News & Insights

By Phil Mackintosh, Senior Vice President, Chief Economist at Nasdaq and Michael Normyle, Senior Director, Economic Research at Nasdaq

Economy at a Glance: Key Indicators and Trends

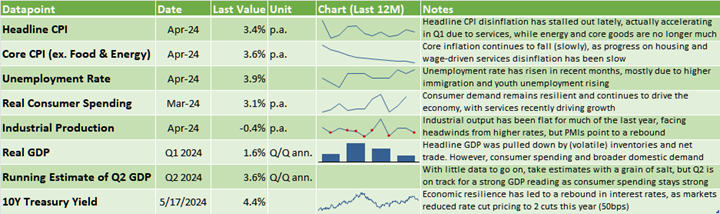

2024 has started stronger than expected

As we headed into December of 2023, inflation was quickly slowing down, and the job market seemed to have returned to normal. With interest rates well above the level of inflation, the market expected to see the Federal Reserve cut rates by at least 1.7% during 2024.

But a consistent feature of the first quarter of 2024 in the United States was much stronger economic data than expected. For example, we have seen strong:

- Jobs: One million jobs added in just four months.

- Spending: Real consumer spending grew 2.5% annualized in Q1.

- Wages: The Fed’s preferred Employment Cost Index rose 1.2% in Q1 – the fastest in one and a half years.

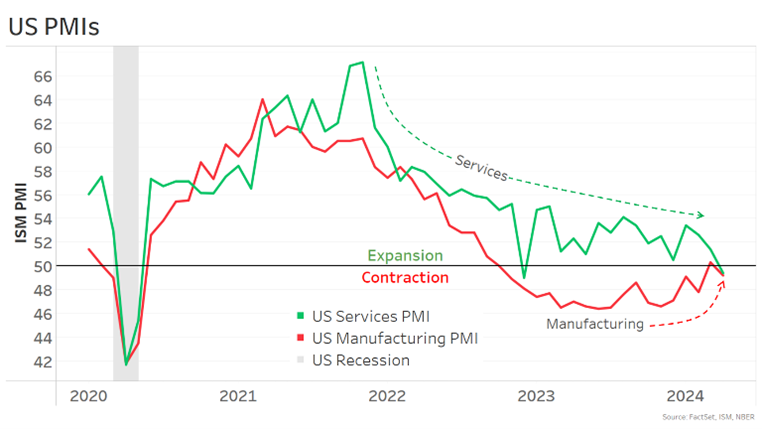

- Manufacturing: The Purchasing Managers’ Index (PMI) returned to expansion for first time since late 2022.

- Inflation: The Consumer Price Index (CPI) inflation rose to 3.4% per annum from 3.1% in January 2024.

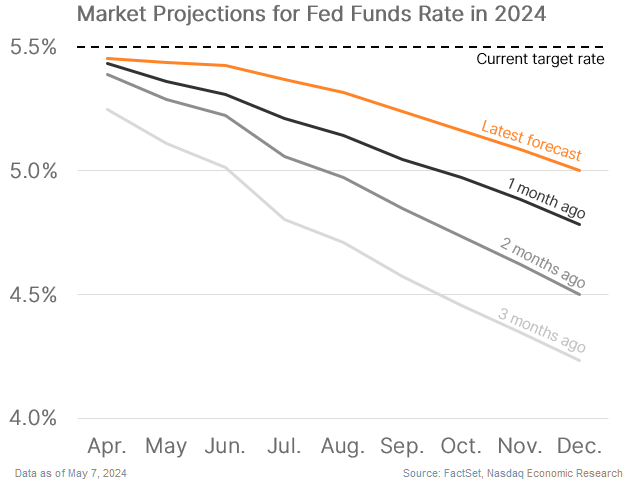

Rate cuts deferred, borrowing costs higher

The rate cut expectations for bond markets have been drastically reduced this year, with the market pricing just 50 basis points (bps) in cuts now.

Interest rates are expected to be “higher for longer,” again, with 10-year U.S. Treasury rates back up to around 4.45%.

That is potentially bad for companies paying variable interest. Data suggests many companies had already been refinancing maturing debt to shorter terms, hoping to finance at lower rates in the next year or so.

Economic strength good for stocks

The strong economy has also been helping stock prices. Strong consumer spending has helped grow earnings, with Q1 S&P 500 earnings on pace to rise 5.6% p.a. – the fastest pace since Q2 of 2022.

There are some consistent differences at the sector level, with Health Care, Energy, and Materials remaining in earnings recessions, while the consumer- and AI-driven sectors (Information Technology, Communication Services, Consumer Discretionary and Utilities) are on track for over 20% p.a. earnings growth.

