Sally Beauty Holdings, Inc. SBH benefits from strength in its strategic growth pillars. The company’s growing e-commerce business is worth mentioning. Sally Beauty is focused on undertaking prudent buyouts to drive growth. Encouragingly, management expects fiscal 2022 net sales growth of 3-4% year over year. The gross margin is likely to expand 40-60 basis points year over year in fiscal 2022.

However, the beauty products provider is not immune to high costs. Let’s discuss.

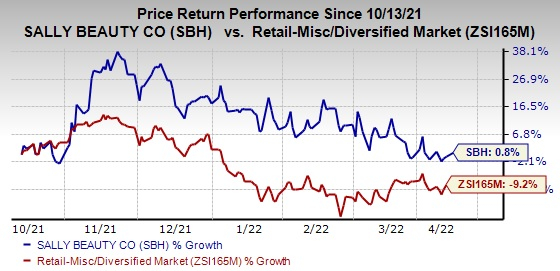

Image Source: Zacks Investment Research

What’s Favoring Sally Beauty?

Sally Beauty is focused on its four strategic growth pillars to boost the fiscal 2022 top line. These include leveraging the digital platform, driving loyalty and personalization, undertaking product innovation and enhancing the supply chain. In this regard, the company is making progress in loyalty and personalization. In its lastearnings call management highlighted that almost 75% of sales at Sally, the United States and Canada were from loyalty programs in the first quarter of fiscal 2022. The company has an impressive innovation pipeline, which is slated for fiscal 2022. Sally Beauty is focused on building an automated, integrated supply chain network. During the call, management highlighted that its JDA implementation is in the final phase.

Sally Beauty is undertaking efforts to augment its online business. Robust investments to enhance the digital space have been yielding. In the fiscal first quarter, the company’s e-commerce sales increased 22% year over year, driven by the Beauty Systems Group’s (BSG) refreshed e-commerce platform. Global e-commerce sales contributed 8.3% to net sales during the quarter. The company’s Sally U.S. and Canada stores contributed 35% to e-commerce sales, with Buy Online, Pick Up In-Store (BOPIS) contributing 19%, rapid two-hour delivery representing 10% and ship-from-store accounting 6%. Management believes its e-commerce business will reach 15% or more of total sales in the next few years.

Sally Beauty intends to strengthen its business on the back of strategic acquisitions. In September 2020, Sally Beauty’s subsidiary BSG acquired La Maison Ami-Co Inc. — a professional beauty products distributor in the Canadian province of Quebec. Per the deal, Sally Beauty acquired 10 La Maison Ami-Co stores. This transaction added 17 direct sales consultants and exclusive distribution rights of leading professional hair color and hair care brands like Wella Professional, Oribe and Goldwell across Quebec. The deal augments its business in Quebec along with increasing the reach of BSG’s professional beauty products in its Chalut store network as well as full-service business.

Hurdles on the Way

Sally Beauty has been grappling with escalated selling, general and administrative (SG&A) expenses for a while. During the first quarter of fiscal 2022, the company reported SG&A expenses of $386.3 million, up $20.1 million. The upside can be attributed to higher labor costs, escalated expenses from international markets associated with re-opening and planned marketing investments. As a percentage of sales, SG&A expenses came in at 39.4%, up from 39.1% reported in the year-ago quarter.

Nonetheless, we believe that the aforementioned upsides are likely to keep Sally Beauty going. Shares of the Zacks Rank #3 (Hold) company have gained 0.8% in the past six months against the industry’s 9.2% decline.

Hot Retail Bets

Some better-ranked stocks are Tractor Supply Company TSCO, Build-A-Bear Workshop, Inc. BBW and Target Corporation TGT

Tractor Supply Company, a rural lifestyle retailer in the United States, carries a Zacks Rank #2 (Buy). TSCO has a trailing four-quarter earnings surprise of 22%, on average. Tractor Supply has an expected earnings per share (EPS) growth rate of 9.8% for three to five years. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Tractor Supply Company’s current financial year sales and EPS suggests growth of 8.1% and 8.9%, respectively, from the year-ago period.

Build-A-Bear, a multi-channel retailer of plush animals and related products, currently carries a Zacks Rank #2. BBW has a trailing four-quarter earnings surprise of 214.3%, on average.

The Zacks Consensus Estimate for Build-A-Bear's current financial-year sales and EPS suggests growth of 9.8% and 9.7%, respectively, from the year-ago period's reported figures.

Target, a general merchandise retailer, carries a Zacks Rank #2 at present. TGT has a trailing four-quarter earnings surprise of 21.3%, on average. Target has an expected EPS growth rate of 16.5% for three to five years.

The Zacks Consensus Estimate for Target’s current financial year sales and EPS suggests growth of 3.5% and 6.7%, respectively, from the year-ago period.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +25.4% per year. So be sure to give these hand-picked 7 your immediate attention.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Target Corporation (TGT): Free Stock Analysis Report

Tractor Supply Company (TSCO): Free Stock Analysis Report

Sally Beauty Holdings, Inc. (SBH): Free Stock Analysis Report

BuildABear Workshop, Inc. (BBW): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.