News & Insights

The United States Securities and Exchange Commission (SEC) recently proposed banning volume discounts for agency orders on U.S. exchanges.

Apart from the fact that setting prices seems anti-competitive and eliminating economies of scale is bad economics (especially in stock markets), there are a number of other things this proposal ignores.

Leveling a fraction of the playing field?

The main justification for this proposal seems to be to level the playing field for brokers. It aims to do this by forcing all agency orders to pay and receive the same rates to trade on a single exchange – with the expected result that broker routing conflicts of interest will be solved.

However, there are a number of reasons why this won’t work.

First is the fact that fees will still be different across exchanges, meaning brokers may still be incented to route to the “cheapest exchange” regardless of the opportunity costs for the underlying investor.

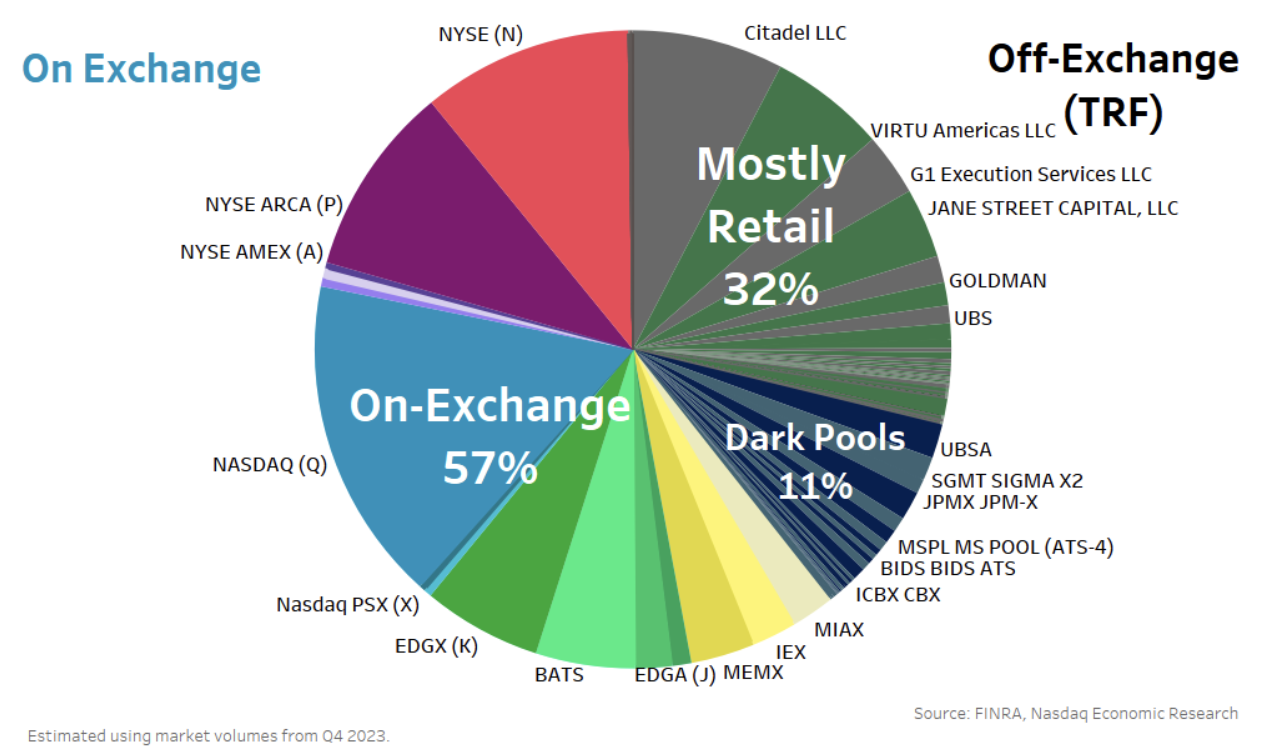

More importantly, this won’t actually level the playing field at all – for a very simple reason – a lot of trading happens off-exchange! The latest data shows that around 40% of trading in the U.S. happens away from exchanges.

On top of that, the SEC’s rule proposal only affects “agency” trades, and it estimates that only around 55% of all trading is agency. That means only 33% (55% agency x 60% on exchange) will be covered by this rule. Said another way, 67% of trading will be exempt from this rule, including a lot of agency executions that happen on non-exchange venues.

Chart 1: Trading in the U.S. market happens in a number of different — and different types — of venues

But in reality, the expected impact might be even worse than that.

In our own prior studies, we’ve estimated that the buy-side is potentially less than 10% of lit trading. And the SEC itself suggested the majority of retail trading already occurs off-exchange.

