News & Insights

In a recent study, we noticed that options liquidity is concentrated close to expiry as traders close out and roll, instead of taking delivery, on expiring positions.

However, for a hedger, that creates problems (as we show in today’s charts).

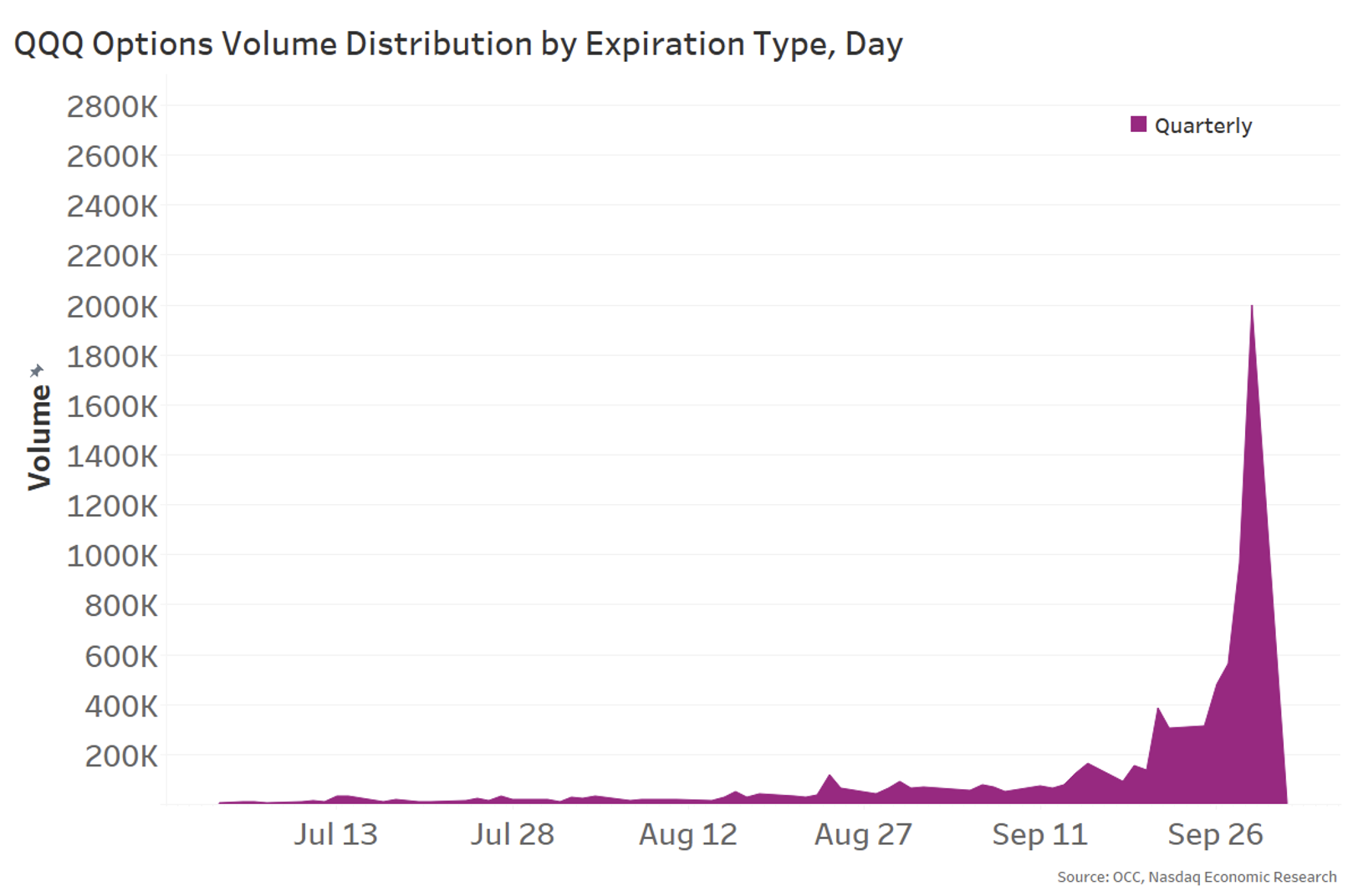

Options liquidity comes in cycles

As shown below, when we look at trading in quarterly-expiring options (which expire at the end of every third month), liquidity is quite seasonal, with a large amount of total trading occurring in the week around expiry. The problem for a hedger is not much liquidity is available at other times of the quarter.

Chart 1: Liquidity in Quarterly options over the course of a quarter

That could be a problem for natural investors, who have cash flows throughout the quarter, or hedgers who want to protect portfolios for specific event risks.

Monthly options introduce more liquidity cycles

The addition of monthly options solves some of those problems.

First, with the introduction of three more expiries per quarter in the middle of each month, those expiries complement the quarterly cycle, which ends at the end of each quarter. As the chart below shows, over the whole quarter, there is a stronger level of underlying liquidity on every day in the quarter.

Second, by introducing more frequent expiries, hedgers are better able to match their position insurance to their cash flow needs. That helps them avoid buying and then selling options with a lot of time value (theta), a less perfect hedge of underlying position movements.

Chart 2: Options with monthly expirations complement quarterly options liquidity

Weekly options smooth the liquidity across the whole year

Weekly options smooth the liquidity cycle out even more. That allows options market makers to more easily use one option to hedge other options (letting “Greeks” like time value and re-hedging requirements offset). The options ecosystem is then allowed to become a hedge for itself – rather than requiring every options trade to be hedged into underlying stocks and re-hedged as underlying prices change.

Chart 3: Adding all weeklies smooths liquidity available throughout the quarter

For investors needing beta hedges, non-Friday weekly options (those that expire on Monday through Thursday) exist for Nasdaq-100 and S&P 500 exposures (in ETF or Index underlying), creating deep and consistent liquidity over those index underlyers on every day of the week.

And based on the open interest in these options, which builds in the three weeks prior to expiry, there are a number of investors who need to match hedges to non-Friday cashflows.

More frequent options expiries are good for liquidity

As we’ve seen already, expiry date has always been more liquid – and that’s because many investors don’t want to have to exercise, or see out-of-the-money options expire. Many will roll positions to retain their insurance or yield enhancement strategies.

Because of that, adding more frequent expiries has increased overall liquidity.

As today’s charts show, additional expiration cycles have also reduced the seasonality of options liquidity. That, in turn, helps options market makers hedge one option with another option, which would reduce the amount of hedging into stocks that needs to be done — saving them crossing spreads. It could also reduce the delta-hedging required at the end of each day.

But that sounds like a study for another time.

Latest articles

This data feed is not available at this time.

Data is currently not available

Market Makers Newsletter

Sign up for our newsletter to get the latest on the transformative forces shaping the global economy, delivered every Thursday.