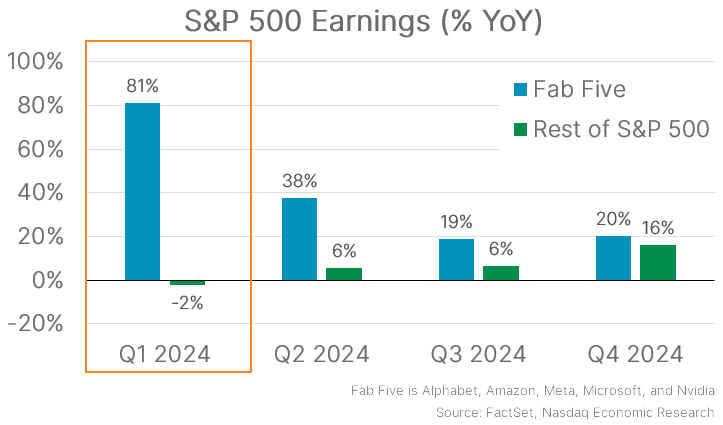

Mega-cap driving earnings (for now)

A more telling earnings divide exists between mega-caps and everyone else. The equity market leaders du jour are the “Fab Five:” Amazon, Google, Meta, Microsoft and Nvidia. Those five companies account for all the Q1 earnings of the S&P 500 and then some. They are on pace for 81% p.a. earnings growth, while the rest of the S&P 500 see negative 2% p.a. growth (chart below).

However, as the year goes on, analysts expect earnings growth to broaden. The rest of the S&P 500 is expected to see positive earnings growth in Q2 and come into line with the Fab Five’s earnings growth by Q4 2024.

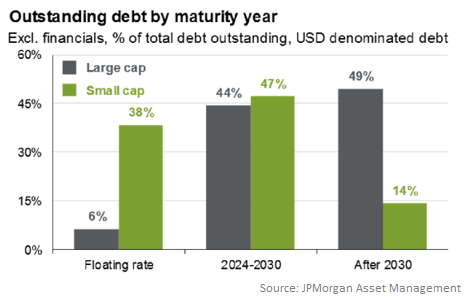

Smaller companies are still reporting earnings declines, with S&P 600 stocks on pace for earnings to fall 20% YoY in Q1. Smaller companies have been more impacted by higher interest rates, as they a have 6x larger share of debt that is floating rate compared to large caps. The data also shows small cap companies have very little fixed debt to refinance after 2030, leaving them more exposed to “higher for longer” rates.

Importantly though, consensus forecasts show earnings of small and mid-cap companies recovering, with profit growth expected by the end of the year.

PMIs indicate more normal 2024

Despite the strong real data, company activity surveys indicate activity in Manufacturing and Services is returning to more normal rates of growth.

That is good news for Manufacturing, which has been in contraction for well over a year. That only partly offsets the stall in services growth given services makes up around 80% of the economy.

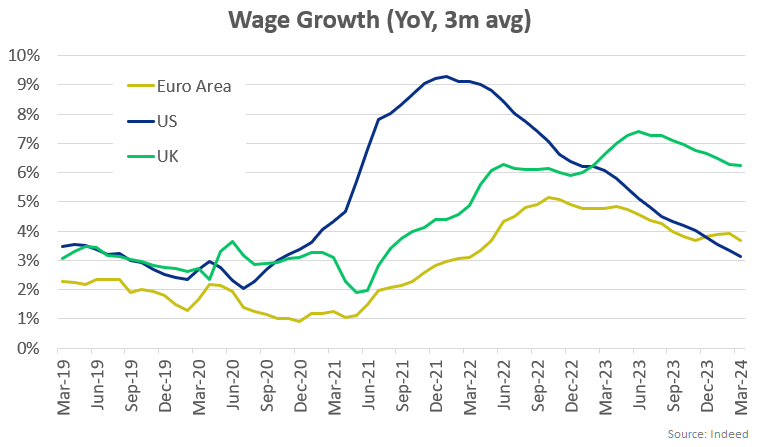

Jobs market much closer to normal

This slowdown in activity is consistent with other signs that the jobs market is closer to the old normal.

Job openings continue to fall, and workers are now less likely to quit jobs than before Covid, a sign that jobs are harder to find. Along with that, wage increases have also slowed back to pre-Covid levels.

