News & Insights

By Phil Mackintosh, Senior Vice President, Chief Economist at Nasdaq and Michael Normyle, Senior Director, Economic Research at Nasdaq

Economy at a glance

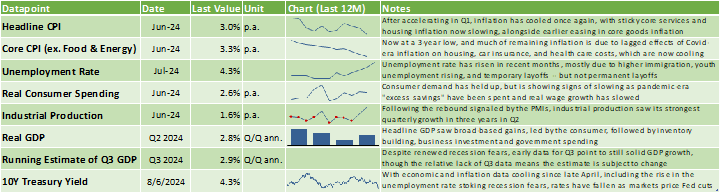

Figure 1: Key Indicators and Trends

After unexpected strength in Q1, economy started slowing since Q2

As we entered 2024, economists were expecting the US economy to slow with markets pricing as many as seven rate cuts. Then, data in Q1 showed the US economy and inflation remained unexpectedly strong. That pushed interest rates up (and rate cuts out), but the news was also good for company earnings (so equity prices rose).

How quickly things changed in Q2. In late April, data started coming in noticeably softer, with:

- Cooling inflation: Consumer price index (CPI) and personal consumption expenditures (PCE) inflation finally started to slow again, and producer prices slowed too.

- Softening labor data: Monthly job gains slowed, and unemployment rose. Labor seemed to sense the softening as “quiet quitting” was replaced by a quits rate back to pre-Covid levels.

- Consumer spending slowing: Lower-income households seemed to have exhausted pre-Covid savings and even real wage growth seemed to be offset by higher prices for essentials.

- Small businesses facing margin pressure: Increased borrowing costs and higher wages continued to crimp margins for smaller firms.

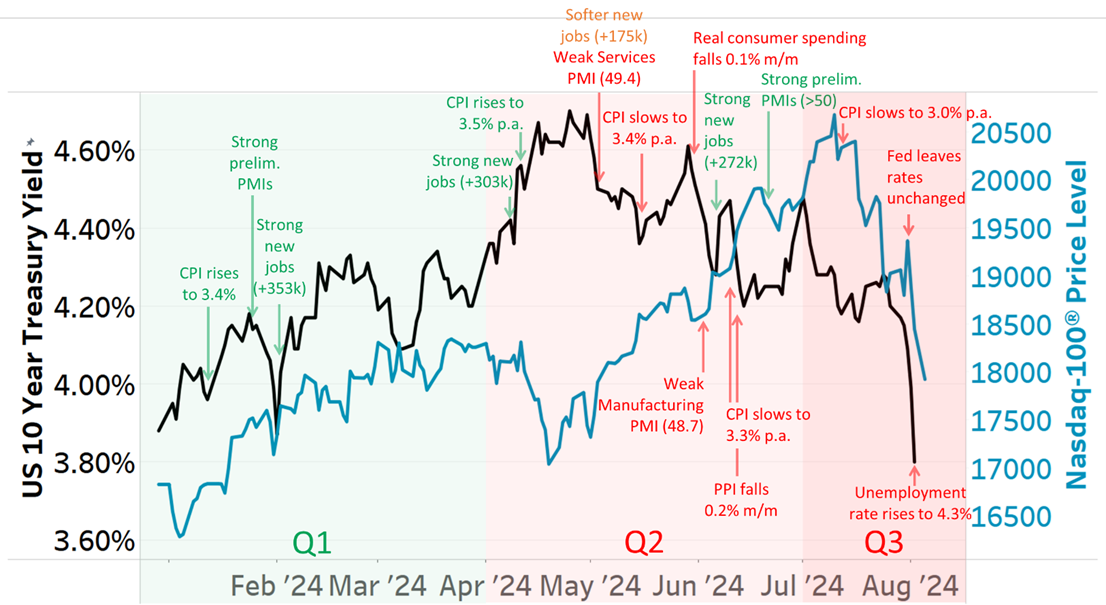

As Figure 2 shows, with more normal growth in the economy, rates started to matter to stocks again (with lower rates being better and vice versa). That was until recession fears reemerged with the latest jobs report coming in weaker than expected, sending stocks and rates lower.

