Credit:

Credit: By David Qian Zhang :

Introduction

With great size comes great economy of scale. However, large countries tend to suffer when they have to transform economically, because most workers who wish to participate in a large country's economic upgrade can not do so concurrently. Therefore, policies behind China's economic reform from manufacturing/export-driven to services/consumption-driven have been slow, variegated, and targeted to prevent instability (as described here ). One key question in this transformative journey is whether its monetary system should converge to the international monetary system, where major developed economies operate on free capital flow, independent monetary policy (if the European Union could been seen as one economic entity), and a fully floating exchange rate (as opposed to a managed floating or fixed exchange rate). After setting the institutional backdrop for China's current monetary system, we will explore how soon the RMB will float fully, whether capital will flow freely, and how volatile the RMB may become.

People's Bank of China (PBOC) and Monetary Policy

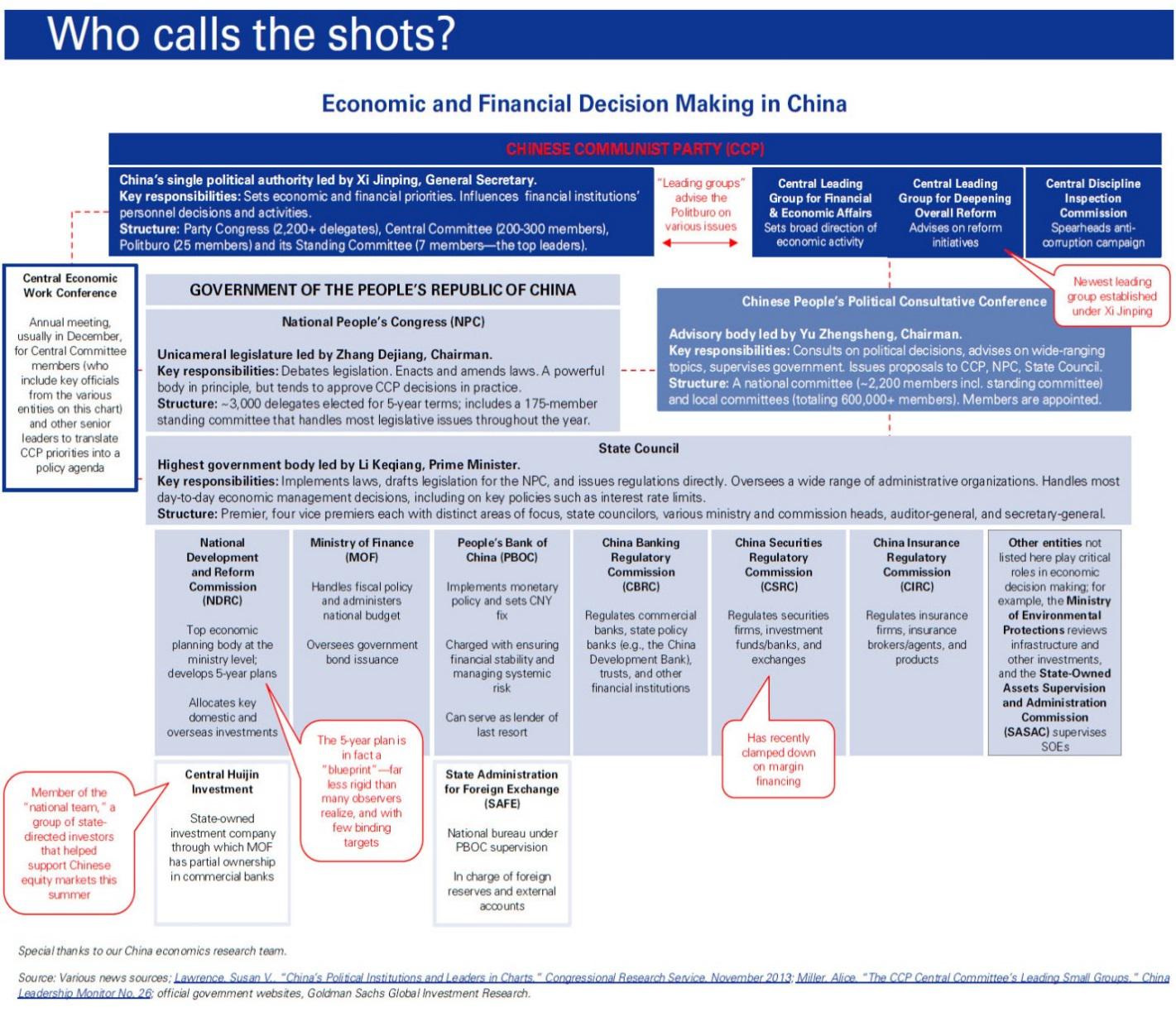

Founded in 1948, the PBOC became a modern central bank that orchestrates monetary policy while achieving currency stability in 1983. Unlike most central banks in developed markets, the PBOC reports to the State Council (see graph from Goldman Sachs below), equivalent to China's cabinet, and is essentially a policy executor. Historically, the PBOC set policy rates through 1+ year deposit rates as opposed to short-term interbank rate (like the Fed Funds overnight rate or the ECB's 7 day refinance rate) that indirectly affects longer term rates. In addition to setting the price of money through deposit rates, the PBOC also sets the quantity of money through the Required Reserve Ratio. These two main tools are becoming obsolete. There will be less need to rein in excessive RMB liquidity caused by the PBOC's sterilization of FX reserves (i.e. PBOC taking USD from exporters in exchange for RMB or RMB government bonds) as China shuns exports and liberalizes interest rates (i.e. let interest rates rise to market-determined levels). Going forward, open market operations and discount window mechanisms will help to set China's discount curve. Having a market-driven risk-free discount curve is a prerequisite for efficient asset pricing, especially for a market-based exchange rate that depends on, among other factors, international interest rate differentials.

Since China's central bank operates with guidance from the State, it's no surprise that its governor is appointed by President Xi. What is surprising, however, is that Xiaochuan Zhou, the PBOC Governor, was not among the 205 most powerful Central Committee members selected from the Chinese Communist Party in 2012. Ironically, this striking omission reflects less on the PBOC's independence from the State, and more on the State's intention to keep the PBOC as a policy executor as opposed to a policy maker. Similarly, PBOC's monetary policy committee is