Mastercard (NYSE: MA) is one of the largest payment processors in the world, sharing an effective duopoly with Visa (NYSE: V). Mastercard has rewarded investors with huge growth over time, and the stock has advanced a massive 500% over the past decade alone. But is this the best payment processor to buy right now? It might pay to do a bit of comparison shopping before you buy.

What does Mastercard do?

Although consumers often consider the credit cards they have in their wallets Mastercards or Visas, the truth is that the cards are issued by other companies. The logos really just signify that Visa and Mastercard handle the back-end work of approving and tracking the use of those cards. Don't underestimate what this means -- the technology and global network that Mastercard (and Visa) have created is impressive. And, perhaps even more important, the systems are highly secure.

Image source: Getty Images.

The way Mastercard makes money is by charging a tiny fee for every transaction that moves through its processing network. A few cents here and a few dollars there doesn't sound like much, but when you process $2.5 trillion dollars worth of transactions in a single quarter, the numbers start to add up. Revenues and earnings have been on a fairly steady upward climb for decades, showing the strength of Mastercard's underlying business.

Basically, Mastercard (and Visa) have been at the forefront of a shift from cash to card/digital payments. That shift is likely to keep going, particularly as online shopping expands its reach. And since ensuring the safety of transactions is just as important as simply facilitating those transactions, it seems likely that the two largest payment processors have a protected industry position given their ability to spend on continually upgrading their processes and systems. There are very good reasons to believe that buying Mastercard will work out well over the long term, if you own it long enough.

Is Mastercard the best choice today?

The problem here is that just about everything positive about Mastercard's business can be said about Visa's business, too. In fact, the two have vary similar growth rates over the long term (though Mastercard's near-term performance has been stronger). However, there's a subtle difference between the two stocks today and that shows up in their valuation.

For example, Mastercard's price-to-sales (P/S) ratio is roughly equal to its five-year average. But Visa's P/S ratio is slightly below its longer-term term average. The same story is true of the price-to-earnings (P/E) ratios for these two companies. Using traditional valuation metrics won't lead you to believe that Mastercard is overpriced per se, but if you compare the company to its main competitor you will come away thinking that Visa is more attractively priced.

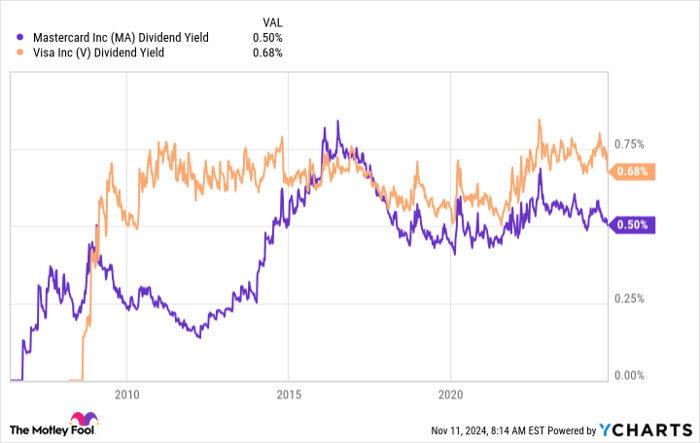

MA Dividend Yield data by YCharts

That flows through to the dividend yield as well, a less traditional valuation tool. Mastercard's yield is roughly 0.5% while Visa's yield is 0.75%. Neither of those are large, but Visa's yield is 50% larger. And, more to the point, Visa's dividend yield is toward the high end of its historical yield range while Mastercard's yield is more middle of the road.

All in, Visa looks more attractively priced even though it shares many of the same business attributes that back the long-term investment appeal of Mastercard. Although you could argue that this difference reflects stronger near-term growth from Mastercard, the similarity between the two businesses suggests that the valuation difference may be placing too large a discount on the long-term potential Visa offers. Indeed, if Mastercard could help you achieve millionaire status, it seems likely that cheaper Visa could do the same, and with a more attractive dividend along the way.

Mastercard is fine, Visa just looks better today

There's nothing wrong with Mastercard, and most long-term growth investors would probably be fine buying it. But if you care about valuation, similarly positioned Visa looks like it would be a better choice right now for those looking to build a seven-figure nest egg with long-term investing.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $22,819!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $42,611!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $444,355!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of November 11, 2024

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Mastercard and Visa. The Motley Fool recommends the following options: long January 2025 $370 calls on Mastercard and short January 2025 $380 calls on Mastercard. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

%20Historical%20Data%20%7C%20Nasdaq&_biz_n=32&rnd=738186&cdn_o=a&_biz_z=1743398662793)

%20After-Hours%20Quotes%20%7C%20Nasdaq&_biz_n=33&rnd=447362&cdn_o=a&_biz_z=1743398663002)

%20Earnings%20Report%20Date%20%7C%20Nasdaq&_biz_n=34&rnd=448513&cdn_o=a&_biz_z=1743398663003)