Credit: Close-up of a social security card — Shutterstock

Credit: Close-up of a social security card — Shutterstock

At first blush, the idea of early retirement is thrilling. Stop giving your time to an employer before you're too old to fully enjoy the time you have left. Live every day you can on your terms. You can even start collecting Social Security payments at a relatively young 62!

Before you make that decision, however, you should know the price for calling it quits so much sooner than most of your peers will be surprisingly steep. Doing so could even translate into serious funding shortfalls in your golden years.

Here's a closer look at what retiring too soon could cost you.

Social Security's retirement benefit trade-off

There are exceptions to every rule. Your circumstances just might merit starting your Social Security benefits at the earliest possible age of 62.

By and large, though, it's a bad idea for most people. Let's look at why this is the case.

Image source: Getty Images.

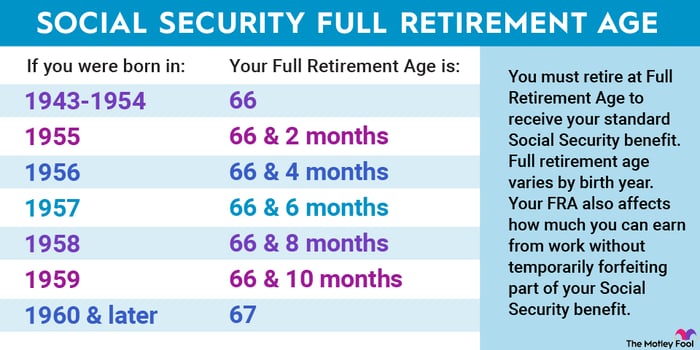

If you retire at your full retirement age (FRA), you'll receive 100% of the Social Security Administration's intended benefit payments. But what's your particular FRA? It's not the same for everyone, and the table below can help you figure out exactly what your FRA is, or will be in the future.

Data source: Social Security Administration.

With that context, as of the end of 2022, the average monthly check being cashed by 66-year-old retirees was about $1,720. Using that figure as a baseline, beginning payments at 62 years of age (with a FRA of 66) would translate into monthly checks of only around $1,290. That's in line with the Social Security Administration's 25% reduction in benefits for people starting their benefits four years before they reach their full retirement age. In absolute terms, that's a $430 reduction to your benefits every month. For many people, that's a significant change to their budget.

If you can afford to wait even longer, there's also an incentive to delay taking benefits past your FRA. Waiting until 70 years old to claim would see that $1,720 monthly benefit at FRA climb to $2,270, a difference of $550 every month. That's the result of the Social Security Administration's policy to increase benefits 8% annually (up to age 70) as an incentive for retirees postponing their payouts.

Keep in mind the FRA for most people alive today is 67. Below, you can see how their benefits change depending on when they start claiming Social Security.

Data source: Social Security Administration. Charles Schwab. Chart by author.

Just remember that while the people starting earlier payments will see smaller checks, they'll be collecting them for a longer period of time. Retirees waiting longer to begin their benefits will cash larger checks, but they'll do so for a shorter time.

Also keep in mind that the dollar figures above are just averages and/or estimates. Your actual range of choices could be higher or lower, depending on how much you earned while working. Nevertheless, the percentage reduction to your checks if you claim early is the same no matter how much you earned while working. The same goes for the percentage addition to your monthly benefit amount should you delay past FRA to start collecting.

Oh, and by the way, waiting beyond 70 years of age to start receiving Social Security checks doesn't add any extra benefit.

Think it through very carefully

Again, there could be good reason to initiate your Social Security retirement payments when you're 62 rather than waiting until you're 67, or even when you're 70. You might need the money much more right now, even if it means less per month. Your current and future health might necessitate beginning your benefits at 62 years of age, for instance.

On balance, though, starting to collect Social Security when you're 62 is an ill-advised idea for most retirees. People in reasonably good health well into their 60s are able to continue working at least until they reach FRA at 67. Indeed, many older workers report enjoying their jobs even more in their later years, perhaps because it's more about their contributions than the money they earn at that stage in their life.

If you need help hammering out how Social Security fits into your bigger retirement plan, check this out.

The $21,756 Social Security bonus most retirees completely overlook

If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $21,756 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after. Simply click here to discover how to learn more about these strategies.

The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.