Dividends are tangible returns on your investments in stocks -- and if you've left the workforce, they can help provide the cash you need to live a comfortable life. But only if you keep getting paid. That's why you need to focus on more than just dividend yield, and look at dividend safety as well. Here are three companies from the broader energy group that provide a good mix of income and safety.

1. Midstream powerhouse with ample coverage

Enterprise Products Partners (NYSE: EPD) is one of the largest midstream companies in North America, with a collection of assets that help move oil and natural gas around the world. It would be virtually impossible for a competitor to recreate this $50 billion market cap company's portfolio. Its business is largely based on fees, so it gets paid for the use of its assets. The often-volatile price of the commodities passing through its system aren't as important as demand for those commodities. And here's the best part: Its distributable cash flow covered the third-quarter distribution by 1.6 times.

Image source: Getty Images.

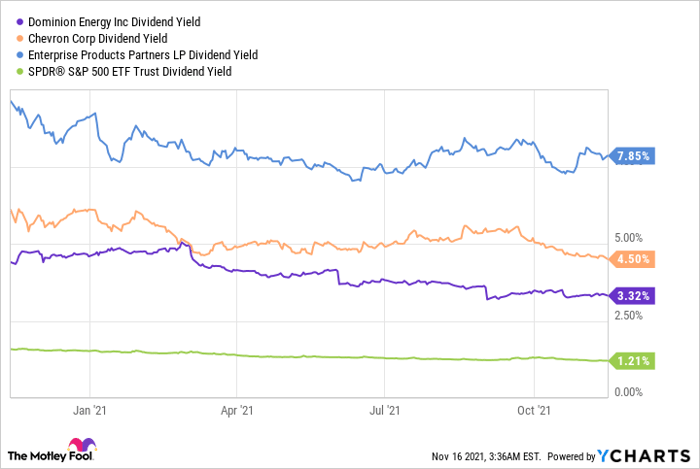

That's robust coverage that provides ample room for adversity before the distribution, which yields 7.8%, is at risk. In addition, the company has a history of using modest leverage, with a debt to earnings before interest, taxes, depreciation, and amortization (EBITDA) ratio of 3.9, which is toward the low end of its closest peers. It has increased its distribution for 24 consecutive years.

But what about the movement to reduce carbon emissions? That's a very real issue, but the transition away from oil and natural gas will likely take decades to complete. In fact, because of population growth and the financial growth of emerging markets, absolute demand for oil and natural gas is likely to keep growing through at least 2040. And that means master limited partnership Enterprise will continue to see robust demand for its services.

2. Drilling into the energy industry

If you're looking for a more direct way to play oil and natural gas, however, you might want to look at integrated energy giant Chevron (NYSE: CVX). The company's business spans from the upstream (drilling) space through the midstream arena and all the way to the downstream (refining and chemicals). The end goal is to help balance out the inherently volatile ups and downs in the commodity-driven drilling business, since downstream operations often benefit when oil and gas prices are low. However, given the ups and downs in the energy patch, the real safety value here is the balance sheet and the company's commitment to the distribution.

On the first front, Chevron's debt to equity ratio is roughly 0.28, the lowest of the energy majors. And that's after an opportunistic acquisition in 2020 that helped to ensure Chevron came out of that year's nasty energy downturn a stronger company. Then there's the 34 consecutive years of annual dividend increases, including in 2020, which shows a dedication to returning cash to investors even during hard times. The key here is to remember that during energy downturns that commitment will usually mean using the balance sheet to fund the dividend for a bit before the energy market rebounds. The stock yields 4.7%.

D Dividend Yield data by YCharts

3. A dividend cut?

The final name here is going to break the mold a little, because Dominion Energy (NYSE: D) recently cut its dividend. However, it is important to understand why, and what it means for the dividend going forward. Effectively, Dominion has been simplifying and de-risking its business for more than a decade, jettisoning oil drilling assets and midstream pipelines, among other things. The last big move was selling midstream assets to Berkshire Hathaway. But that represented a huge chunk of the company's business and, thus, a dividend cut was necessary. What's left now is a boring old regulated utility, one of the largest in the United States, with much-improved dividend coverage and growth prospects.

At this point, Dominion is expecting to grow earnings by around 6.5% a year through at least 2025. That is expected to translate into 6% dividend growth, a notable level for a utility. Combined with its roughly-3.4% dividend yield (backed by a modest payout ratio of around 65%), that should equate to around 10% annual returns for investors. That's backed by a $32 billion five-year capital investment plan.

The key here, however, is that Dominion is a regulated utility, so all of that spending has to be approved by regulators. Once regulators are on board, it is likely to take place no matter what's going on in the stock market. That makes this something of a boring cornerstone investment -- but boring can be good when you are a dividend-focused investor.

Energy options that help you sleep at night

The energy sector can be volatile, but that doesn't mean your investments in the sector have to be. That's why large, financially strong players like Enterprise, Chevron, and Dominion are great ways to play the space for dividend investors. All three have sizable yields, strong businesses, and conservative approaches that should yield material benefits for income seekers today and in the future. It's likely that at least one will find its way into your portfolio if you take the time for some deep dives here.

10 stocks we like better than Chevron

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Chevron wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of November 10, 2021

Reuben Gregg Brewer owns shares of Dominion Energy, Inc. The Motley Fool owns shares of and recommends Berkshire Hathaway (B shares). The Motley Fool recommends Dominion Energy, Inc and Enterprise Products Partners and recommends the following options: long January 2023 $200 calls on Berkshire Hathaway (B shares), short January 2023 $200 puts on Berkshire Hathaway (B shares), and short January 2023 $265 calls on Berkshire Hathaway (B shares). The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.