Key Points

U.S. adult smoking rates continue to reach all-time lows.

Altria has been able to offset declining volume with its pricing power.

Altria hasn't been making as fast a progress in its non-smoking segments as some investors would like.

- 10 stocks we like better than Altria Group ›

In sports, it's much easier to ignore off-court antics when they're from your star player. The same thought process is often applied to stocks, too. It's much easier to ignore a company's red flags if its stock is producing.

That's the position that Altria (NYSE: MO) has found itself in recent years, with its business and attractive dividend. According to the CDC, U.S. adult smoking rates have declined to an all-time low, at 9.1%. As the country's largest tobacco company, Altria has been directly affected by this. It's a shrinking market.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

But as one of the stock market's premier dividend stocks, is it worth ignoring the elephant in the room?

Image source: The Motley Fool.

A portfolio built for any type of consumer

Despite falling volume, Altria's one saving grace has been its pricing power. Cigarette smokers tend to like what they like and will spend whatever (within reason) it costs for their preferred product. In cases where rising prices push customers toward more discount brands, Altria's portfolio helps it retain some of those customers by having options.

A good example is the first quarter, where Altria's flagship Marlboro brand lost 1.4 percentage points in retail share, while its discount brand, Basic, gained 2.4 percentage points. Ideally, you'd want your customers in your premium segment because the margins are higher, but that's a much better alternative than losing them completely.

Marlboro will continue to be Altria's foundation and its biggest brand equity, but it's nice to know you have a portfolio that can cater to both premium and budget-conscious consumers.

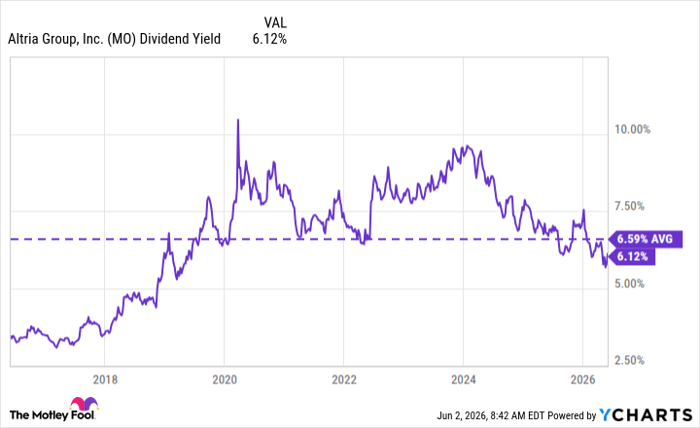

Just how attractive is Altria's dividend?

I consider Altria a premier dividend stock because of its consistently high yield and longevity. Its current dividend yield is 6.1%, slightly below its 6.6% average over the past decade. For comparison, the S&P 500's current yield is barely above 1% (as of June 1).

Altria is also a Dividend King (a company with at least 50 consecutive years of dividend increases), with a 56-year streak of increases (60 total in that time). The company knows its dividend is the selling point for investors, so it prioritizes keeping it healthy and growing. It's far from a growth stock, but its dividend and recent share buybacks are as shareholder-friendly as they come.

Financially, Altria doesn't seem to be in any major trouble sustaining its dividend for now. In Q1, its free cash flow was $2.23 billion, and it paid $1.8 billion in total dividends and $280 million in share buybacks. That 81% payout ratio (excluding buybacks) is still safe, but again, there's the elephant in the room.

MO Dividend Yield data by YCharts.

What smoke-free product is coming to save the day?

The story of Altria is a race against time. In other words, can it find a viable smoke-free alternative by the time the declining smoking rates become an irreversible issue? I don't think it will happen quickly, but I do think Altria's runway is a bit longer than some skeptics believe.

It's true that after Altria's failed $12.8 billion Juul experiment and Njoy fiasco, it doesn't necessarily deserve the benefit of the doubt. But there are a few positives to be optimistic about. Right now, Altria is banking on its On! nicotine pouches becoming a viable product. While they haven't been able to stand up against the popular Zyn nicotine pouches, they have been making progress nonetheless.

In Q1, the number of On! cans shipped increased 17.5% year over year to 46.2 million. They lost 0.8 percentage points in the oral tobacco market, but right now, footprint matters. They're now available in more than 100,000 stores in all 50 U.S. states. It's still an uphill battle for Altria in the segment, but the turnaround doesn't have to happen overnight. At its scale, there just needs to be progress.

With its attractive and reliable dividend, I think it's worth investors being patient until there's a clearer reason to ring the alarm and jump ship.

Should you buy stock in Altria Group right now?

Before you buy stock in Altria Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Altria Group wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $449,393!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,366,006!*

Now, it’s worth noting Stock Advisor’s total average return is 983% — a market-crushing outperformance compared to 212% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of June 4, 2026.

Stefon Walters has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.