Get ready everyone, we are officially entering the meat of this quarter's earnings season. Alphabet (NASDAQ: GOOG) -- parent company of Google and YouTube -- is set to report earnings after the closing bell on Oct. 29. The company is in a complicated position at the moment. On the one hand, profits have never been higher. On the other hand, it is in the throes of multiple monopoly lawsuits and is seeing an onslaught of competition from artificial intelligence (AI) start-ups.

Alphabet stock has fallen 14.6% from highs set just a few months ago. Should you take the opportunity to buy the dip on the stock before Q3 earnings are released?

Google Search market share

For years, investors and start-ups thought it was impossible to compete with Google Search. The company had a virtual monopoly in search engines (greater than 90% market share) and an immense war chest to push out any small competitors.

That all changed when OpenAI released ChatGPT. Fueled by an investment from Microsoft (Google Search's biggest competitor), ChatGPT quickly grew to over 100 million users with its advanced language model and search features. In the wake of this growth, dozens of other start-ups have been formed to try and tackle the search monopoly. So far, Google has been able to retain its market share fairly well, with an estimated 90% share across all platforms. However, it is losing a bit of ground on desktops, where Microsoft has an operating system advantage and is pushing the Bing/ChatGPT search engine onto users. Google's market share is estimated to have fallen to under 80% on desktops, although this segment is getting less important every year.

Google is also facing charges from the Department of Justice (DOJ) in the United States, which wants to break its monopoly. It is hoping -- depending on if the lawsuits hold up in court -- to stop its distribution payments to companies like Apple, using its data to build a monopoly, and create competition in search-based text advertising. Stopping payments to Apple is straightforward, but it is unclear how the DOJ will enact these other remedies.

Even with all these news headlines and worries about competition, Alphabet's overall revenue and profits keep soaring, mostly driven by Google Search. Last quarter, Google Search revenue grew to $48.5 billion compared to $42.7 billion in the same period a year prior. If the competition is coming for Google, it hasn't shown up in the financials yet.

Watch the Google Cloud division closely

The fastest-growing division for Alphabet is Google Cloud. The cloud infrastructure provider is benefiting greatly from the booming demand for AI products, which require tons of spending on the cloud. Segment revenue grew 29% year over year last quarter to $10.3 billion. That is an annualized run rate of over $40 billion. Just a few years ago in 2020, Google Cloud quarterly revenue was only $3 billion.

As the division scales, it is getting much more profitable as well. Google Cloud operating income was over $1 billion last quarter. With the general tailwind from the transition to cloud computing still at its back, Google Cloud can easily grow to $100 billion in annual revenue within the next five years. If profit margins can expand to 20%, that is $20 billion in future annual earnings from this once-tiny division within the Alphabet empire.

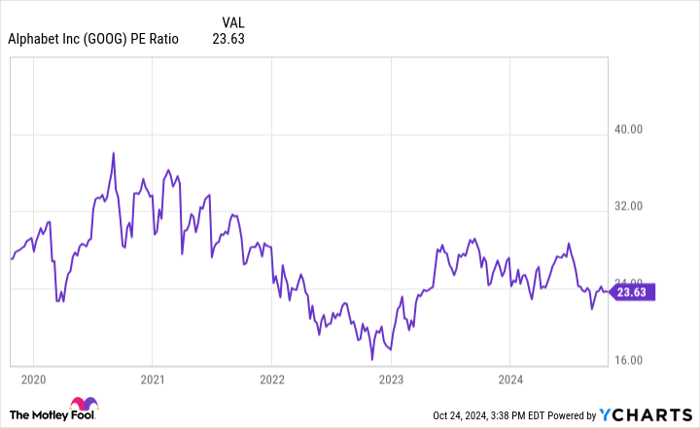

GOOG PE Ratio data by YCharts

Should you buy the stock?

The headlines for Alphabet look scary. The stock has reacted to these headlines, with shares down around 15% from highs put in earlier in 2024.

However, if we look at the company's underlying financial performance, it is still performing at a high level. Google Search and Google Cloud keep putting up strong growth figures, and we haven't even talked about YouTube or Waymo. The company currently has an operating margin of around 30%, which should expand as Google Cloud continues to scale up. Management keeps buying back stock and reducing shares outstanding, which will help earnings per share (EPS) grow over the long term.

After the drawdown, Alphabet stock now trades at a price-to-earnings ratio (P/E) of 23.5. This is well below the S&P 500 of 30. Alphabet can grow EPS at a faster rate than the index. When put in this perspective, the stock looks like an easy buy before Q3 earnings on Oct. 29.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,154!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,777!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $406,992!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 21, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool's board of directors. Brett Schafer has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet, Apple, and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.