Welcome back to our 2022 regtech series, where we trace the evolution of regtech adoption in financial services and the legal industry, the regtech funding market, and specific strengths and weaknesses of regtech. In this post, I discuss the current state of cryptocurrency and why decentralized finance (DeFi) is distinct and different from crypto. Let’s dive in.

The Divorce of Crypto and DeFi

Most people barely understand cryptocurrencies, and many of those main-streeters who have a basic knowledge of crypto don’t understand how it's different from DeFi. While both rely on blockchain technology and are financial in nature, that’s about as far as the connection goes. Crypto is in a complete market crash. DeFi, not so much. Sure, DeFi markets are in bear territory, but so are the S&P 500, Nasdaq, and U.S. bond markets.

Putting a “Fork” in Crypto

Let’s quickly address the 800-pound gorilla in the room. All major crypto markets are getting throttled. As of June 10, 2022, Bitcoin was down 55 percent since its November 2021 peak, with the entire crypto market down 59 percent since then. By June 30, Bitcoin was down over 70 percent! (U.S. equities are down about 21 percent during that same period.) The drop in crypto prices is affecting miners, whose revenue has fallen by 56 percent since November.

Since May, crypto firms have been in a “contraction phase” as hiring and funding have declined, and layoffs have spiked. The Wall Street Journal reported that crypto-related job listings were down 20 percent between April 2022 and June 2022. Meanwhile, jobs at other online companies were up during that period. Large venture capital firms are still investing in the sector and some, like Andreessen Horowitz, have raised huge funds to last through the crypto winter. The rest of 2022 is likely to see lower amounts raised than in Q1 2021, which had $10 billion in crypto-related raises.

On June 12, Celsius Network, a crypto lender, froze withdrawals and other transactions on its platform, citing “extreme market conditions.” Celsius is one of many neo-banks that lend and borrow money and digital assets. Like other digital assets, Celsius’ coin was down substantially (about 80 percent) over the past year. Later, I’ll discuss why Celsius is not DeFi; rather, it is a centralized blockchain used by a highly levered firm that is collapsing like Lehman Brothers in 2008.

