Seagate Technology Holdings plc STX shares have been performing well on the trading front, with the stock gaining 33.7% in the past year compared with the sub-industry’s growth of 32.7%.

The uptrend is driven by Seagate’s impressive top-line performance in the past few quarters. The company is witnessing an increasing demand for its mass capacity solutions. STX’s earnings beat estimates in all of the last four quarters, delivering an average surprise of 85.1%.

One-Year Price Performance

Image Source: Zacks Investment Research

Despite strong gains, STX is still down 13.5% from its 52-week high of $115.32, reached on Oct. 15, 2024. Does this indicate a buying opportunity?

Let’s dive into STX’s prospects and determine your portfolio's best course of action.

Mass Capacity Demand: Key Growth Driver

Seagate, a leader in data storage solutions, is well-poised for strong growth amid favorable mass capacity demand trends despite stiff competition from prominent players in the storage space like NetApp NTAP, Pure Storage PSTG and Western Digital Corporation WDC.

In the last reported quarter, mass capacity revenues surged 70% year over year and 21% sequentially, owing to stronger nearline cloud demand and increasing nearline enterprise sales. Its mass capacity exabyte shipments now represent more than 93% of HDD exabyte shipments.

Nearline cloud demand was mainly driven by cloud service providers (“CSPs”) across the United States. Seagate added that it has been witnessing positive demand trends globally. Management anticipates continued improvement in the fiscal second quarter, owing to shipments for the latest high-capacity products expanded across global CSP and enterprise customers. Also, cloud service providers are focusing more on the development and deployment of AI applications while building cloud infrastructure. Seagate believes HDDs will play a key role in enabling these stages of the AI adoption curve and expects HDD demand to pick up pace going ahead.

Management anticipates second-quarter fiscal 2025 revenues to be $2.3 billion (+/- $150 million). STX expects continued momentum in mass capacity demand, caused by strengthening nearline demand from global cloud customers and improvement in the enterprise & OEM markets. This increase in mass capacity revenues is likely to offset lower revenues from legacy and other markets.

Mozaic Platform: A Game Changer for STX?

Seagate expects secular trends and innovations to drive up aerial density to benefit mass capacity storage. Management also noted that the launch of the Mozaic 3+ hard drive platform earlier in the year, which featured HAMR (heat-assisted magnetic recording) technology, positioned it well to capture share in the mass capacity storage solutions market.

Seagate expects HAMR to aid in exploiting megatrends like AI and machine learning, which will drive long-term demand for cost-effective mass-capacity storage solutions. The company has been ramping up its 24TB CMR / 28TB SMR drives, and these now represent the second-highest revenue product, contributing more than 20% of total nearline revenues.

Seagate added adoption of Mozaic 3+ was gaining steam. The qualification with the lead CSP customer is progressing well and it has expanded qualifications with several other cloud and enterprise customers in the current quarter. The company anticipates delivering capacity increases through further aerial density gains for its Mozaic 4+ platform. This will lead to lower savings for its customers.

STX’s Improving Profitability

Focus on high-capacity HDDs and cost efficiencies in a healthy industry supply-demand environment is driving margin expansion for Seagate. In the last reported quarter, non-GAAP gross margin increased to 33.3% from 19.8% in the prior-year quarter. Non-GAAP income from operations totaled $442 million, up from $40 million a year ago. Non-GAAP operating margin increased to 20.4% from 2.8% in the year-earlier quarter.

Image Source: Zacks Investment Research

Going ahead, STX expects gross margin is expected to benefit from a higher mix of mass capacity revenues and ongoing pricing actions. At the midpoint of the revenue guidance, management expects the non-GAAP operating margin to grow in the low-20s percentage range of revenues in the current quarter.

Driven by strong revenue and margin performance, along with robust liquidity levels, STX raised its quarterly dividend by 3% to 72 cents.

However, increasing expenses could drag down margin performance. This is especially true if top-line expansion fails to keep pace with mounting costs. In the last reported quarter, non-GAAP operating expenses were up 13% on a year-over-year basis to $281 million, primarily due to higher variable compensation, and for the current quarter, the same is expected to be 285 million.

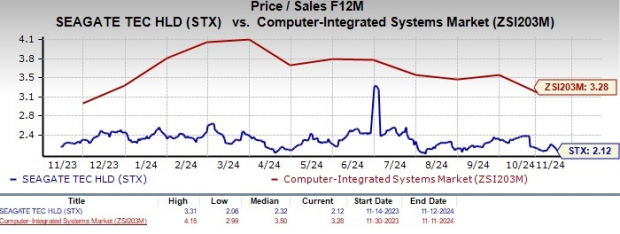

STX’s Attractive Valuation

Seagate presents a compelling investment opportunity with its attractive forward 12-month price-to-sales ratio of 2.12X, significantly lower than the industry average of 3.28X observed over the past year. Its forward 12-month price-to-sales ratio positions Seagate as a value-driven choice with significant upside potential.

Image Source: Zacks Investment Research

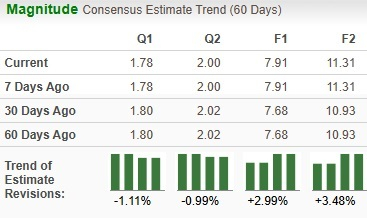

STX Estimate Revision Activity

Though estimates for the current quarter and next quarter have been marginally revised downwards, the same for the current and the next fiscal year have been revised upward by 3% and 3.5% in the past 60 days.

Image Source: Zacks Investment Research

Here’s Why STX Shares Are a Buy

Strong financial performance, strategic initiatives, favorable demand trends, and appealing dividend policy make Seagate an attractive investment opportunity. Given the recent pullback from its 52-week high, investors have an opportunity to invest in this Zacks Rank #2 (Buy) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Apart from a favorable rank, STX has a Growth Score of B. Per Zacks’ proprietary methodology, stocks with a combination of a Zacks Rank #1 or 2 and a Growth Score of A or B offer solid investment opportunities.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.7% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>NetApp, Inc. (NTAP) : Free Stock Analysis Report

Western Digital Corporation (WDC) : Free Stock Analysis Report

Seagate Technology Holdings PLC (STX) : Free Stock Analysis Report

Pure Storage, Inc. (PSTG) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.