Note: The following is an excerpt from this week’s Earnings Trends report. You can access the full report that contains detailed historical actual and estimates for the current and following periods, please click here>>>

Here are the key points:

- For 2022 Q2, total S&P 500 earnings are expected to increase +2.1% from the same period last year on +9.7% higher revenues and net margin compression of 95 basis points.

- Excluding the hefty contribution from the Energy sector, total Q2 earnings for the rest of the S&P 500 index are expected to be down -6.1% on +7.4% higher revenues.

- Q2 earnings are expected to be above the year-earlier period for 9 of the 16 Zacks sectors, with the strongest gains in Energy (up +212.1%), Transportation (+130.5%), Basic Materials (+16.7%), Construction (+19.8%), Autos (+20.8%), and Business Services (+8.0%) sectors.

Part of the uncertainty in the market at present is related to how earnings estimates should evolve in an aggressive Fed tightening cycle. The market has a sense of what should happen to earnings estimates, but it isn’t seeing much of that just yet.

The natural order of things is that rising interest rates take the edge off of aggregate demand, causing the economy to start cooling off. Businesses start experiencing this changed ground reality in their normal operations, which shows up in their quarterly numbers and management’s guidance.

We have started seeing some of that already. For example, recent quarterly results and guidance from the likes of Nike NKE, Bed Bath & Beyond BBBY, and Lennar LEN could be indicative of many more such reports, as the June-quarter reporting cycle really gets going. That said, not every early reporting company is missing estimates or guiding lower, as we saw in the results from Oracle ORCL, FedEx FDX and General Mills GIS.

It is reasonable to expect the Q2 earnings season to give analysts a clear directional thrust to adjust their estimates in-line with the economic moderation resulting from Fed tightening. But history tells us that analysts aren’t very good at identifying inflection points in the economy.

This suggests that we will likely need to wait some more, perhaps until the Q3 reporting cycle in October, to get clarity on the revisions question. That said, we have had some estimate cuts already, though they are nowhere near what would be consistent with a significant economic slowdown, not to mention a recession.

You can see in the chart below that the aggregate earnings total for this year has actually increased since the start of the year.

Image Source: Zacks Investment Research

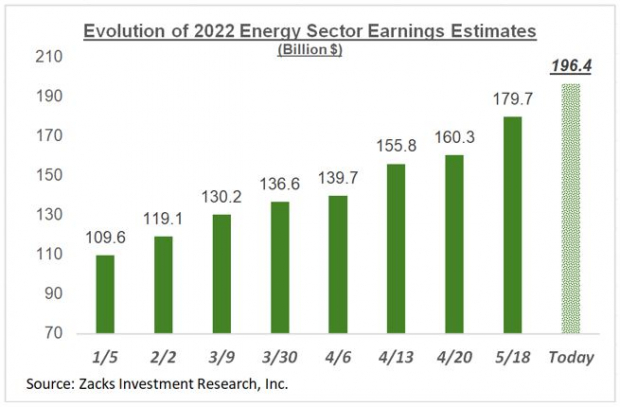

A very big part of the above positive revisions trend is thanks to the Energy sector, which you can see below.

Image Source: Zacks Investment Research

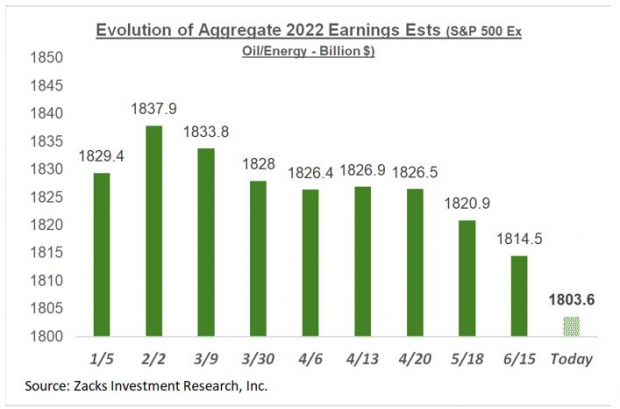

The chart below shows us the aggregate revisions trend for the S&P 500 index on an ex-Energy basis.

Image Source: Zacks Investment Research

As you can see above, aggregate S&P 500 earnings outside of the Energy sector have declined -1.4% since the start of the year, with double-digit percentage declines in the Consumer Discretionary (down -15.5%), Retail (-13.9%) and Aerospace (-12.8%) sectors.

Aggregate Energy sector earnings estimates for the year have increased by +79.2% since the start of the year. Other sectors enjoying significant positive revisions since the start of the year include Basic Materials, Autos, Consumer Staples and Construction.

A lot will be riding on how management teams share evolving business trends in their industries on the Q2 earnings calls. But given the lag with which tighter monetary policy seeps through to the broader economy, we may have to wait some more to get greater clarity.

The Overall Earnings Picture

Beyond Q2, the growth picture is expected to modestly improve, as you can see in the chart below that provides a big-picture view of earnings on a quarterly basis.

Image Source: Zacks Investment Research

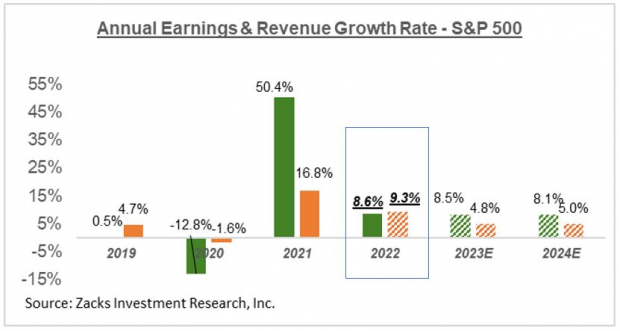

The chart below shows the overall earnings picture on an annual basis, with the growth momentum expected to continue.

Image Source: Zacks Investment Research

As strong as the full-year 2022 earnings growth picture is expected to be, it’s worth remembering that a big part of it is due to the unprecedented Energy sector momentum. Excluding the Energy sector, full-year 2022 earnings growth for the remainder of the index drops to only +2.8%.

There is a rising degree of uncertainty about the outlook, reflecting a lack of macroeconomic visibility in a backdrop of Fed monetary policy tightening. The evolving earnings revisions trend will reflect this macro backdrop.

Zacks' Top Picks to Cash in on Electric Vehicles

Big money has already been made in the Electric Vehicle (EV) industry. But, the EV revolution has not hit full throttle yet. There is a lot of money to be made as the next push for future technologies ramps up. Zacks’ Special Report reveals 5 picks investors

See 5 EV Stocks With Extreme Upside Potential >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

NIKE, Inc. (NKE): Free Stock Analysis Report

General Mills, Inc. (GIS): Free Stock Analysis Report

Oracle Corporation (ORCL): Free Stock Analysis Report

FedEx Corporation (FDX): Free Stock Analysis Report

Bed Bath & Beyond Inc. (BBBY): Free Stock Analysis Report

Lennar Corporation (LEN): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.