As Alibaba BABA approaches 2025, investors face a crucial decision point amid the company's aggressive AI investments and strategic pivots. While the stock has gained traction with a 14.3% year-to-date return, the critical question remains: should investors enter now or wait for a potentially better entry point in 2025? Recent developments in AI technology and cloud computing capabilities, coupled with China's anticipated monetary policy shift, present both opportunities and challenges for potential investors.

Current Performance and Strategic Direction

Alibaba's second-quarter fiscal 2025 results paint a picture of a company in transition, with revenues reaching $33.7 billion alongside a 5% year-over-year growth. While maintaining a robust $50.2 billion net cash position, the company's substantial investments in AI infrastructure have led to a 70% decrease in free cash flow. This decline reflects Alibaba's strategic prioritization of long-term value creation through technological advancement, particularly in AI and cloud computing, though it may pressure near-term profitability.

AI Innovation and Cloud Leadership

The company's technological advancement is particularly evident in its recent AI initiatives. The launch of Wanx 2.1, achieving an 84.7% score on the VBench leaderboard, demonstrates Alibaba's growing capabilities in visual AI and content generation. The Cloud Intelligence Group continues to show strong momentum, with AI-related products maintaining triple-digit growth for five consecutive quarters. The recognition as an Emerging Leader across all four quadrants in Gartner's Innovation Guide further validates its technological leadership.

Strategic Investments and Market Expansion

International commerce through AIDC shows robust growth at 29%, while the implementation of new monetization strategies, including a 0.6% software service fee and increased adoption of the Quanzhantui marketing tool, signals improving revenue potential. The Qwen model series has garnered significant traction with more than 40 million downloads and spawned 78,000 derivative models, indicating strong ecosystem adoption. Meanwhile, Model Studio's reach to more than 300,000 customers underscores growing market penetration in the enterprise AI space.

Investment Considerations

Several factors warrant careful consideration before making an investment decision. The company's investments in advanced AI models like QVQ for visual reasoning and autonomous delivery vehicles through Cainiao's GT Pro demonstrate a clear commitment to future growth. However, these investments, while promising, may continue to pressure margins in the near term. The anticipated shift in China's monetary policy to "appropriately loose" in 2025 could provide macroeconomic tailwinds, but geopolitical tensions and domestic competition remain key risk factors.

Price Performance & Valuation

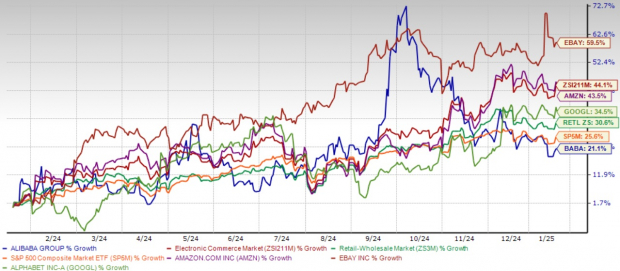

The stock has gained 21.1% in the past year compared with the Zacks Internet-Commerce industry, the Zacks Retail-Wholesale sector and the S&P 500’s return of 44.1%, 30.6% and 25.6%, respectively.

Alibaba’s dominant e-commerce position in China remains threatened by global bigwigs like Amazon AMZN and eBay EBAY. Also, BABA's growth in the global cloud market has been significantly hindered due to rising competition from the leading cloud players, namely Amazon, Microsoft and Alphabet’s GOOGL Google.

1-Year Performance

Image Source: Zacks Investment Research

Alibaba is currently trading at a discount with a forward 12-month Price/Earnings of 8.11X compared with the industry’s 25.48X and lower than the median of 15.04X. This valuation metric indicates that BABA's stock is significantly undervalued compared to its industry peers, trading at less than half the industry average P/E ratio. The lower-than-median forward P/E suggests an attractive entry point for investors, as the stock appears to be trading below its fair market value despite strong fundamentals. It also has a Value Score of A, which is hard to ignore.

BABA’s P/E F12M Ratio Depicts Discounted Valuation

Image Source: Zacks Investment Research

Investment Strategy Recommendation

Given the current landscape, investors might benefit from a measured approach. While Alibaba's technological advances and market position are impressive, several factors suggest better entry points may emerge in 2025. The company's aggressive investment phase in AI infrastructure and international expansion, though strategically sound, may continue to impact near-term financial metrics.

The ongoing share buyback program, with $22 billion in authorization remaining, provides some downside protection and demonstrates management's confidence in the company's long-term value proposition. However, investors should closely monitor key metrics, such as cloud revenue growth, AI adoption rates and the success of international market expansion before making substantial commitments.

A gradual position-building strategy through 2025 might offer the most prudent approach to participating in Alibaba's long-term growth potential while managing near-term volatility risks. This strategy allows investors to benefit from potential improvements in operating leverage as AI investments mature and monetization strategies take hold while maintaining flexibility to adjust positions based on execution success and market conditions.

The Zacks Consensus Estimate for fiscal 2025 revenues is pegged at $137.85 billion, indicating 5.63% year-over-year growth. With the Zacks Consensus Estimate for fiscal 2025 earnings indicating a downward revision of 5.6% over the past 30 days to $8.78 per share, the market appears uncertain regarding Alibaba's growth trajectory.

Image Source: Zacks Investment Research

Find the latest earnings estimates and surprises on Zacks Earnings Calendar.

Conclusion

While Alibaba's long-term prospects appear promising, particularly in AI and cloud computing, the current transitional phase suggests patience may be rewarded. Investors should consider waiting for clearer signs of return on AI investments and the impact of China's monetary policy changes before making significant commitments. Monitoring the company's execution in cloud computing, AI monetization and international market penetration will be crucial for identifying more favorable risk-reward entry points in 2025. BABA stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Just Released: Zacks Top 10 Stocks for 2025

Hurry – you can still get in early on our 10 top tickers for 2025. Handpicked by Zacks Director of Research Sheraz Mian, this portfolio has been stunningly and consistently successful. From inception in 2012 through November, 2024, the Zacks Top 10 Stocks gained +2,112.6%, more than QUADRUPLING the S&P 500’s +475.6%. Sheraz has combed through 4,400 companies covered by the Zacks Rank and handpicked the best 10 to buy and hold in 2025. You can still be among the first to see these just-released stocks with enormous potential.

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

eBay Inc. (EBAY) : Free Stock Analysis Report

Alphabet Inc. (GOOGL) : Free Stock Analysis Report

Alibaba Group Holding Limited (BABA) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.