News & Insights

The SEC is set to split U.S. ticks tomorrow

The U.S. Securities and Exchange Commission (SEC) has scheduled a meeting for tomorrow where they are expected to release final rules on their Tick Size Proposal from 2022. There have been a lot of comments — including Nasdaq’s — as well as academic data, showing how ticks work, so it will be interesting to see what experts the SEC has listened to.

The right tick size can make trading costs much lower

We already know tick sizes make a big difference to how stocks trade. We have spent a lot of time discussing the importance of tick size in previous blogs, including getting tick right improves valuation, the economics of tick regimes, and what ticks make spreads trade best.

But it’s not just us who have spent a lot of time analyzing ticks. Today, we focus on other people's research. What they consistently find is that tick size and depth are a trade-off: smaller tick size reduces spread costs, but also reduces depth. That makes small trades cheaper, but large orders harder to trade.

U.S. ticks haven’t always been 1-cent for all stocks

Historically, tick size was 1/8 of a dollar for more than 200 years in the U.S. equity market until 1997, when exchanges started to reduce the tick size from 1/8 to 1/16. In 2000, tick size was further reduced to 1 cent as electronic trading started to dominate all trading.

These reductions in tick size prompted the debate on the optimal tick size among the industry, regulators and academics.

Ticks make little difference to supply and demand, but change trading costs

Interestingly, research before decimalization tended to be more theoretical, while newer research uses real data and compares real examples. Overwhelmingly, though, most research discovered the same trade-off: smaller tick size reduces spread costs but also reduces depth.

This is not all that surprising to an economist. The depth of book is a classic example of a supply and demand curve, with:

- Demand (buying increasing as prices fall) and

- Supply (sellers increasing as prices rise), and an

- Equilibrium price (where the last trade happened).

Clearing all volume below the equilibrium price results in a V-shaped supply and demand curve that is surprisingly linear (a straight line).

It would seem that changing the tick for trading just changes the increments along the supply and demand curve where trades can occur – but not the actual supply and demand for stocks.

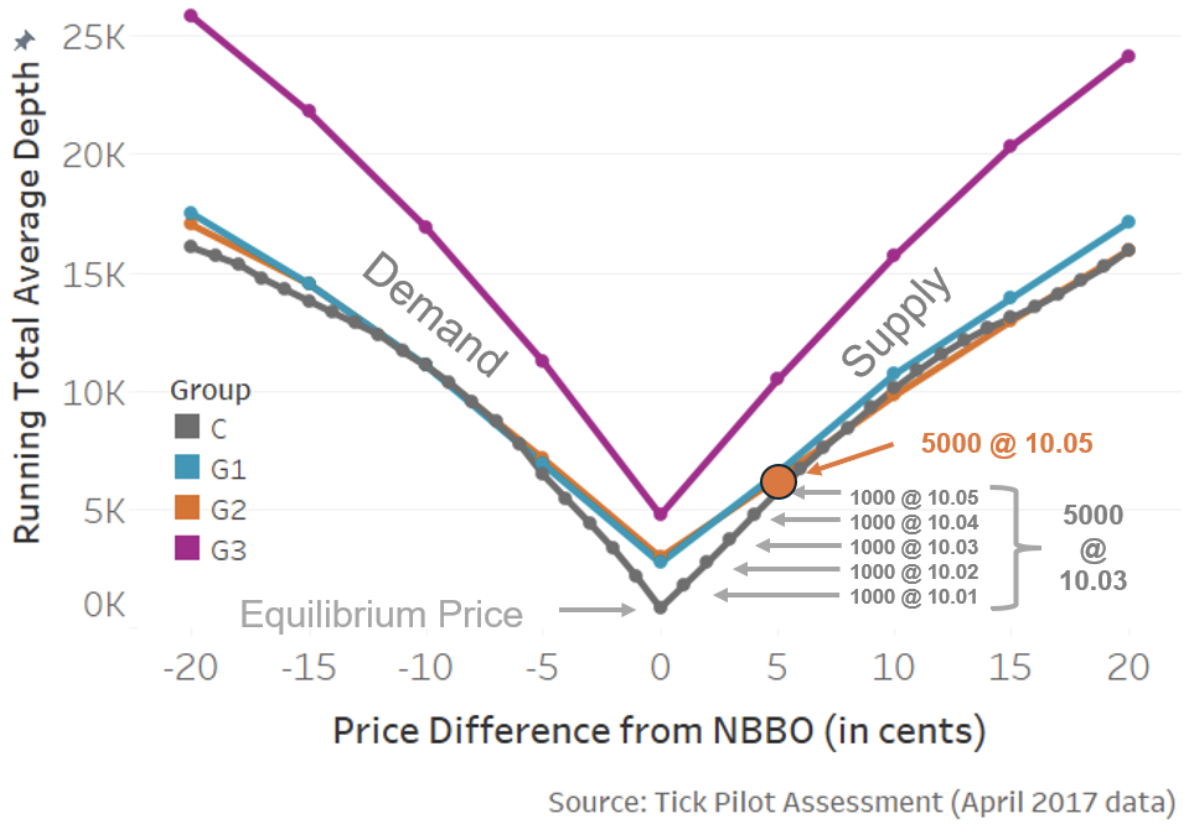

One study that proves this point clearly is the tick pilot report (Chart 1). The data from it showed that the cumulative volume for the 1-cent tick group (control, C group) and 5 cent tick groups (G1 & G2) remain basically the same.

