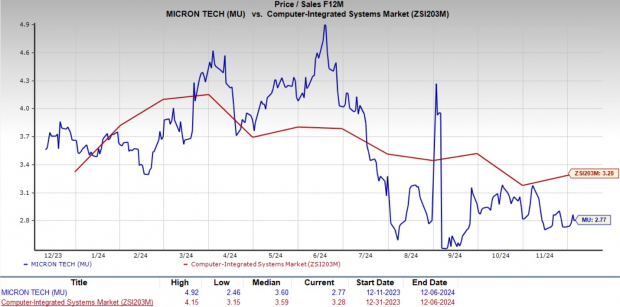

Micron Technology, Inc.’s MU current valuation suggests that the stock is available at a discounted price compared with the industry average. MU stock trades at a forward 12-month price-to-earnings (P/E) ratio of 10.41, significantly lower than the Zacks Computer – Integrated Systems industry average of 20.21. Similarly, the forward 12-month price-to-sales (P/S) ratio of 2.77 is substantially lower than the industry average of 3.28.

Image Source: Zacks Investment Research

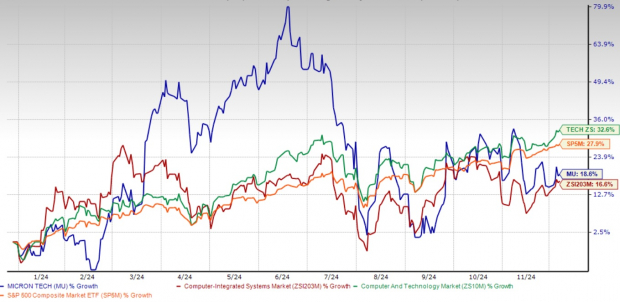

Shares of Micron have been highly volatile in 2024, with the stock soaring 18.6% year-to-date. While this performance has outpaced the industry, it has lagged behind the Zacks Computer and Technology sector and the S&P 500 index, raising questions about its current valuation and prospects. Despite trading at a low valuation multiple compared to the industry, Micron's near-term challenges suggest that holding the stock is the best action for now.

YTD Price Return Performance

Image Source: Zacks Investment Research

Industry Trends Favor Micron's Long-Term Growth

Micron’s position in high-demand segments such as artificial intelligence (AI), automotive and industrial IoT places it at the forefront of the semiconductor industry's evolution. The explosion of AI applications has significantly increased demand for advanced memory solutions, such as DRAM and NAND. Micron’s investments in cutting-edge DRAM and 3D NAND technologies ensure it remains competitive and poised to capitalize on these trends.

Micron’s diversification strategy is noteworthy. By reducing reliance on consumer electronics, which are more susceptible to demand swings, and focusing on stable sectors like automotive and data centers, Micron mitigates revenue volatility. This balance reinforces its resilience in an industry often impacted by cyclical trends.

Micron’s Product Innovation and Partnerships Drive Demand

Micron’s innovative product lineup strengthens its market position. Its high-performance GDDR7 graphics memory is already being tested by key players like Advanced Micro Devices AMD and Cadence Design Systems CDNS, highlighting its relevance in gaming and advanced computational applications.

Moreover, Micron’s HBM3E chips are set to power NVIDIA’s NVDA next-generation AI chip, the H200. This collaboration underscores Micron’s critical role in the AI ecosystem. Micron has already sold out its HBM supply for 2024, with robust orders secured for 2025, ensuring strong revenue visibility in the coming years.

Micron’s Financial Recovery and Positive Outlook

Micron has staged an impressive recovery from the downturn it faced in late 2022 and early 2023. It has consistently surpassed earnings expectations in the past four quarters, averaging a surprise of 72.7%. This performance highlights its ability to navigate market challenges effectively.

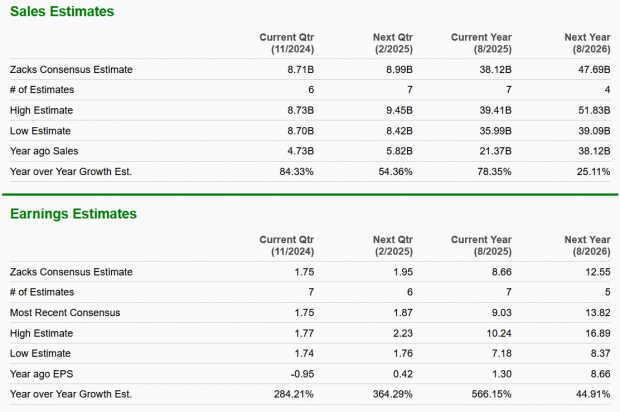

Micron’s fiscal 2025 and 2026 growth prospects remain positive, supported by its significant investments in memory technologies and partnerships with major tech players. The Zacks Consensus Estimate reflects continued optimism for Micron’s earnings trajectory, driven by strong demand in AI, data centers and other high-growth markets.

Image Source: Zacks Investment Research

Micron: Risks to Watch

Despite its strengths, Micron faces near-term challenges that could pressure its growth. A primary concern is the risk of oversupply in the high-bandwidth memory (HBM) market. As HBM chips become increasingly critical to Micron’s revenues, any imbalance between supply and demand could lead to declining average selling prices (ASPs). Such a scenario would directly impact profit margins, particularly as competition intensifies.

Micron’s dependence on AI-driven demand also presents a potential vulnerability. While the AI revolution is fueling unprecedented growth, any slowdown in adoption or shifts in technological trends could impact demand for its memory solutions.

Conclusion: Hold Micron Stock for Now

Micron is well-positioned to thrive in the evolving semiconductor landscape, thanks to its leadership in advanced memory technologies and strategic partnerships. Its financial recovery and commitment to innovation bolster its long-term growth potential. However, near-term uncertainties, including the risk of HBM oversupply and market volatility, warrant a cautious approach.

For now, holding Micron stock appears to be the best strategy. As the memory market stabilizes, Micron’s value proposition may become even more compelling, making it a stock worth monitoring closely. Currently, MU carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Free Today: Profiting from The Future’s Brightest Energy Source

The demand for electricity is growing exponentially. At the same time, we’re working to reduce our dependence on fossil fuels like oil and natural gas. Nuclear energy is an ideal replacement.

Leaders from the US and 21 other countries recently committed to TRIPLING the world’s nuclear energy capacities. This aggressive transition could mean tremendous profits for nuclear-related stocks – and investors who get in on the action early enough.

Our urgent report, Atomic Opportunity: Nuclear Energy's Comeback, explores the key players and technologies driving this opportunity, including 3 standout stocks poised to benefit the most.

Download Atomic Opportunity: Nuclear Energy's Comeback free today.Advanced Micro Devices, Inc. (AMD) : Free Stock Analysis Report

Micron Technology, Inc. (MU) : Free Stock Analysis Report

NVIDIA Corporation (NVDA) : Free Stock Analysis Report

Cadence Design Systems, Inc. (CDNS) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.