Periodic Tables of Risk - Q2 2023

Published quarterly, the Periodic Tables of Risk highlight how different factors in the capital markets are affecting institutional investors’ portfolios. The percentages represent the trailing quarterly returns for these key factors.

Review the tables and accompanying commentary to understand what’s driving (or detracting) from returns for investors.

Asset Class Risk Factor Returns Q3 2020 to Q2 2023 (trailing 3 years)

Commentary

Data-Driven Insights for Asset Owners

The Source is a twice-monthly email newsletter that delivers insights on the topics that matter most to asset owners. Sign-up to stay in the know with the latest analysis, news, and views on the world of institutional investing from Nasdaq.

Learn More- 2023 has thus far been characterized by a return to "risk-on". The fears of stubbornly high inflation (and the need for high rates to combat it) seem to have abated, allowing the market to rally and bonds to recover some of their prior losses.

- The most consistent macro factor this year has been the equity market which has benefited from stabilizing inflation, a slowdown in interest rate increases, and the U.S. economy's ability to withstand everything without going into a recession.

- Two questions to consider over the coming quarter will be:

- 1) Will bonds regain their ability to act as a consistent portfolio hedge and diversifier now that markets are less driven by fears and expectations of rising rates?

- 2) If things continue to normalize, how will higher real yields on shorter duration and lower risk fixed income assets (such as 1-2 year Treasuries) affect the demand for riskier assets? What is the incentive to go further out on the risk curve when attractive real yields can be had virtually risk free and could we see the return of the carry trade where investors go long the bonds and currencies of higher yielding and lower inflation countries and short the bonds and currencies of lower yielding and high inflation countries?

Key

Market: MSCI All Country World Stock Index

Rates: 20+ Year Treasuries

Credit: US Corporate Credit Index

Commodities: GSCI Commodities Index

Dollar: US Dollar versus basket of foreign currencies

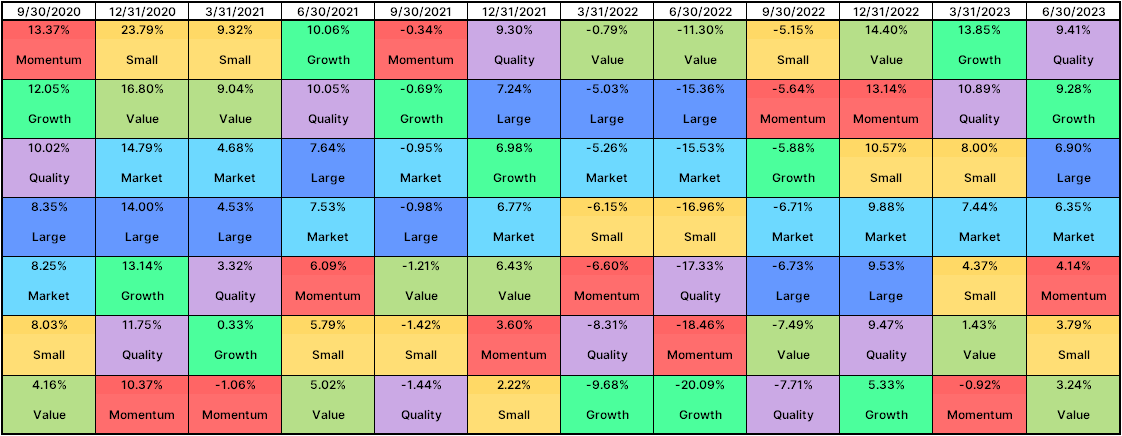

Equity Style Risk Factor Returns Q3 2020 to Q2 2023 (trailing 3 years)

Commentary

- Within equities, the hype around AI has caused a quick reversal of last year’s short-lived value rally (relative to growth stocks).

- Looking at the past 3 quarters, an interesting bifurcation has emerged where growth, quality, and large tend to move together while momentum, small, and value tend to do the same. This indicates (and we confirmed it by checking the stats) that quality is significantly positively correlated to growth and to a lesser extent larger firms.

- Meanwhile momentum is, at least for now, more correlated to value, smaller firms, and commodities (but subject to change as it turns over). The implication is that correlations across equity styles are constantly shifting, which causes the risk contributions of each equity style to a portfolio to change as well. When macro drivers change significantly, equity styles and factors that investors rely on for diversification may suddenly offer less (or more) of it than anticipated – thus, it is important that investors pay close attention to these shifts.

Key

Market: MSCI All Country World Stock Index

Quality: MSCI Quality Index

Momentum: MSCI ACWI Momentum Index

Growth: MSCI ACWI Growth Index

Value: MSCI ACWI Value Index

Large: MSCI ACWI Large Cap Index

Small: MSCI ACWI Small Cap Index

Do You Know What’s Driving Your Portfolio Risk?

Dive deeper in this new whitepaper to learn how risk factors affect multi-asset class portfolios for institutional investors.

Tony Yiu

Nasdaq

Tony Yiu is the Director of Quantitative Research & Development for Nasdaq Solovis and currently leads the Risk Analytics team.

Nasdaq for Asset Owners

Nasdaq

Delivering insights and intelligence for institutional investors

Read Nasdaq for Asset Owners 's Bio