Credit: Shutterstock photo

Credit: Shutterstock photoBy Lutz Muller :

Toys "R" Us (TOYS) has basically three main businesses in the United States: toys, video games and baby products. None has done particularly well, as the chart below demonstrates:

Not so surprisingly, toys are the company's main business and its primary raison d'être. Toys "R" Us is also the last remaining specialty toy retailer, after the demise of Zany Brainy, Noodle Kidoodle, Imaginarium and others, and it thus offers innovative start-ups a way to showcase their products in a way no other retailer lets them do it. In 1996, the company added Babies "R" Us as a new retail sector, partly as free-standing stores and partly as a component of a regular Toys "R" Us store. Video games and consoles were the last addition to round out Toys "R" Us' product portfolio.

Both Babies "R" Us and video games were introduced to correct one major flaw in Toys "R" Us' concept - seasonality. The fourth quarter accounts for more than 40% of yearly toy sales, and it is absolutely crucial for the company to generate enough profit then to offset the losses incurred during the lean three quarters. This also makes it impossible for Toys "R" Us to follow the strategy of its main competitors - Wal-Mart ( WMT ) and Target ( TGT ) - to use toys as loss leaders during the fourth quarter as a strategy to draw in consumers and then sell them other stuff. Babies "R" Us and video games were introduced to flatten this seasonality curve. More so, it was hoped that the young mother who comes in to buy Pampers returns later to also buy toys. And that the teenager who visited the store as a young child with his or her mother to buy toys would later return to buy video games as well. To further accelerate this process, the role of Babies "R" Us within the TRU universe was further expanded by giving it more space and more promotional dollars.

In the U.S., its stores are in two major categories - regular stores and side-by-side stores. The difference is less in the overall footprint but rather how this footprint is allocated. In the regular stores, space is allocated roughly 60% toys, 20% baby products [Babies "R" Us], 15% video games and 5% stuff like check-out counters, service desks and toilets. Side-by-side stores allocate less space to toys [about 40%] and more to baby products [also 40%]. Regular stores are being converted to side-by-side stores on an ongoing basis, and today about half of the total 873 stores in the U.S. are in this format.

However, these diversification measures did not work out too well. Not only did overall U.S. sales, all categories, dropped from $8.317 million in 2009 to $7.638 million in 2013, the percentage contributed to these totals by Babies "R" Us and video games dropped from 52.7% in 2009 to 48.79% in 2013. In other words, sales of toys themselves stayed flat in terms of dollars and grew in terms of percent participation in the total - from 47.3% in 2009 to 51.2% in 2013.

This picture is replicated by what web searches say about consumer interest levels:

As you can see, the direction for Toys "R" Us overall is clearly trending down, and the same applies to Babies "R" Us. Also, competition did not stand still. This is what happened between 2009 and March 31 of this year in terms of market shares:

In other words, Toys "R" us had a U.S. toy market share of 17.2% in 2009, gradually increased it to 20.8% at the end of the third quarter 2012, and from there again declined to end up at 17.5% at the end of the first quarter this year. In fact, I suspect that the decline would have been even faster and steeper had it not been for the fact that both Wal-Mart and Kmart fell on their respective keisters due to their appallingly bad in-store management during the past few years. So, the question is why Toys "R" Us did relatively well for a while and then lost it again.

Many different reasons have been quoted, but two stand out because they affect the fundamentals of Toys "R "Us' mission - broadest product selection at competitive prices. The company fell down on both accounts.

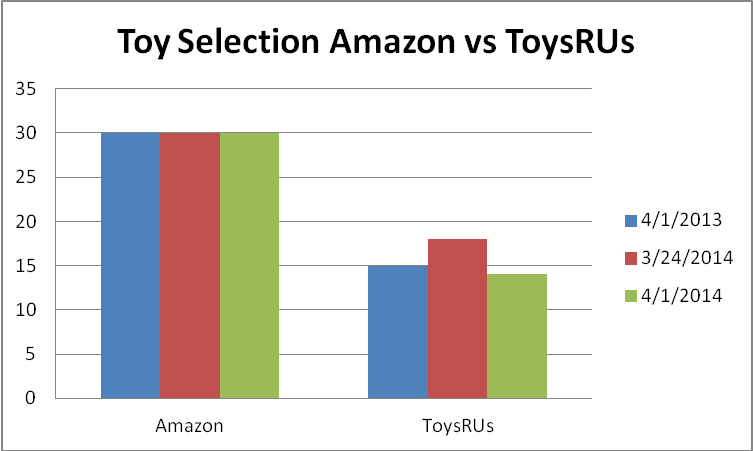

First, product selection. Toys "R" Us' most potent competitor is Amazon ( AMZN ), and Amazon is the company to beat in toy selection. I looked at Amazon's best-selling thirty toys at three time points and checked whether Toys "R" Us had these products available as well. This is the result:

In short, Toys "R" Us on average had only about half of Amazon's top-selling toys available to its customers. If the consumer wants a product and your competitor has it and you don't, you lose.