Lower Inflation is still critical to reduce rates

Despite moderation in the jobs market, layoffs and unemployment are still near multi-decade lows. So, it seems smaller companies will only get relief on interest costs and refinancing if inflation falls, enabling the Fed to cut rates.

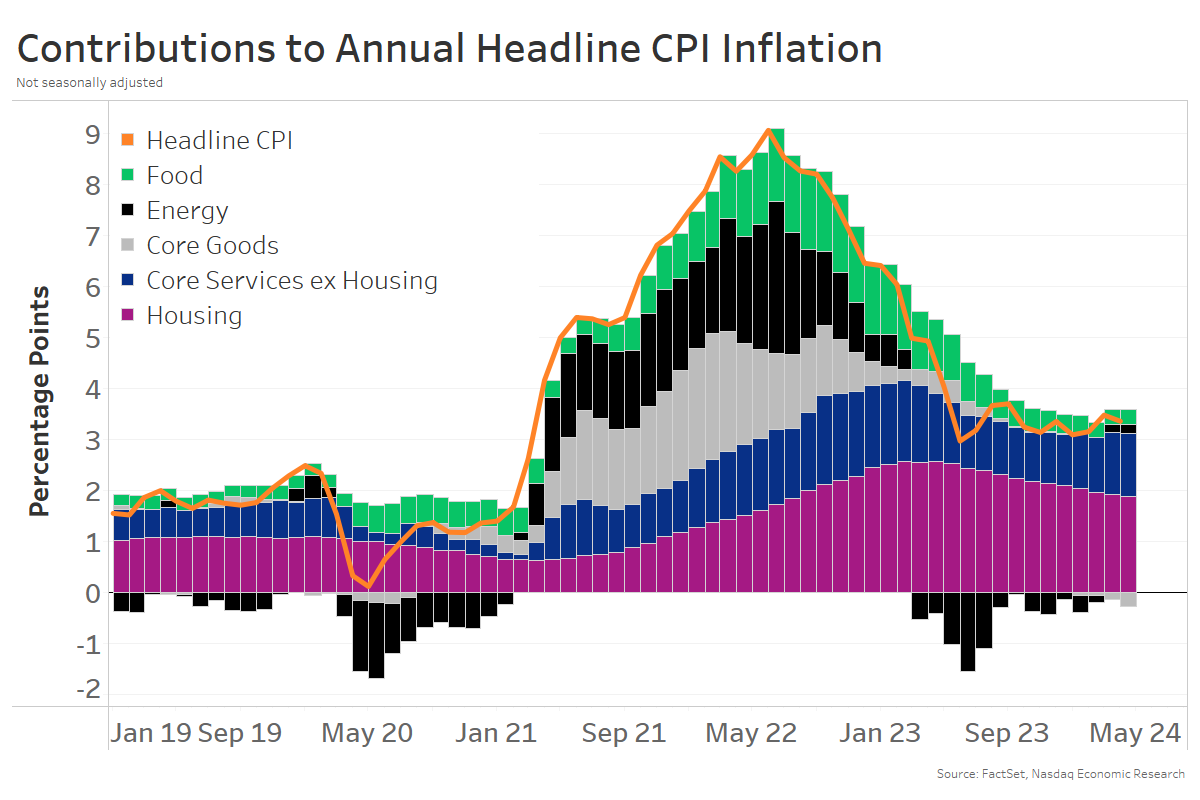

Many factors that pushed inflation up the last few years (energy, food and goods prices) are now seeing their inflation fall close to zero.

What has made overall inflation stickier (orange line) is Housing (purple bars) and Core Services (blue bars).

Importantly, Core Services inflation includes car insurance – which is still rising in response to increased vehicles costs from earlier chip and parts shortages leading to higher costs of new cars and repairs. However, vehicle costs have stabilized, pointing to normalization in the future.

The bulk of residual inflation is coming from rent. There too, leading indicators show new rent growth close to zero but the 12-month CPI data includes many one-year leases, some of which are still rising to catch-up to 2023’s price gains.

We still expect rates to fall, just more slowly

In short, inflation and a strong economy has added to expectations that higher interest rates will persist for longer than many probably hoped.

But normalization of wages and goods supply chains had added net disinflationary pressures.

That should allow the Fed to start cutting rates this year. Which, in turn, will help smaller companies manage new refinancing at higher rates while avoiding a recession.

Join the Nasdaq Center for Board Excellence to receive an exclusive video with further insights from Nasdaq’s Phil Mackintosh and Michael Normyle. For previous reports, we invite you to explore the Center’s Resource Library and subscribe to Market Makers.

Latest articles

This data feed is not available at this time.

Data is currently not available