more of an advisory committee and less of a policy making committee such as the Fed's FOMC. In addition to Zhou and two other PBOC officials, it includes those from other government branches, academia, and regulatory agencies, with no strict rules on the number, composition, and terms of the committee members. While most do not carry extensive international educational and professional backgrounds, the three academic advisors appointed in 2015 lends some fresh air. Among them, two carry PhD's from foreign institutions, and one even has extensive experiences at two international bulge-bracket banks. The diverse experiences of these new academic advisors bode well for the internationalization of china's monetary system, albeit at a measured pace.

Benefits of a Fully Floating RMB?

By maintaining an artificially weak RMB through buying up foreign currencies, China has accumulated $3.3 Trillion of FX reserves (see chart below from tradingeconomics.com) while issuing government bonds that eventually reached more than 50% of GDP (see chart from McKinsey below). By relying less on a weak currency and FX reserves, the PBOC can pay a higher return to its domestic government bond holders while maintaining a more positive and thus sustainable return itself. It could also immunize itself somewhat from monetary policy spillovers from the US, which tends to export excessive capital to emerging markets during monetary easing and disrupt growth when capital flows out during monetary tightening. For example, whenever the USD weakens due to the Fed's easing, stronger currencies in China and other high-growth countries will limit inflationary pressures. Policy impact could also run in the reverse direction as seen after the RMB devalued by 3% in 2 days in August of 2015, which immediately lessened the chance of a Fed rate hike as implicitly referenced by "recent global economic and financial developments" in the September 2015 FOMC statement.

Aside from long-term monetary independence, floating the RMB during an economic slowdown provides further upsides. First, by not having to shore up the RMB with FX reserves, the PBOC is not inadvertently tightening monetary conditions when it sells foreign currencies and buys RMB, because there will be less RMB and thus less liquidity in the market place. Second, when the RMB depreciates via market forces, the vast amount of FX reserves that the PBOC carries appreciate. Third, if the PBOC devalues the RMB one time by 10-15% (either directly or indirectly by abolishing the 3% daily trading band) before fully floating it as suggested by Yongding Yu , an ex-monetary committee member, then pressure for further depreciation and capital outflow may subside. And fourth, at 16% of M2 money supply, a figure lower than the amount carried by crisis-ridden countries at the time of the 1997 Asian Financial Crisis, FX reserves in China may not be enough to conduct currency intervention and to pay off $1.1 Trillion of external liabilities ( of which $0.7 Trillion are international bank loans and $0.4 Trillion are bond issuances ).

