It'a been a tough few months for shares of Pinterest (NYSE: PINS). The stock was crushed during the summer after the company warned of slower revenue growth when it reported its second-quarter results. Then, the stock took another hit following its third-quarter results as investors disliked the company's fourth-quarter guidance.

Let's examine Pinterest's most recent results and guidance to see if this is a golden opportunity to buy the stock on the dip.

Another disappointing forecast

Pinterest turned in another solid quarter of revenue growth, with its top line rising 18% to $898.4 million. However, it marked a continued deceleration of growth from 23% in Q1 and 21% in Q2. U.S. and Canada revenue grew 16% to $719 million, while European revenue climbed 20% to $137 million. Revenue from the rest of world (ROW) segment jumped 38% to $42 million.

Monthly active users (MAUs) grew by 11% to 537 million, led by a 16% jump in ROW users to 300 million. U.S. and Canada MAUs increased by 3% to 99 million, while European users rose by 8% to 139 million.

One of the most important metrics to look at for Pinterest is average revenue per user (ARPU), as closing the gap with competitors and better monetizing its users is the company's biggest opportunity moving forward.

Overall ARPU rose 5% to $1.70, although it tends to be best to look at trends on a regional level since ARPU levels vary greatly from region to region. In the U.S. and Canada, ARPU climbed 13% to $7.31, while European ARPU rose by 11% to $1. For the rest of the world, ARPU jumped 18% to $0.14.

Looking at profitability, Pinterest reported a 31% jump in adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) to $242 million. Adjusted earnings per share (EPS), meanwhile, soared 43% to $0.40.

Pinterest forecast Q4 revenue of between $1.125 billion and $1.145 billion, representing 15% to 17% growth year over year. This would be a continued deceleration in revenue growth. The company said it has been seeing weakness in the food and beverage vertical, which will persist into Q4. However, it is seeing strength in lower funnel revenue.

Is this a golden opportunity to buy the dip?

For the second straight quarter, Pinterest stock sank on guidance. While the food and beverage industry vertical is facing headwinds and spending a bit less on advertising, overall there are still a lot of good things happening at Pinterest.

Regional ARPU continues to grow solidly, and the company will expand its Amazon partnership into Canada and Mexico. Meanwhile, it continues to test and grow its partnership with Alphabet to help better monetize users from emerging markets. It's also turning to resellers to help in these markets.

Meanwhile, it just made its Performance+ automation platform (which helps improve ad campaign creation) generally available to advertisers at the start of October -- and will introduce Performance+ with ROAS (return on ad spending) in Q1. This should help be a driver in 2025.

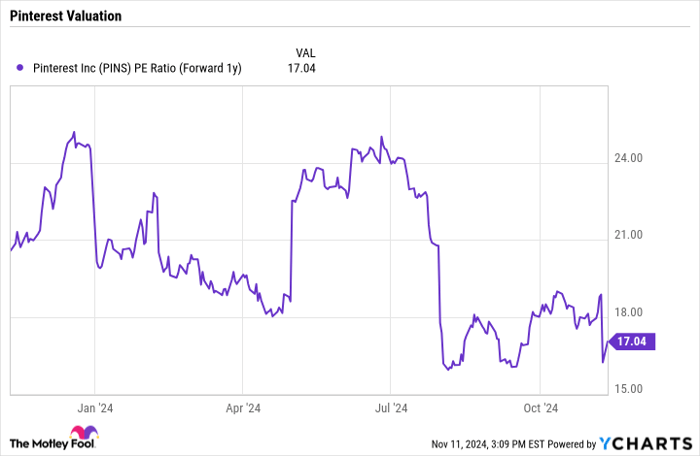

Trading at a forward price-to-earnings (P/E) ratio of about 17 based on 2025 analyst estimates, Pinterest stock looks attractive given the opportunities in front of it.

PINS PE Ratio (Forward 1y) data by YCharts

While investors were disappointed with Pinterest's decelerating growth, the stock is attractively valued based on its current growth. Meanwhile, it still has a lot of opportunities to continue to better monetize users both in the U.S and abroad. This, together with Performance+ could help reaccelerate revenue growth next year.

As such, I think the dip in stock price is a golden opportunity to buy this growth stock.

Should you invest $1,000 in Pinterest right now?

Before you buy stock in Pinterest, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Pinterest wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $896,358!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of November 11, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool's board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool's board of directors. Geoffrey Seiler has positions in Alphabet and Pinterest. The Motley Fool has positions in and recommends Alphabet, Amazon, and Pinterest. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.