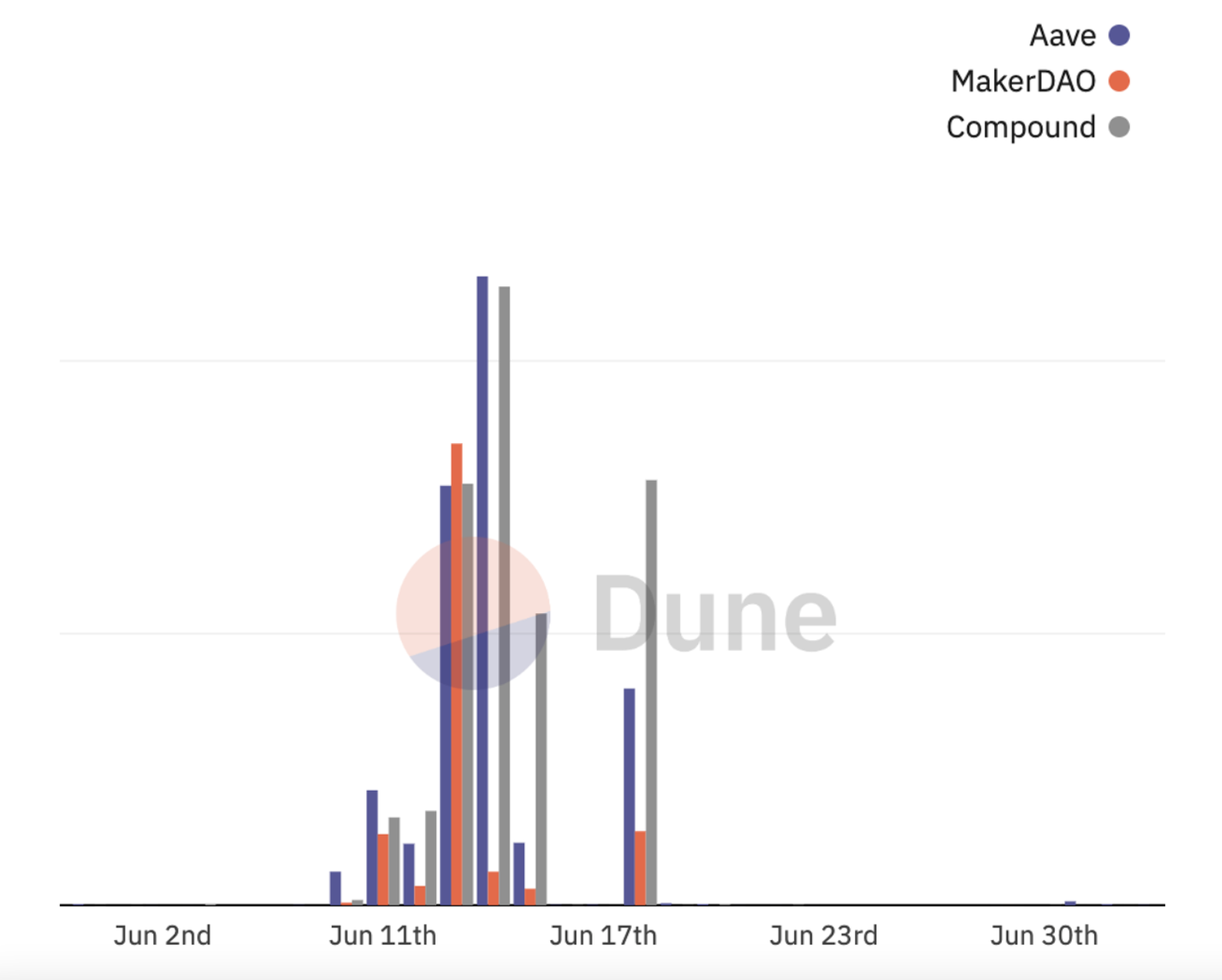

DeFi, on the other hand, is handling the contraction in stride. Yes, its assets are down as collateral on loans have liquidated and transaction activity has declined. But DeFi markets are acting more like traditional equity and bond markets—down but not in free fall. Axios and Dune Analytics reported that DeFi loan liquidations spiked in June, going from $358 in liquidations on June 5 to over $25 million on June 12 and $33 million on June 13! Many DeFi veterans believe the markets are acting in a healthy manner, and as expected.

Defining DeFi

Before we get too deep into a discussion on regulatory issues, let’s take a moment to define DeFi. DeFi projects are run by robots on the internet, not companies with management teams. The DeFi software has set rules around functionality. For example, when it comes to DeFi lending,

- every loan is guaranteed by collateral,

- collateral is sold to close to loan if repayment isn’t timely, and

- there's a fee against the borrower if the loan is liquidated (the stick).

In DeFi, all financial operations occur automatically and autonomously on an open blockchain.

Firms that issue digital coins and handle other financial transactions are not necessarily DeFi. For example, Celsius operated a closed blockchain network (keyword closed). Yes, it had an initial coin offering and allowed people to lend and borrow cryptocurrencies. But the closed nature of the business’ blockchain and its ability to manipulate that blockchain mean it was not decentralized. Celsius’ ability to block access to accounts proves that it wasn't DeFi. In a DeFi setting, Celsius would have needed to post a proposal for a public vote and discussion first. They didn’t because they wanted to avoid a “run on the bank.”

True DeFi firms are not likely to suffer from the contagion spreading through many crypto firms and their centralized blockchains. (I first saw the word “contagion” used in this context in a Wall Street Journal article that discussed the collapse of Three Arrows Capital on June 17, 2022.) A true DeFi firm is not leveraged like these venture-backed, high flying neo-banks. By design, DeFi firms are radically transparent and can’t simply turn off the spigot. During the worst days in June for crypto markets, DeFi saw $300 million in liquidations across the three biggest lenders, and yet there's over $40 billion in outstanding DeFi loans. As Compound Labs CEO Robert Leshner stated, “the protocols are doing what they are designed to do.”

Dealing with the Crypto Crash

The issue with cryptocurrencies is that they are not immune to systemic risk. The crypto crash in June 2022 was due, in part, to high inflation and recession fears that caused investors to flee risky assets, and crypto appeared to be the riskiest asset class of all. Celsius brought down Ethereum, which created issues at Three Arrows Capital. Lower crypto prices caused Coinbase to lay off 20 percent of its workforce, further exacerbating recession fears. The contagion rippling through traditional markets made waves in the crypto markets.

As crypto markets continued to unravel through the end of June, the term contagion kept appearing in various news media. For example, Axios noted on June 22, 2022, that FTX was becoming a last-resort lender for crypto firms such as BlockFi ($200 million credit line) and Voyager Digital ($500 million revolving loan and other loans). Writing for Axios, Ryan Lawler noted that “[t]here is a risk of contagion in the crypto industry as companies start to fall and default on obligations to other companies as they go.”

The crypto market crash is causing other blockchain and Web3 players to distance themselves from cryptocurrencies. Many executives at blockchain-based and Web3-focused companies are trying to distinguish their technology and business plans from cryptocurrency. They were happy to crash that party while the good times were rolling, but now that the party is busted, they are nowhere to be seen. But as Crystal Kim, writing for Axios, suggested, the current crypto bear market “is a greed problem, not a blockchain one. The business models of crypto exchanges, lenders and funds aren’t very different from their Wall Street counterparts. They all have to be very large to stay competitive because they are effectively running commoditized businesses.”

As always, the markets will continue to ebb and flow and no financial institutions or markets are immune to these waves, no matter how tumultuous they get. Whether on Wall Street or in crypto, stability requires careful planning and action. Will the issue continue to be greed-related? Will the business model of these crypto exchanges stay the course and help to reboot the market? It may be too early to tell, but rest assured, we’ll keep you in the loop.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Other Topics

Cryptocurrencies

Bo Howell

Bo has been the CEO of Joot, a fintech company, for over three years. He has helped design, develop, and implement technology in the financial services sector. Bo has over 10 years of experience as a securities lawyer and chief compliance officer.

Read Bo's Bio