Will the RMB Flow Freely?

As reported by the Wall Street Journal in December 2015, Yi Gang, deputy governor of PBOC, said that moving from a managed floating RMB to a fully floating RMB is a long-term goal. However, whether capital should flow freely is still debatable. As mentioned by PBOC governor Zhou in April 2015 at an IMF meeting, "China will adopt a concept of managed convertibility." Specifically, it will retain control when faced with the following: illegal transactions, excessive external debt, short-term speculative capital, and deteriorating balance of payments.

Due to overwhelming benefits of a floating currency as mentioned earlier, China is incentivized to float its currency while controlling capital flow and monetary policy. As suggested by IMF researchers , "countries appear to have better medium-term outcomes if they introduce exchange rate flexibility before fully liberalizing their capital account, especially if there are weaknesses in the financial sector". This is very much the case in China, where non-performing loans in the large state-owned banks spurred by the 2008 fiscal stimulus undermined their price to asset ratios to less than one. Letting the RMB float fully without flowing freely will not help the RMB reach its market equilibrium. Therefore, the RMB will have to float fully and flow freely around the same time to achieve stability.

Furthermore, due to a small off-shore RMB bond market (less than $70 Billion in 2014 as seen below from Fitch Ratings) and an underdeveloped on-shore RMB government bond market (less than 50% of GDP as seen below from IMF) that limits foreign bond investor participation, China will have a hard time attracting capital inflow even in the case of a fully floating and freely flowing RMB. To battle the latest wave of massive capital outflow, the Chinese government has progressively set inbound investment quota to be greater than outbound quota since 2013 (see chart below from Gavekal). It also recently imposed a $5000 daily limit on top of the $50,000 that Chinese residents can exchange to USD per year. Such temporary patches are designed to buy more time for China to shore up its domestic capital markets in order to attract more capital inflow on balance.

Next Steps in Floating the RMB?

A reliable short-term interest rate benchmark leads to stable short-term interest rates, which is highly correlated with volatility of exchange rates (see chart below from Michael Zhu). China's fully floating currency volatility may be as high as 20% when the positive relationship between currency volatility and short-term interest rate volatility is extrapolated (see chart below from Michael Zhu). Therefore, the PBOC needs to roll out new target policy rates that determine short-term interest rates in a more stable manner.

A working paper published by PBOC's chief economist Jun Ma in November 2015 suggested an interest rate corridor that will take several years to implement. The floor will be based on interest on excess reserves (IOER, similar to the same term at the Fed and deposit facility at the ECB), while the ceiling will be administered by the short-term Standing Lending Facility (SLF, similar to Marginal Lending Facility at the ECB and the Discount Window at the Fed). In contrast, IOER in the US is used as a ceiling during the current Fed Funds rate hike cycle due to excessive bank reserves on the Fed's balance sheet. Reverse Repos are currently used to floor the Fed Funds Rate due to the unavailability of IOER to non-depository institutions such as Government Sponsored Entities and money market funds.

Besides missing stable monetary policy tools, economic conditions are also not ripe for a fully floating exchange rate. This is shown by the recent weakness of the managed floating off-shore (i.e. accessible to foreign capital) USDCNH exchange rate (yellow line below) relative to the more centrally determined on-shore USDCNY exchange rate (white line below) after the August 11th devaluation. As mentioned by IMF researchers , moving to a floating regime is "best accomplished during a period of relative tranquility in exchange markets…a next-best set of circumstances is when the domestic economy is strong and pressures are for an appreciation of the currency". However, by letting the overnight HIBOR rise to 66% in recent days, the Chinese government has quelled near-term speculation of further divergence between CNH and CNY (seen green line below).

How Volatile Will the RMB Become?