Figure 2: Market-Moving Events in 2024

Sources: FactSet, Nasdaq Economic Research

In this economic outlook, we focus on three tracks:

- How the economy is slowing

- How company profits are driving stock returns

- How the rates outlook has improved (rates have fallen) but the US Federal Reserve (the Fed) risks again being “late”

1. Economy is slowing in places, returning closer to “normal” levels

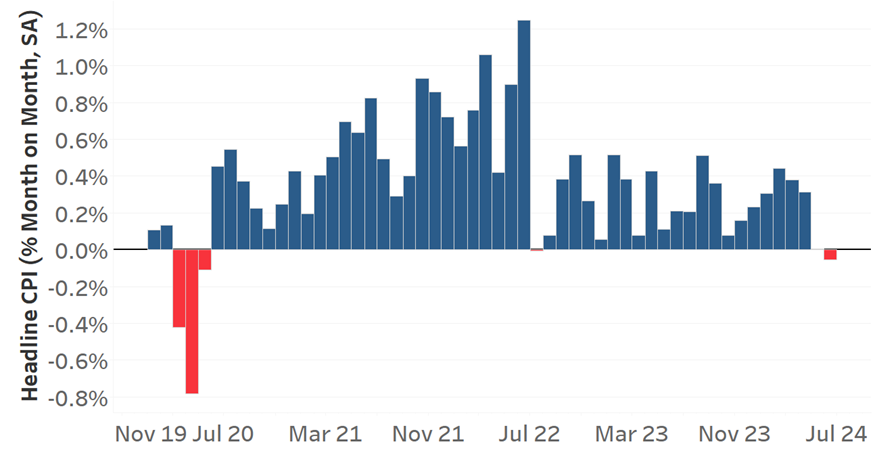

Sticky inflation is now falling too

After months of “sticky” inflation, data in Q2 was more helpful to set the Fed up to start cutting rates. From January to April, headline CPI inflation increased 0.35% per month on average (an annualized rate of 4.4%). From May to June, monthly inflation averaged 0.0%. In fact, in June, prices fell for the first time in two years (see Figure 3). That pushed headline inflation down to 3.0% p.a., while the Fed’s preferred PCE inflation is now running at 2.5% p.a., which tied for its lowest reading in over three years.

Figure 3: Monthly Headline CPI Inflation

Sources: FactSet, Nasdaq Economic Research

And many of the inflation components have been flat to down for a while. Food, goods, and energy inflation are all very low. But in Q2 we started to see housing slow too, with the smallest monthly increase in over three years in June. One measure of market rate rents fell -1.1% p.a. in Q2.

Don’t panic about the unemployment rate… yet

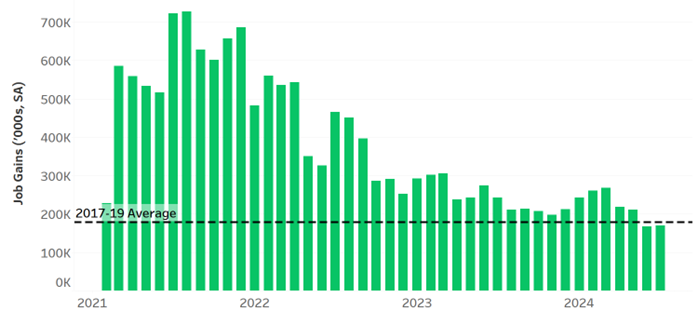

Supply and demand imbalances in the labor market caused by Covid seem to finally be back to normal.

