from its rolls. My colleague Anna Baydakova dug into what happened and why.

- Celsius CFO Arrested on Charges Tied to Former Job at Moshe Hogeg’s Firm: Yaron Shalem, who joined crypto lender Celsius as its chief financial officer in March of this year, was one of the individuals arrested alongside Israeli crypto entrepreneur Moshe Hogeg earlier this month (the charges appear to be unrelated to Celsius). This took some investigating by my colleague Ian Allison to report out.

Outside CoinDesk:

- (The New York Times) Uber allegedly had a team that watched over “competitors, opponents and disgruntled employees,” Kate Conger at the NYT reports. One of the members of this team claimed the others broke laws involving wiretapping and other crimes – but it appears this might not have been the case.

"Coach, before you go, we wanted to tell you one thing from the bottom of our hearts: This 7 a.m. meeting could have been, and was, a 10:08 p.m. text message." https://t.co/uSll3FBavE

— southpaw (@nycsouthpaw) November 30, 2021

If you’ve got thoughts or questions on what I should discuss next week or any other feedback you’d like to share, feel free to email me at nik@coindesk.com or find me on Twitter @nikhileshde.

You can also join the group conversation on Telegram.

See ya’ll next week!

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.