The only group that saw both ticks and depth improve was the trade-at group (G3). Although some might say that the difference just represents the volume that is “hidden” in today’s more segmented markets.

Chart 1: Smaller ticks lead to lower depth in Tick Pilot stocks; only the trade-at group saw lit market quality improve

Key research on ticks

Since tick size reduction can make stocks trade very differently, it is important to understand if a smaller tick size improves market quality or increases the costs for large trades.

Good market design should balance the trade-off between minimizing the quoted spread and depth. A smaller tick size may be:

- Beneficial to retail investors, since it reduces the spread transaction cost.

- Worse for larger institutional investors (who manage retail investors funds), who may see more impact cost as they “work” their larger orders in thinner markets.

We list the key studies from this topic in Table 1 below, but the findings worth knowing include:

Theoretical research: Predicts smaller tick size reduces spread and depth

Harris (in 1994) predicted that a reduction in tick size would lead to a decrease in quoted spread.

Other researchers (Seppi in 1997) came to the same conclusion using different logic – they suggested that smaller tick size reduces the cost of queue priority, which reduces protection to liquidity suppliers, and thus results in reduction in their displayed depth.

Empirical findings: Smaller tick size reduces spread and depth

Many studies used “real” data coming from events that reduced U.S. tick sizes, such as:

- Tick size reduction from 1/8 to 1/16 in 1997,

- Tick size decimalization in 2001 and

- Tick size pilot program in 2016.

Looking at the tick size reduction from $1/8 to $1/16, Goldstein and Kavajecz (2000) showed that a tick size reduction reduces the quoted spread, although they also saw a reduction in cumulative depth as well. Jones and Lipson (2001) found that although the tick reduction to 1/16 led to a reduction in both quoted and effective spreads, the total execution costs for institutions increased.

Studying the tick size decimalization, Chakravarty et al. (2001) also showed that reducing the tick size resulted in a lower spread and depth. They also found that institutional orders took longer to fill, which adds to opportunity costs.

A few recent studies explore the tick size pilot program. Statistically, the tick pilot was easier to analyze because some stocks remained unchanged (in the “control” group), meaning changes in markets over time, like periods of volatility, could be removed from the results.

Consistent with earlier studies, Chung et al. (2020) and Rindi and Werner (2019) implied that a smaller tick size would reduce the trading cost of small orders but increase the cost of large orders.

Studies also show that the same tick change can yield different impacts on tick constrained and unconstrained stocks. For:

- Tick-constrained stocks, a smaller tick size would lead to a reduction in the spread and depth (Albuquerque et al. (2020), Chuang, Lee and Rosch (2020) and (Rindi and Werner (2019)).

- “Too-many-tick” stocks show that sometimes a “too-narrow” tick size could actually increase the spread. This is why Blackrock and others have suggested 5-cent ticks should also be considered for wide spread stocks.

Table 1: Comparing academic research and its key findings

Tick-constrained problem vs. Too-many-ticks problem

The results from the last two studies in Table 1 share the same finding we’ve noted before regarding stock splits: ticks that are too small are bad, too. That’s consistent with another set of studies we analyzed that suggest that 1-3 ticks wide spread is optimal.

In that context, it's interesting to look at the U.S. stock universe. Just how many stocks are constrained…and how many have “too many ticks”?

In the chart below, we show each stock (as a dot), colored based on their average actual spreads. It shows that:

- About 764 stocks are tick constrained (blue group), which would benefit from a tick size reduction.

- About 943 stocks are optimally ticked (yellow group), of which the current tick size is optimal.

- About 1,526 stocks are slightly over ticked (light grey). They could benefit from a small tick size increase, although the benefit may not be worth the complexity.

- About 1,669 stocks have too many ticks (dark grey). They would benefit from a tick size increase.

Chart 2: There are more U.S. stocks that have “too many ticks” than are “tick constrained”

Ticks haven’t changed for 24 years — is depth and spread unchanged, too?

Looking at data since 2015, it would seem that spread and depth has been getting worse, even for liquid S&P 500 stocks.

Some of the increase in spreads (especially the sporadic spikes) is likely due to higher volatility. However, with volatility in the second quarter of 2024 back to unusually low levels, spreads remain elevated (blue line) while depth (pink line) remains near its lows.

Chart 3: Spreads and depth are worse, even with no recent changes in tick size

Given the tick size hasn’t changed in over 20 years, why is this happening?

Academics who studied cream skimming and market segmentation may have the answer. Their studies theorized that as markets segment, liquidity would rest elsewhere, available only to a more profitable subset of customers. As a consequence, “fair access” (lit) quotes would decrease.

Given the findings in today’s blog, that could result in either spreads widening or depth falling, or (plausibly) a combination of both.

Not surprisingly, that’s the opposite to what we saw from the “trade-at” group in the tick pilot, which intentionally tried to unsegment the market and increase all-to-all trading.

What does this all mean?

There is lots of data on how ticks can impact market quality.

Their findings suggest we need to weigh the costs of retail and institutional investors (and issuers, too).

The data suggests we shouldn’t have ticks that are too large (creating tick constrained stocks), but we should also avoid having ticks that are too small (leaving too many ticks inside a spread).

At the end of the day, the NBBO is important to all kinds of investors, as well as the costs of capital for companies. Ticks alone might not affect supply and demand curves, but getting ticks wrong could increase costs for everyone.

Market Makers Newsletter

Get market insights and analysis from Nasdaq Chief Economist Phil Mackintosh straight to your inbox

Latest articles

This data feed is not available at this time.

Data is currently not available