Besides keeping a close hand on the offshore CNH, the PBOC is also planning ahead for a more stable and fully floating RMB. Within 2 weeks of RMB's acceptance into the IMF SDR in November 2015, the PBOC timely introduced a 13 currency basket that essentially tracks the RMB relative to a pseudo-SDR (Special Drawing Rights) basket. Because the USD is only 26% in this pseudo-SDR basket (see below from Money Morning) instead of 42% in the IMF SDR or 100% in the RMB-USD peg, the RMB can potentially decouple (although a basket reference alone can not prevent speculative attacks or natural imbalances) from USD's current bullish trend and thus mitigate a hard landing scenario in China. In the long run, it also provides developing market economies a second global reserve currency that is more stable than the USD and more practically used than the 5 currency-based SDR from the IMF. Seventy years after John Keynes advocated the commodity-based Bancor and 6 years after PBOC Governor Zhou advocated the SDR (as described here ), China is quietly turning the RMB into an SDR-like currency. At almost half of the world's GDP, developing economies are not only offered a seat in the current international monetary system through the RMB, but also on the verge of a new monetary system that runs on a more stable basket-pegged RMB.

Conclusion

As gestured by its December 2015 13-currency basket peg announcement, China has found an anchor and excuse to depreciate the RMB relative to USD. When the RMB moves, emerging market currencies follow shortly via herding effect in monetary policy, developed market currencies respond via trade and portfolio flows, and so do worldwide commodity, equity, and bond markets. While opportunities may outweigh threats in becoming a fully floating currency, a stable RMB would necessitate a large and open bond market to accommodate capital inflows and stable monetary policy tools such as the interest rate corridor. In conjunction with an SDR-like currency peg, the PBOC may just have enough tools to achieve a fully floating and stable currency in a few years. But due to uncertainties of an economic transformation for a large country, expect some zig-zag policies in China's new monetary system.

Bonus Section(Will the HKD re-peg from USD to the RMB?)

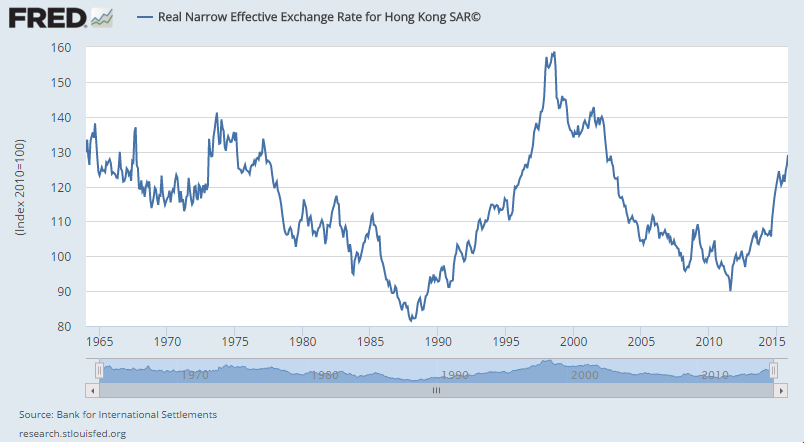

On January 15th 2016, the Hong Kong Monetary Authority reiterated its intention to keep the 7.8 HKD to 1 USD peg since it was first introduced in 1983. Coincidentally, it also marks the one year anniversary of the SNB's surprise dismissal of the Swiss Franc ceiling due to the inability of a small economy to print its way to a weaker currency. Such official reassurances are usually contrarian signals according to George Soros. Furthermore, Hong Kong's FX reserves relative to M2 is about 22%, not much higher than China's 16%. Therefore, one can not help but to wonder if the HKD may also experience a widely unexpected one-time sharp devaluation followed by a re-peg from USD to RMB (as Bill Ackman speculated in 2012 ).

Hong Kong, being a small economy, is susceptible to volatile trade flows. It has to eventually re-peg from USD to RMB, as the US runs on a separate economic/monetary policy cycle. A strong correlation (see chart below) between sharp movements in HKD and CNH reflects the market's fear that the HKD may also devalue relative to the USD, especially since HKD's effective exchange rate is approaching a 13 year high (see chart below). A one-time devaluation enroute to a re-peg to the RMB may keep the HKD stable on a trade-weighted basis. More importantly, it may serve as a guinea pig for a one-time devaluation of the RMB. After all, how often in history do you see a large country like China running on three different official exchange rates?

Much thanks to Arthur Kroeber at GaveKal Dragonomics and Dan Rosen at Rhodium Group for inspiring this article through their Columbia SIPA course called "China's New Market Place". Also special thanks to Professor Michael Cheah at NYU and Michael Zhu at First Eagle Investment Management for their unstinting suggestions! Readers are encouraged to double-check data points before making investment decisions.

See also Market Update: Gee Thanks, Japan! And Zuckerberg Vs. Bezos (Video) on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}