In October, Wall Street celebrated the two-year anniversary of the current bull market. Since this year began, the mature stock-driven Dow Jones Industrial Average (DJINDICES: ^DJI), benchmark S&P 500 (SNPINDEX: ^GSPC), and growth stock-powered Nasdaq Composite (NASDAQINDEX: ^IXIC) have respectively surged by 19%, 28%, and 31%, as of the closing bell on Dec. 4. They've also hit multiple all-time closing highs.

There's no singular catalyst behind this outperformance, but rather a combination of factors lifting Wall Street's sails. In no particular order, these catalysts include:

- The rise of artificial intelligence (AI), which, according to PwC in Sizing the Prize, could increase global gross domestic product by $15.7 trillion come 2030.

- Stock-split euphoria, with more than a dozen industry-leading businesses announcing or completing stock splits in 2024.

- Better-than-expected corporate earnings, which are fueling investor optimism.

- President-elect Donald Trump's November victory, which has Wall Street anticipating a lower corporate income tax rate and plenty of stock buybacks from America's most influential companies.

While things seemingly couldn't be better for Wall Street, history would like a word.

Image source: Getty Images.

The stock market has achieved this feat just three times in 153 years

For more than a year, there have been a couple of forecasting tools and predictive metrics signaling trouble for Wall Street and/or the U.S. economy. Examples have included the first sizable decline in U.S. M2 money supply since the Great Depression, and the longest yield-curve inversion in history, which has historically been a key ingredient for a U.S. recession.

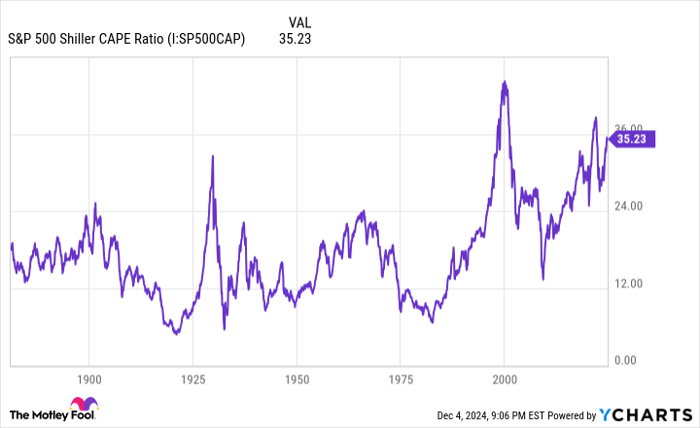

But the indicator that's the biggest harbinger of disaster for Wall Street just might be the S&P 500's Shiller price-to-earnings (P/E) ratio, which is also commonly referred to as the cyclically adjusted P/E ratio, or CAPE ratio.

Whether you've been investing for multiple decades or a few weeks, you're probably familiar with the traditional price-to-earnings (P/E) ratio, which divides a company's share price into its trailing 12-month earnings per share (EPS). This valuation tool provides a quick and concise way for investors to determine if a stock is respectively cheap or pricey when compared to its peers and the broader market.

While the P/E ratio has been around for ages, it does have its limitations. For instance, it doesn't factor in a company's growth potential, nor does it do a particularly good job during shock events. The traditional P/E ratio was pretty useless during the early stages of the COVID-19 pandemic, when most publicly traded companies were adversely affected by a historic demand cliff.

On the other hand, the S&P 500's Shiller P/E is based on average inflation-adjusted earnings from the prior 10 years. Because it accounts for a decade of earnings history, it's able to minimize the effect of shock events, which allows for more accurate valuation comparisons dating back to the early 1870s.

S&P 500 Shiller CAPE Ratio data by YCharts.

When the closing bell tolled on Dec. 4 (and the S&P 500 closed at a fresh record closing high), the S&P 500's Shiller P/E clocked in at 38.87. This marks the highest reading during the current bull market rally, and is more than double the 17.17 average for the Shiller P/E, when back-tested to January 1871.

Perhaps more importantly, this is only the third time in 153 years that the S&P 500's Shiller P/E has neared or topped 39. It briefly surpassed 40 during the first week of January 2022, which was subsequently followed by a bear market. In 2022, the Dow Jones Industrial Average, S&P 500, and Nasdaq Composite all shed more than 20% of their value on a peak-to-trough basis.

The only other time since 1871 that the Shiller P/E has been even higher occurred prior to the dot-com bubble bursting in December 1999, where it hit a peak of 44.19. When the internet bubble finally popped, the S&P 500 lost 49%, and the Nasdaq Composite tumbled 78% before reaching its nadir.

When back-tested to 1871, there are only six occurrences, including the present, where the S&P 500's Shiller P/E reached 30 during a bull market rally. All five prior instances were eventually followed by 20% to 89% plunges in one or more of Wall Street's major stock indexes.

Although the Shiller P/E isn't a timing tool -- stock valuations can remain extended for weeks, months, or even years -- it has flawlessly foreshadowed a major pullback in stocks for well over a century (when back-tested).

Image source: Getty Images.

Time is a pendulum that changes everything for investors

Admittedly, this isn't the rosiest of forecasts for Wall Street, and it probably isn't what investors want to hear. But the interesting thing about history is that it's a two-sided coin -- and those sides aren't necessarily the same.

For instance, neither working Americans nor investors look forward to recessions. The unemployment rate rises, wage growth slows or reverses, and stocks tend to perform poorly when the U.S. economy turns south. No amount of well-wishing can stop these normal and inevitable downturns within the economic cycle from occurring.

But at the same time, recessions are historically short-lived. Since World War II ended in September 1945, there have been 12 U.S. recessions, nine of which were resolved in less than a year. Of the remaining three, none endured longer than 18 months.

In comparison, a majority of the economic expansions since the end of World War II have lasted multiple years, including two periods of growth that stuck around for at least a decade. Although recessions and expansions are both part of the economic cycle, the economy spends a disproportionate amount of time growing, which is why corporate earnings tend to climb over the long run.

This same pendulum provides a favorable disparity between bear and bull markets on Wall Street, as well.

It's official. A new bull market is confirmed.

The S&P 500 is now up 20% from its 10/12/22 closing low. The prior bear market saw the index fall 25.4% over 282 days.

Read more at https://t.co/H4p1RcpfIn. pic.twitter.com/tnRz1wdonp-- Bespoke (@bespokeinvest) June 8, 2023

The data set you see above was posted on social media platform X by Bespoke Investment Group in June 2023. Though it's a bit dated, this data set illustrates the importance of time and perspective when investing on Wall Street.

Bespoke calculated the calendar-day length of every bear and bull market in the broad-based S&P 500 since the start of the Great Depression in September 1929. Altogether, this worked out to 27 separate bear and bull markets.

Whereas the average bear market has lasted just 286 calendar days (about 9.5 months) over a 94-year period, the typical S&P 500 bull market endured for 3.5 times as long (1,011 calendar days). It's also worth pointing out that more than half of all bull markets (14 out of 27, including the current bull market) have stuck around longer than the lengthiest bear market, which was 630 calendar days.

With time and proper perspective, even the direst of short-term forecasts can prove benign for long-term investors.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $376,143!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $46,028!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $494,999!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of December 2, 2024

Sean Williams has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.