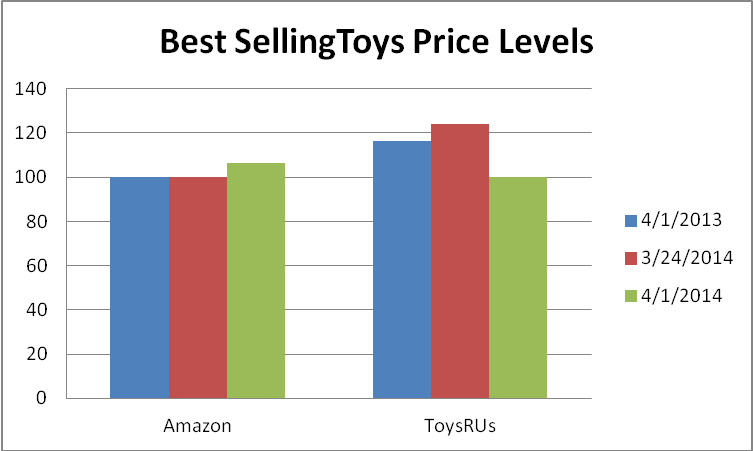

The second is price. I again checked Amazon's price against that of Toys "R" Us for those top-selling products carried by both retailers, also at the same three time points. This was the picture:

In two of the three cases, Amazon had clearly and significantly lower prices than Toys "R" Us, with Toys "R" Us being 16% and 24% higher. The most recent reading suggested that Toys "R" Us was in fact more competitive than Amazon by 6%. This is, however, due to a very recent price action by Toys "R" Us which, while on the surface tending in the right direction, was done in a very confusing manner and is likely to backfire rather than benefit the company.

This is how one of my esteemed colleagues described it:

First reactions from consumers are mixed. A lot are simply confused and there are, according to my retailer panel contacts, continuous discussions at the checkout counters about pricing. Also, the Service Desks report numbers of unhappy consumers arguing that they have been misled and wanting to return merchandise. It would appear that somebody in the company's Wayne, N.J., HQ was just too clever for their own good when designing and implementing this approach.

I do not think that these price reductions signal a change in Toys "R" Us' overall pricing strategy, but that they are simply designed to reduce inventory built up over the past six disappointing months.

However, there is little doubt that Toys "R" Us' management is trying to adapt its business model to accommodate pressure from the company's owners for greater profitability. I understand that a number of changes are in the offing to achieve this. Specifically, following the lay-offs already implemented at its Wayne headquarters, staff cuts are slowly being carried out on the shop floor level. Secondly, the closing of a significant number of unprofitable stores is under consideration. And finally, a greater emphasis on more profitable private label toy products is likely to become apparent as we move towards the 2014 fourth quarter selling season. This is likely to be only the beginning - all the three leading rating agencies Moody's, Fitch and Standard + Poor's - downgraded Toys "R" Us' debt this year, which means significantly higher borrowing costs starting in 2016. In short, Toys "R" Us' outlook over the next few years will be characterized by cost cutting, store closing, store staff lay-offs and other measures designed to boost short-term profit at the expense of long-term life expectancy.

It could well be that Toys "R" Us' overriding consumer promise of broadest product selection at competitive prices is no longer practical in the face of competition from Amazon and others who have a built-in economic advantage. It is also understandable that the owners - Bain, KKR ( KKR ) and Vornado ( VNO ) - are pressuring management to cut costs and to boost profits, regardless of long-term consequences. However, this is a one-way street littered with signposts that say "Kmart," "Frank's Nursery" and "Borders." Consumers do not forgive retailers who stray away from their fundamental mission promise.

However, it is not only consumers that are affected if Toys "R" Us changes its posture. The large toy manufacturers - Mattel (MAT), Hasbro (HAS), Jakks (JAKK), and Lego - depend on TRU to a major degree. They have basically two choices: they can either support the company with promotional activities and markdown dollars, or they can elect to leave the sinking ship. Whatever they choose to do will determine whether Toys "R" Us will live or die.

All charts courtesy ofKlosters Retailer Panel unless noted otherwise.

(This article was first published on April 30 by the Toy Directory.)

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

See also Killam Properties: Solid Fundamentals With Take Private Possibility Serving As Upside on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}