Netflix (NASDAQ: NFLX) stock has been an incredible performer, up more than 1,100% over the past 10 years. The stock's momentum has continued this year, with its shares up more than 50%, boosted by its most recent quarterly results.

The company continues to be the big winner in the streaming space, and saw another nice jump in paid memberships in Q3. Meanwhile, it provided a solid outlook for next year.

Let's take a closer look at Netflix's Q3 results and determine whether it's too late to buy the stock or whether its momentum can continue.

Growing memberships

Netflix continues to show strong membership growth, with paid memberships rising 14.4% year over year to 282.72 million members. Memberships for the ad-supported plan continue to soar, rising 35% sequentially. This continues the streak of strong double-digit paid membership growth the company has seen over the past year.

| Metric | Q3 2023 | Q4 2023 | Q1 2024 | Q2 2024 | Q3 2024 |

|---|---|---|---|---|---|

| Membership growth | 10.8% | 12.8% | 16% | 16.5% | 14.4% |

| Paid members |

247.15 million |

260.28 million |

269.6 million |

277.65 million |

282.72 million |

Data source: Netflix earnings reports.

This membership growth helped lead to a 15% increase in revenue to $9.8 billion. That was above the $9.7 billion in revenue that the company had previously forecast.

U.S. and Canada revenue rose 16%, with a 10% increase in paid members and a 5% rise in average revenue per member (ARM). Asia led the way with a 19% jump in revenue, while European sales rose 16% and Latin American revenue was 9% higher.

Earnings per share (EPS) climbed 45% from $3.73 a year ago to $5.40. That was well ahead of the $5.10 Netflix had forecast three months earlier.

Ad-supported memberships made up approximately 50% of sign-ups where Netflix offers the service, showing the continued impact this tier is having on its business. The company said it is getting close to reaching enough subscribers in all its ad-supported countries to reach critical scale for advertisers, allowing the tier to continue growing and being better monetized. However, it said that the ad-based service is currently scaling faster than Netflix can monetize its growing ad inventory, which is a drag on its ARM.

Netflix has also recently increased prices in several regions. It said earlier in the month it raised prices in a few EMEA (Europe, Middle East, and Africa) countries and Japan, and it was set to increase prices in Spain and Italy right after the earnings report. Management also said Netflix had discontinued its basic plan in the U.S. and France this past quarter and it will do the same in Brazil in Q4. Analysts have been expecting Netflix to raise prices in the U.S., but the company did not clearly indicate when that might happen.

Looking ahead, Netflix forecast Q4 revenue to grow by nearly 14% year over year to $9.7 billion, with EPS of roughly $5.10. It offered up guidance for next year as well.

For 2025, Netflix projects that revenue will grow by 11% to 13%, reaching $43 billion to $44 billion. It expects operating margins to come in around 28%, up slightly from 27% in 2024.

Image source: Getty Images.

Is it too late to buy Netflix's stock?

Netflix was able to nicely grow its paid memberships this year despite the lingering effects the 2023 Hollywood strikes had on its content slate this year. That should normalize in 2025, and several new seasons of popular shows are lined up for next year, including Wednesday, Squid Games, and Stranger Things. Its strong content lineup should be a nice growth driver next year, and help propel it past its initial guidance.

In addition, the company continues to delve into more live events. In December, the service will have some NFL games, and it will also show the Mike Tyson-Jake Paul fight next month. Perhaps most importantly, though, 2025 will be the start of its deal to broadcast WWE's popular Monday Night Raw nearly every week of the year. These live events should help the company continue to gain scale for its advertising business. While its advertising will take some time to become a meaningful contributor to the overall revenue flow, it should be a large future growth driver.

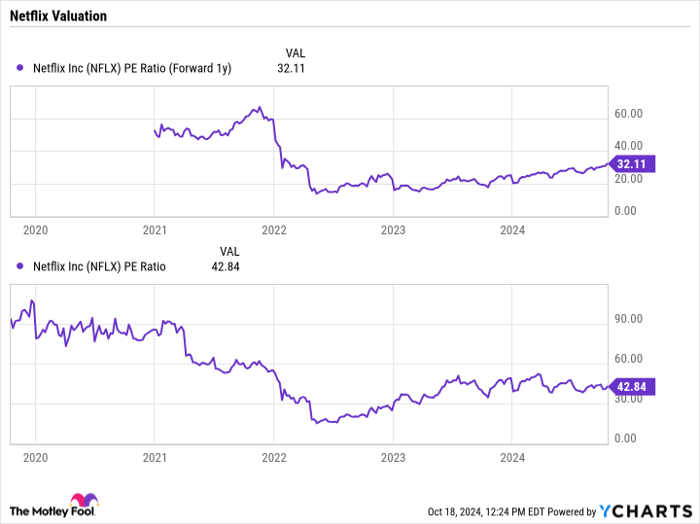

Netflix trades at a forward price-to-earnings (P/E) ratio of 32 times based on 2025 analyst estimates. The stock has often traded at a P/E ratio well above 40 times in the past, so while its valuation has risen, it is still well below where it traded several years ago.

NFLX PE Ratio (Forward 1y) data by YCharts

Overall, Netflix still has a lot of opportunities in front of it. Membership continues to increase. The introduction of more live events and a return to a normal content production slate only helps in this regard. Meanwhile, the company should have some pricing power, while advertising looks like it could be its next big future growth driver in a few years.

As such, I don't think it is too late to buy Netflix, as the stock's future continues to look bright.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,285!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $44,456!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $411,959!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 21, 2024

Geoffrey Seiler has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Netflix. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.