The semiconductor industry has delivered tremendous growth over the last several decades. Demand for chips can experience downturns, especially during economic recessions, but history shows that more advanced devices and technologies require more powerful processors, which creates an upward-sloping demand curve. In the near term, artificial intelligence (AI) continues to be a key sales catalyst for leading chip suppliers.

IDC's latest report projects the semiconductor market will grow 15% in 2025, led by AI demand. This could spell a great buying opportunity for stocks that have recently fallen in value.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. See the 10 stocks »

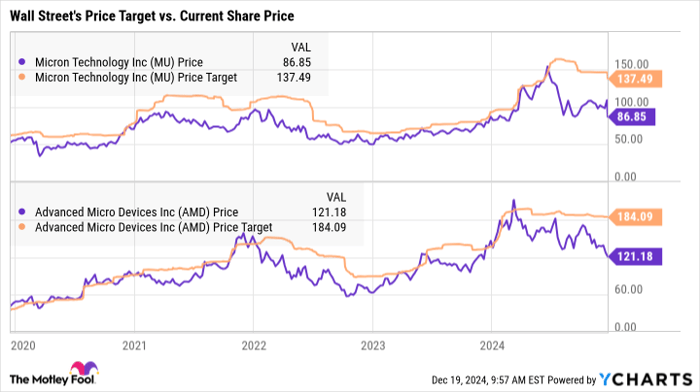

Two stocks earning high praise on Wall Street are Advanced Micro Devices (NASDAQ: AMD) and Micron Technology (NASDAQ: MU). These stocks are trading well off their recent highs but have been reporting robust revenue growth from the data center market.

The average Wall Street price target is 55% higher than AMD's share price of roughly $121 and 53% above Micron's share price hovering near $87. Let's take a deeper look at these companies to see if it's a smart move to bet your money on Wall Street's opinion.

Data by YCharts

Advanced Micro Devices expects demand to pick up

Shares of Advanced Micro Devices have delivered outstanding returns in recent years. AMD is making a lot of gains in the server market, which is coming at Intel's expense. Over the last few years, its market share of central processing units (CPUs) used in servers increased from the single digits to 34%.

AMD also sees strong demand for its graphics processing units (GPUs) in the data center market, and this is the opportunity that could catapult the stock higher in 2025. Despite soft results in gaming and industrial markets, AMD's growth in data center helped drive double-digit revenue growth in Q3 over the year-ago quarter. Analysts expect AMD to report year-over-year revenue growth of 13% for 2024, according to Yahoo! Finance.

Next year could see growth accelerate if demand in other segments picks up. For example, AMD's embedded chip revenue, including sales for industrial markets, was down 25% year over year in Q3, but the segment's revenue grew 8% over the previous quarter.

With AMD stock selling 43% off its previous highs and trading at just 23 times next year's consensus earnings estimate, Wall Street's price target could be on the money.

AMD expects the market for AI accelerators, or GPUs, to grow over 60% annually to reach $500 billion by 2028. It's got a potentially long runway of growth ahead, and these advanced processors generate above-average profit margins. This should allow earnings to grow faster than revenue.

Analysts expect AMD to grow earnings at an annualized rate of 41%. For 2025, the Street is calling for earnings to reach $5.13. If the stock continues to trade at its current price-to-earnings multiple, the share price could climb along with earnings and reach Wall Street's price target of $184.

Of course, a sudden downturn in the chip industry would stall AMD's momentum and limit the stock's gains. But with the share price already trading at a big discount to previous highs, there is a favorable risk-reward setup for AMD investors heading into 2025.

Micron Technology's low valuation is tempting

Micron Technology is a leading supplier of memory and storage products for data centers, original equipment manufacturers, and consumer markets. The stock has had a good run since bottoming out in 2022, with the share price up 71%. But the shares are trading well off their highs as demand for dynamic random access memory (DRAM) weakened this year.

The company just reported fiscal first-quarter results, where a soft outlook sent the stock down again. Sales to data centers grew 400% year over year and 40% over the previous quarter. Data center sales now make up over half of Micron's total revenue.

Micron also said its high-bandwidth memory (HBM) shipments were ahead of expectations, with HBM revenue more than doubling over the previous quarter.

Offsetting these positive demand trends was management's soft outlook for fiscal Q2. Revenue guidance was below the Street's estimates, but management said this is a temporary bump in the road stemming from an inventory adjustment by customers in consumer-related markets. The company expects this adjustment to be completed soon.

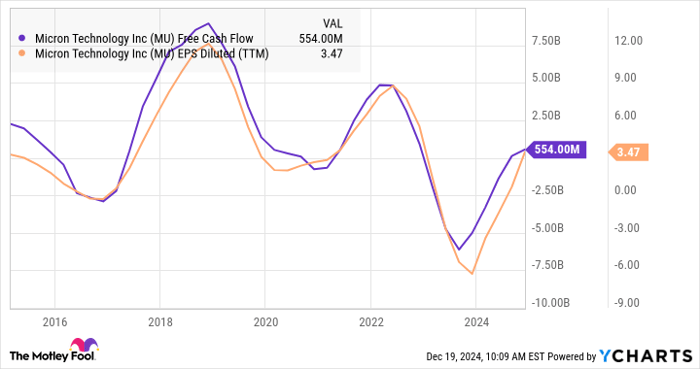

Based on its updated outlook, Micron still expects to achieve record revenue and positive free cash flow in fiscal 2025 (which ends in August).

The stock looks cheap at these lower share prices, but there is the risk that it could be a value trap. The problem is that Micron has an inconsistent operating history. While revenue has steadily grown over the last decade, the competitive nature of the memory market has caused major swings in Micron's earnings per share (EPS) and free cash flow.

The stock is cheap enough that if the company delivers on management's outlook for the full year, the stock could return to its previous highs. At the current share price of $86, the stock is trading at 10 times this year's earnings estimate and 6.6 times fiscal 2026 estimates. Those low valuation multiples are tempting.

Still, AMD offers the better risk-reward and is the safer bet to hit Wall Street's price target in 2025. Micron's latest quarter is a good reminder that there are a lot of variables impacting demand for its products that are difficult to predict, which makes valuing the company a challenge.

Where to invest $1,000 right now

When our analyst team has a stock tip, it can pay to listen. After all, Stock Advisor’s total average return is 901% — a market-crushing outperformance compared to 173% for the S&P 500.*

They just revealed what they believe are the 10 best stocks for investors to buy right now… and Advanced Micro Devices made the list -- but there are 9 other stocks you may be overlooking.

*Stock Advisor returns as of December 16, 2024

John Ballard has positions in Advanced Micro Devices. The Motley Fool has positions in and recommends Advanced Micro Devices. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.