Plug Power (NASDAQ: PLUG) is on a mission to deliver sustainable energy with its innovative fuel cells. The company looks to capitalize on the renewable energy market with its hydrogen technology. According to an estimate by Deloitte Consulting, the green hydrogen market could reach $1.4 trillion by 2050, giving Plug Power massive upside potential.

Even so, the company has faced significant hurdles in recent years. After reaching as high as $75 per share in 2021, the stock has come crashing down to Earth, plummeting 97%, and has failed to recover since then. Here's what you should consider if you are thinking of buying Plug Power (or if you already have).

Start Your Mornings Smarter! Wake up with Breakfast news in your inbox every market day. Sign Up For Free »

Reason to buy or hold Plug Power

Plug Power aims to position itself in the evolving renewable energy sector with its hydrogen fuel cells. As an alternative to conventional batteries, Plug Power provides clean and efficient energy with minimal carbon emissions.

The company develops products that use electrolysis to produce hydrogen from water, creating a green fuel source. Their advanced liquefaction and cryogenic systems facilitate the efficient storage and transportation of hydrogen gas, making the fuel accessible and practical for various applications.

One of its products is GenDrive, a hydrogen-powered fuel cell system engineered for material-handling vehicles, such as forklifts. And its GenSure system aims to provide a reliable backup and grid-support power solution, ensuring that crucial infrastructure remains operational during broader outages.

The company counts industry giants like Amazon and Walmart among its customers and investors, which could provide it with a steady revenue stream and longer-term growth opportunities. With support from major companies, Plug Power could be in position to benefit from the projected increase in hydrogen demand, which McKinsey estimates could rise by two to four times by 2050.

Image source: Getty Images.

The long-term growth opportunity makes Plug Power stock appealing, but its financial situation is something to keep an eye on.

Reason to sell Plug Power

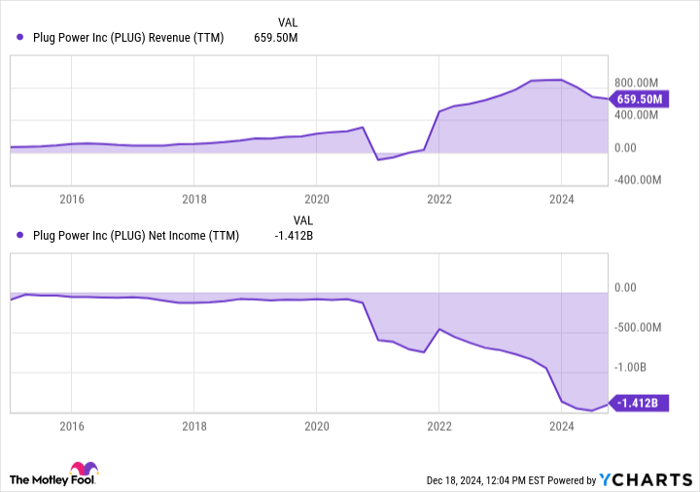

Plug Power has experienced solid top-line growth in recent years, with revenue increasing by 27% last year to $891 million. However, the current landscape paints a different picture. In the first three quarters of 2024, revenue plummeted to $437 million, reflecting a 35% decline compared to last year.

This downturn is mainly attributable to the company's struggles with hydrogen infrastructure sales. In the current year, it completed only 11 hydrogen site installations, a stark contrast to the 41 installations from the previous year. This reduction illustrates the slower-than-anticipated development of the hydrogen economy.

Moreover, Plug Power is grappling with rising losses. As of Sept. 30, the company reported an operating loss of $720 million, slightly worse than the $718 million loss from the prior year. Over the last 12 months, Plug Power's total losses are a staggering $1.4 billion.

PLUG revenue (TTM), data by YCharts; TTM = trailing 12 months.

In response to these challenges, the company has initiated cost-reduction strategies and hired Dean Fullerton as the new chief operating officer (COO). With his experience overseeing engineering services for Amazon across various regions, Fullerton is expected to enhance Plug Power's operational efficiencies and optimize its supply chain.

Management has adjusted its revenue projections for the coming year, estimating between $850 million and $950 million -- well below its previous estimates of $1.5 billion.

On a more promising note, the Department of Energy (DOE) awarded Plug Power a conditional loan of $1.66 billion in May to finance the construction of six clean hydrogen plants. These will produce hydrogen intended for use by clients within the material handling, transportation, and industrial sectors.

However, with the political dynamics shifting, particularly with the Trump Administration's impending inauguration in January, CEO Andy Marsh looks to secure this loan before the transition. Failure to do so could significantly hinder the company, which is already facing cash flow challenges.

Buy, hold, or sell Plug Power?

Plug Power's technology could help further develop the renewable energy industry. However, the company faces significant challenges due to declining revenue and disappointing forward-looking projections. Most recent projections from analysts show that it may not be profitable until 2028.

If you're intrigued by Plug Power's technology and prospects, it could be a stock to add to your watch list and track over time. I would like to see improved sales and more efficient operations that help bring down costs. However, given the uncertainties ahead and its lack of financial success, I'd say the stock is a sell right now.

Should you invest $1,000 in Plug Power right now?

Before you buy stock in Plug Power, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Plug Power wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $825,513!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of December 16, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool's board of directors. Courtney Carlsen has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon and Walmart. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.