For decades, investors have turned to Warren-Buffett-led Berkshire Hathaway for ideas, his sentiment on the market, and top stocks to buy.

Berkshire has been a net seller of stocks in 2024 -- amassing a record-high $325 billion cash position. But Berkshire's fifth- and sixth-largest holdings remain the same.

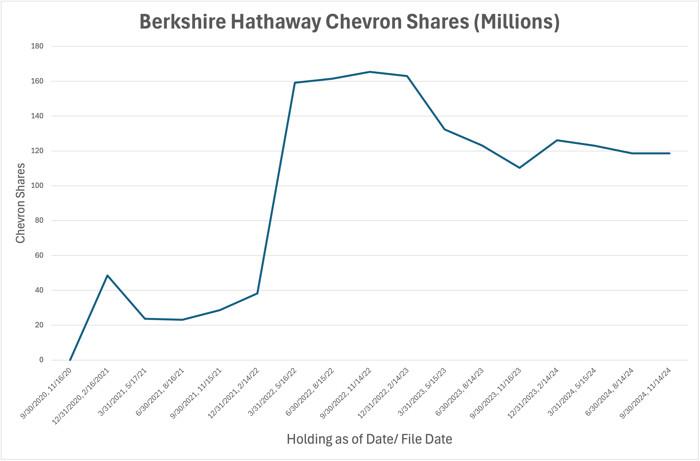

Berkshire owns $19.07 billion of Chevron (NYSE: CVX) stock, giving it 6.6% ownership. It also owns $13 billion in Occidental Petroleum (NYSE: OXY) stock, representing a 27.2% stake.

Here's Berkshire's background in each company and which dividend stock is the better buy now.

Image source: Getty Images.

A highly reliable energy stock for generating passive income

Chevron is an integrated oil and gas major and one of the world's most valuable non-nationalized energy companies. Berkshire began building a stake in early 2021, but the real jump came in the first quarter of 2022.

Data source: Berkshire Hathaway SEC Filings.

Except for a noteworthy sale in the first quarter of 2023, Chevron has remained a key holding for Berkshire and a notable exception to the selling spree in Apple, Bank of America, and other top holdings in 2024.

Chevron remains one of the best oil and gas dividend stocks to buy now, even with West Texas Intermediate crude oil prices below $70 a barrel. Chevron has invested in quality over quantity, giving it a diversified asset portfolio that can break even at lower oil prices. For example, around 75% of Chevron's locations can break even below $50 per barrel -- giving Chevron a sizable margin of error even compared to current oil prices.

Chevron has paid and raised its dividend for 37 consecutive years. Its most recent raise was 8%, which it announced in February. In addition to paying a boatload of dividends, Chevron generates plenty of capital to reinvest in the business and repurchase stock.

To top it all off, Chevron has an elite balance sheet with very low leverage. Chevron further strengthened its balance sheet earlier this fall by selling its Canadian assets to Canadian Natural Resources for $6.5 billion.

A bolder bet on higher oil prices

Berkshire's history in Occidental Petroleum, commonly known as Oxy, dates back to 2019 when Berkshire helped Oxy fund the purchase of fellow exploration and production (E&P) company Anadarko Petroleum. The deal gave Berkshire 100,000 shares of preferred stock valued at $100,000 per share with an 8% annual dividend and a warrant to purchase up to 80 million more shares at $62.50 per share.

Since then, Berkshire has bought more Oxy stock, bringing its position to a 27.5% stake in the company. But Berkshire could own much more if it exercised its warrants.

Oxy paid top dollar for Anadarko in 2019, coincidentally outbidding Chevron. Because of the deal, Oxy entered the oil and gas downturn of 2020 overleveraged and saw its stock price fall to single digits. But the subsequent boom in 2021 and 2022 was a huge win for Oxy, which was able to pay down debt thanks to higher oil prices. Then, in late 2023, Oxy announced that it would acquire CrownRock L.P. to boost its Permian Basin exposure further. It closed the deal on Aug. 1, 2024.

Although the deal made Oxy, once again, more leveraged, it could pay off as long as oil prices remain around current levels. Oxy's latest quarter showed strong results, plenty of free cash flow, and a path toward paying down debt. Despite the good quarter, Oxy's stock price remains just a few percentage points off its 52-week low, which makes sense given oil prices are also around a 52-week low.

Betting on quality

Oxy is a much higher risk, higher potential reward play than Chevron because it is an E&P rather than an integrated major. The vast majority of its portfolio is in one region -- the Permian Basin. It also doesn't have a balance sheet as strong as Chevron's. In 2020, Oxy slashed its dividend to just $0.01 per share per quarter. It has since brought it back up to $0.22, but the dividend isn't nearly as reliable as Chevron's. Chevron also has a higher yield at 4% compared to 1.8% for Oxy.

Oxy would be stretched thin if oil prices tanked and could cut its dividend again, whereas Chevron's superior financial health would allow it to support its dividend even if its cash flow was negative in the short term. All told, Chevron is a better all-around buy than Oxy, but Oxy will likely outperform Chevron if oil prices go up because it has more to gain.

Should you invest $1,000 in Chevron right now?

Before you buy stock in Chevron, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Chevron wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $869,885!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of November 25, 2024

Bank of America is an advertising partner of Motley Fool Money. Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple, Bank of America, Berkshire Hathaway, and Chevron. The Motley Fool recommends Canadian Natural Resources and Occidental Petroleum. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.