Investors might be wondering how the results of the 2024 election will affect Taiwan Semiconductor Manufacturing (TSMC) (NYSE: TSM). As the world's largest and most advanced semiconductor producer, it is one of the most critical companies in an important industry.

However, the incoming Trump administration has emphasized an increasing need for domestic manufacturing. Hence, the election results could also make it a target. Thus, chip stock investors should probably contemplate whether they should buy before the Jan. 20 inauguration.

TSMC's political situation

TSMC is in a geopolitically sensitive situation. China has targeted the company's home country for takeover in a political battle predating the existence of the semiconductor industry. Today, the ramifications of that dispute affect the entire globe since approximately two-thirds of all chip production takes place in Taiwan.

According to a study by the Semiconductor Industry Association (SIA), only about 12% of chip manufacturing took place in the U.S. in 2020, down from around 40% in 1990. This situation was concerning enough that the Biden administration approved almost $53 billion in chip manufacturing subsidies through the CHIPS Act.

TSMC is about to open a facility in Arizona, but its fabs there are set to cover just under 4% of the company's total production. That is likely not enough domestic production to appease an administration wanting to return the U.S. to its former glory as a manufacturer.

Why TSMC may benefit anyway

Despite those political concerns, U.S. companies may continue to buy from TSMC for one critical reason: They have no choice.

Taiwan claims approximately 92% of all wafer production capacity for the most advanced chips, according to the SIA. The most advanced technology depends on these chips, including many desired artificial intelligence (AI) applications. Hence, not buying from Taiwan would mean the U.S. falls behind technologically.

Other companies may only offer the administration limited help. Samsung and Intel are building fabs in the U.S. Like TSMC, they will rely on the most advanced extreme ultraviolet lithography (EUV) machines from ASML. However, TSMC has maintained its technical lead even over companies with the same EUV machines, which will probably force chip companies and governments to continue dealing with TSMC.

Also, ramping up production capacity is a years-long process. Samsung does not expect production to begin at its fab in Texas until 2026, while Intel will likely not begin making chips in Ohio until 2027 or 2028. Thus, the Trump administration will probably have to accept the industry's current situation for now.

Furthermore, investors have some incentive to invest in TSMC stock despite these risks. In the first nine months of 2024, revenue of $63 billion surged 32% higher compared to the same period in 2023. Also, the company slowed its operating expense growth relative to revenue. That meant the company's $25 billion in net income attributable to shareholders rose 33% from year-ago levels.

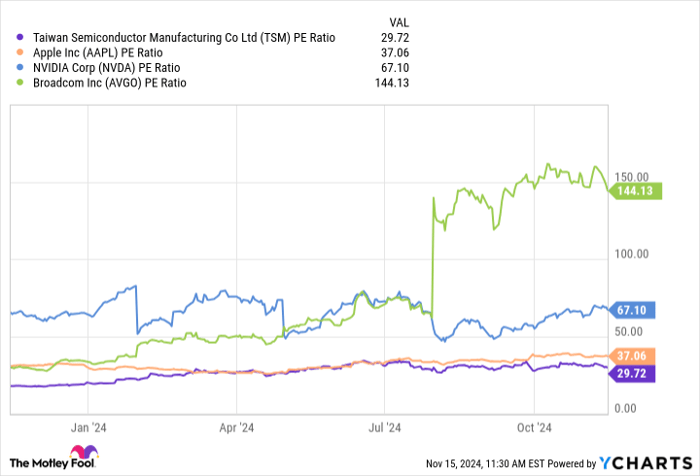

Amid that profit growth, TSMC's P/E ratio is 30, a lower earnings multiple than its three largest customers, Apple, Nvidia, and Broadcom. That could make the stock attractive to some investors despite the risks.

TSM PE Ratio data by YCharts

Should investors buy TSMC stock before Jan. 20?

Ultimately, TSMC stock remains a likely buy before Jan. 20.

Indeed, a Trump administration will want more manufacturing in the U.S., which may seem unfavorable to TSMC.

However, TSMC is so indispensable to the tech industry and, by extension, the world economy, that political forces will probably not sweep this company to the sidelines. Even if a company matched or surpassed TSMC, it would take years to build the fabs needed to meet any potential production goal.

Finally, the stock trades at a discount to its largest clients. Thus, TSMC stock is a likely winner for investors regardless of how an incoming administration may feel about the company.

Should you invest $1,000 in Taiwan Semiconductor Manufacturing right now?

Before you buy stock in Taiwan Semiconductor Manufacturing, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Taiwan Semiconductor Manufacturing wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $870,068!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of November 18, 2024

Will Healy has positions in Intel. The Motley Fool has positions in and recommends ASML, Apple, Intel, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom and recommends the following options: short November 2024 $24 calls on Intel. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.