As of January, more than 50 million retired workers were bringing home an average monthly Social Security benefit of $1,909. While Social Security checks aren't making retirees rich, they're helping to pull more than 15 million seniors aged 65 and over out of poverty each year.

Furthermore, an overwhelming majority of retirees lean on their monthly payout to make ends meet. More than two decades of annual surveys from national pollster Gallup have found that between 80% and 90% of then-current retirees need their Social Security benefit, in some capacity, to cover their expenses.

Considering how vital Social Security is to the financial foundation of aging Americans, there's arguably no event more anticipated each year than the cost-of-living adjustment (COLA) reveal by the Social Security Administration (SSA).

Image source: Getty Images.

What is Social Security's COLA, and how is it calculated?

Social Security's cost-of-living adjustment is best thought of as the tool used by the SSA to ensure beneficiaries don't lose purchasing power to inflation. This is to say that if a commonly purchased basket of goods and services increases in price, Social Security checks should, in an ideal world, rise by the same percentage to ensure beneficiaries can still buy those same goods and services. COLA is the mechanism designed to make that happen.

Before 1975, Social Security's COLAs were arbitrarily passed along by special sessions of Congress. In fact, beneficiaries went an entire decade in the 1940s before the very first COLA was passed in 1950. Since 1975, the program's COLA has been calculated annually using the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W).

The beauty of the CPI-W is that it has eight major spending categories and a boatload of subcategories, all of which have their own respective weightings. The advantage of everything having a specific weighting is that it allows the CPI-W to be whittled down to a single figure each month, which makes comparing month-over-month and year-over-year moves in the price of a large basket of goods and services a breeze.

What's unique about Social Security's COLA calculation is that it only factors in CPI-W readings from the third quarter (Q3) -- we're talking July through September. While the other nine months of the year are reported by the U.S. Bureau of Labor Statistics (BLS), they don't factor into the COLA calculation.

If the average CPI-W reading from Q3 of the current year is higher than the average CPI-W reading from Q3 in the previous year, inflation has occurred and beneficiaries will receive a larger payout in the upcoming year. The amount of the benefit increase is simply the year-over-year percentage difference in the average Q3 CPI-W readings, rounded to the nearest tenth of a percent.

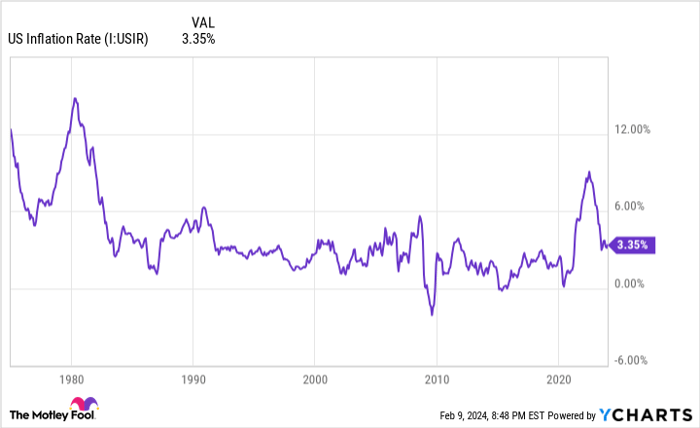

An elevated inflation rate has lifted Social Security's COLA for three consecutive years. US Inflation Rate data by YCharts.

Social Security's 2025 cost-of-living adjustment may have a silver lining

As you'll note, we're still quite a ways away from the period that actually matters for Social Security's COLA calculation. Nevertheless, the months that don't count toward the calculation can offer clues as to what beneficiaries can expect the following year.

The December inflation report, released by the BLS in mid-January, offers a potential silver lining for all 67 million-plus Social Security recipients.

Although the aggregate inflation rate has been declining since June 2022, an important component of both the CPI-W and Consumer Price Index for All Urban Consumers (CPI-U) has remained stubbornly high. In December, the unadjusted 12-month inflation rate for shelter was a scorching-hot 6.2% for the CPI-U. The CPI-U is a similar inflationary measure to the CPI-W, and shelter is the highest-weighted expense category for both indexes.

The Federal Reserve's most aggressive rate-hiking cycle in over four decades has sent mortgage rates soaring after a period of historically low lending rates. The end result has been fewer existing homes on the market for sale and considerable rental pricing power for landlords. As long as shelter prices remain elevated, I believe there's a good chance Social Security's 2025 COLA will come in higher than the 2.6% average over the past 20 years.

For what it's worth, the CPI-W rose by 3.3% over the past 12 months, as of December 2023. If, hypothetically speaking, Social Security's 2025 cost-of-living adjustment settles around 3% during the third quarter, the average retired-worker benefit would rise by close to $60 per month in the upcoming year.

Image source: Getty Images.

There's potential bad news, too

Following a period of lackluster cost-of-living adjustments between 2010 and 2021, which saw three years where no COLA was passed along, as well as a fourth where benefit checks rose by a meager 0.3%, a fourth consecutive year of above-average COLAs in 2025 would be a welcome sight. Unfortunately, it won't be free from negative repercussions.

Although historically high shelter inflation is what could juice the program's COLA in 2025, shelter is one of the two major expenses (medical care being the other) that accounts for a higher percentage of monthly expenditures for seniors than working-age Americans. In other words, if the inflation rate for shelter remains stubbornly high, the purchasing power for retired workers would be expected to decline, even if the 2025 COLA comes in above its average over the past two decades.

The unpleasant reality for seniors is that the purchasing power of a Social Security dollar has been plunging since this century began.

In May 2023, The Senior Citizens League (TSCL), a nonpartisan senior advocacy group, released a study that examined this steady loss of purchasing power. Whereas aggregate cost-of-living adjustments between January 2000 and February 2023 rose by 78%, the cost for a typical basket of goods and services purchased by the average retiree jumped by 141.4% over the same timeline. According to TSCL, the purchasing power of Social Security income for seniors has declined by 36% since 2000.

The culprit for this steady erosion is the CPI-W. As its full name shows, it's an index focused on the spending habits of "urban wage earners and clerical workers." These are predominantly working-age Americans, few of which are currently receiving a Social Security benefit.

Meanwhile, well over 80% of existing beneficiaries are aged 62 and above. Seniors spend their money quite differently than working-age Americans. As a result, the CPI-W isn't adequately factoring in the expenses that matter most to retired workers, such as shelter and medical care.

While lawmakers on both sides of the political aisle agree that the CPI-W isn't doing a particularly good job, finding a fix has proved challenging. Democrats and Republicans have both proposed workable solutions, but their respective measures of inflation come from opposite ends of the spectrum. With bipartisan cooperation on Social Security virtually nonexistent in Congress, there's little hope for diminishing this loss of purchasing power anytime soon.

The $22,924 Social Security bonus most retirees completely overlook

If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $22,924 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after. Simply click here to discover how to learn more about these strategies.

View the "Social Security secrets"

The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.