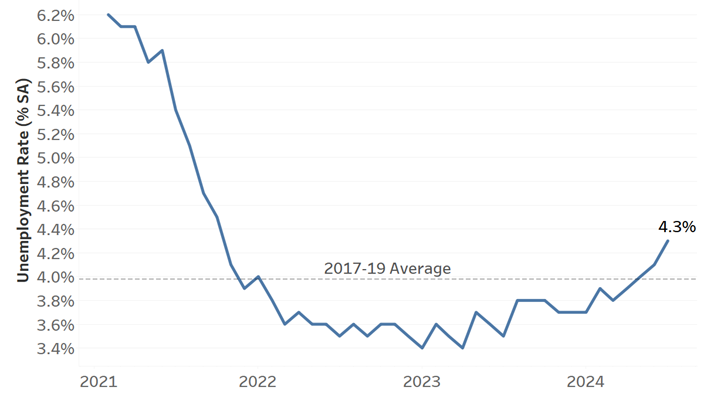

Over the last couple years, job gains have slowed and are now back to pre-Covid levels (Figure 4). But, with people joining the labor force faster than companies are hiring, the unemployment rate has pushed up to 4.3% (Figure 5). This caused some concern since it triggered a popular recession indicator – the “Sahm Rule,” which looks at the increase in the jobless rate from its low over the past year. Since the increase in the unemployment rate has mostly been driven by labor force growth and not job losses, its increase is not as bad as it seems. But, if the labor market continues cooling, a recession becomes increasingly likely.

For now, workers are no longer eager to quit, therefore the pressure on wages continues to slow – which should be good news for companies. It’s also good news for inflation that remains wage-driven, pointing to even lower inflation in the future.

Figure 4: Monthly Job Gains (3-Month Average)

Sources: FactSet, Nasdaq Economic Research

Figure 5: Unemployment Rate

Sources: FactSet, Nasdaq Economic Research

Small businesses are unable to raise prices and pull back on hiring

Overall, job losses remain low, helping maintain consumer confidence and spending – an important driver of the US economy’s strength.

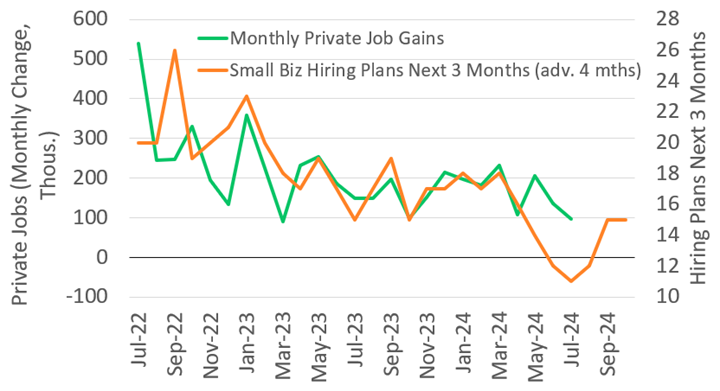

However, data suggests that small businesses, which employ nearly half of all workers, still face margin pressure. Over the last two and a half years, the share of small businesses able to raise prices has more than halved, while short-term borrowing costs have more than doubled to 9.5%. So, margins are getting squeezed from both sides.

To protect their bottom line, small businesses have reduced their hiring plans to a pace that’s consistent with fewer than 100,000 private sector job gains per month over the next few months (see Figure 6). That’s down from an average monthly gain of 200,000 jobs last year.

Figure 6: Private Job Gains and Small Business Hiring Plans

Sources: FactSet, NFIB, BLS, Nasdaq Economic Research

2. Stock prices driven by earnings differences

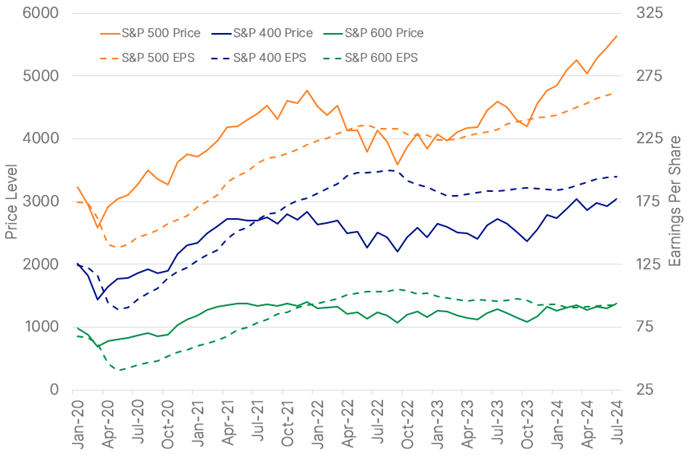

Although headline indexes recently hit all-time highs, small cap indexes have been struggling. In fact, the 1H24 return of the S&P 600 small cap index is just negative 2%, compared to the large cap index which gained 14% through June 2024.

However, stock returns reflect relative forward earnings growth (see Figure 7). Mega cap companies have grown earnings and maintained strong margins, supporting their recent highs. Higher earnings have helped push the S&P 500 up about 50% throughout the past couple of years, setting 38 new record highs this year alone (see Figure 7).

Meanwhile, data suggests the smaller companies are more affected by higher interest rates and wages. Earnings for the S&P 600 companies are still falling, while the large cap earnings recession recovery happened months ago. That could also be one reason some even smaller companies are still a little hesitant to IPO.

Importantly, moving forward, heading toward 2025 analysts project positive earnings growth for large, then mid, and finally small cap stocks. Combined with falling rates – that should be a tailwind for stocks.

Figure 7: Prices and Forward Earnings per Share (EPS)

Sources: FactSet, Nasdaq Economic Research; Note: July value is July 16, 2024

3. Rates are falling again and three rate cuts are possible in 2024

With inflation and employment both cooling, it seems to be time for the Fed to start cutting rates, especially knowing monetary policy operates with “long and variable lags.”

With inflation now 3% and falling and the Fed rates still at 5.5%, the US has the most positive real interest rates since before the credit crisis. Many economists argue a more “neutral” rate of interest would be around 3%.

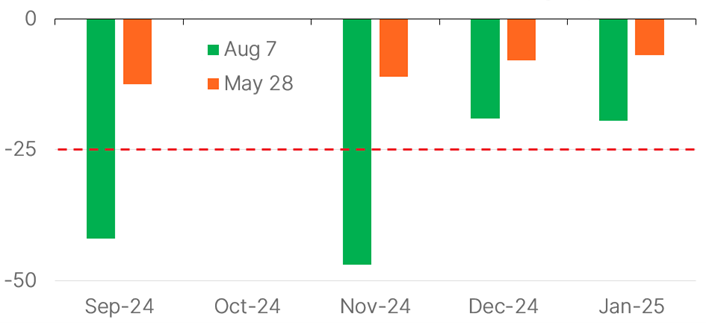

While the Fed used its July meeting to set the table for a possible cut in September, markets are pricing more than four cuts before 2025 – up from three prior to the increase in the unemployment rate to 4.3% (see Figure 8). However, that only gets rates down to 4.5%, so rates should keep falling in 2025 too.

Figure 8: Market-Implied Fed Rate Cuts by Meeting (bps)

Sources: FactSet, Nasdaq Economic Research

Lower rates will reduce interest expenses, which overwhelmingly benefits smaller companies with variable rate debt or bonds with imminent refinancing. However, with the economy clearly slowing, the question is whether the Fed might have waited too long to act. Will low unemployment still keep consumers spending, or will the economy slow before rate cuts start to help?

The market is still pricing in a soft landing as the base case – and for now, that still looks likely. But the risks of a hard landing are starting to increase. The Q3 data will be interesting to see.

5 Questions Board Members Should Ask Now

- How have we prepared for a recession?

- What is our debt refinancing schedule?

- Have our sales held up as the economy has normalized?

- Have we seen falling employee turnover as quits have slowed across the broader economy?

- Have we been able to raise prices to keep up with inflation?

To receive an exclusive video with further insights from Nasdaq’s Chief Economist and Senior Director of Economic Research, join the Nasdaq Center for Board Excellence. For the latest market insights, explore the Nasdaq Center for Board Excellence Resource Library and subscribe to Market Makers.

Latest articles

This data feed is not available at this time.

Data is currently not available