If that’s true, it’s likely that a lot of the other “agency” flow on the market is hedge funds. However, if hedge funds use “cost plus” trading strategies, research shows they have no conflict of interest from different exchange fees.

In short, rather than leveling a whole playing field, this might just form a pothole in one part of the field.

A lot of venues treat different customers differently

Any starting point for leveling the playing field needs to incorporate what the playing field is.

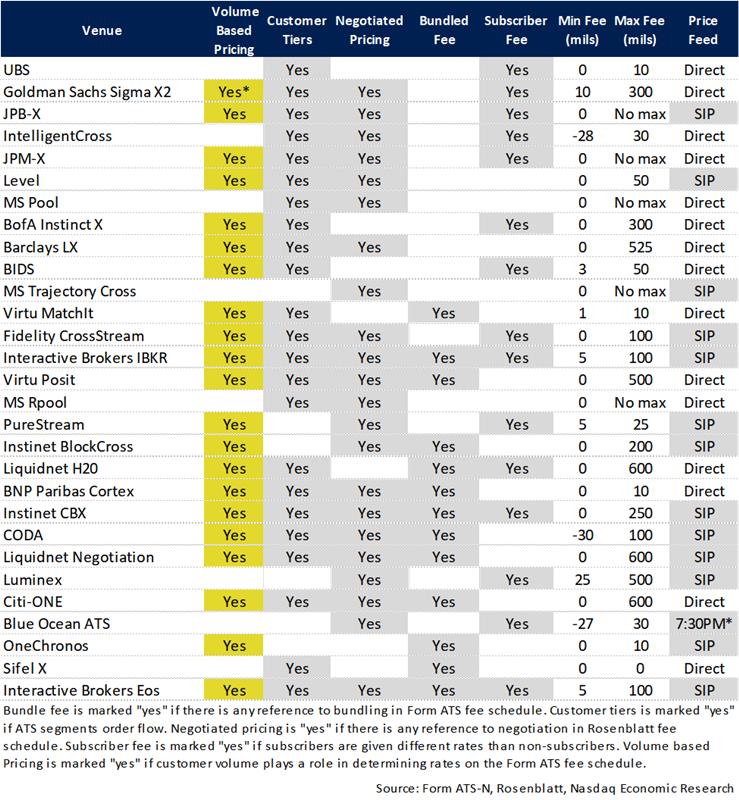

In reality, we know that exchanges are just one of the types of venues that investors can trade on. There are also ATSs (dark pools) and brokers internalizing trades. The data in Table 1 also shows that competitors to exchange trading also operate under quite different rules and trading practices.

Data also seems to show that all offer different pricing to their best customers – and many offer discounts to high-volume customers, or “volume-based tiers.”

Table 1: Different venues in the U.S. market operate in very different ways

However, there are many dimensions in addition to trading fees that each venue uses to compete with exchanges and each other.

Fair access and the value of an NBBO

Exchanges are generally required to provide “fair access,” where all participants can interact with all orders. Most exchanges offer quotes without a speed bump, meaning (in theory) that all their liquidity providers’ quotes are available to all investors on a market sweep. That tends to result in more adverse selection and less spread capture on exchange fills.

Exchanges are also the only venues providing public prices to the market that other venues use to determine their own execution prices. And although dark pools need to trade on the same ticks as exchanges, that’s not true for the whole market.

That makes things like rebates (and speed bumps) important to compete with the spread capture enabled by market segmentation. And that’s important for a high-quality NBBO, which creates economic benefits for the whole market, including benefiting issuers.

Customer Tiers

Dark pools and brokers are also able to use customer tiers to decide who they do (and don’t) want to trade with. That increases the profitability of spread capture (with or without rebates) on those venues. In fact, research shows that for retail trades, each broker gets a statistically different execution for the same retail order (see Chart 2 here).

Bundling and subscription models

Data also suggests that off-exchange venues sometimes bundle transaction pricing with other services or offer subscriber pricing models (with lower trade prices after a fixed cost payment).

These are rational economic solutions to the high-fixed-cost platforms market participants operate. However, their existence is also something exchanges need to be able to compete against.

Transparent and “equitable” transaction pricing

Although exchanges do offer tiers, those tiers are transparent (as they are filed with the SEC) and available to all (so any broker knows the trade-off between total costs and average costs as the trade).

Importantly, volume tiers specifically reduce the marginal costs of trading to those who trade the most (and usually add the most to market quality and breadth – a positive externality).

In contrast, the pricing models of other venues are less transparent – undoubtedly not “equal” – and likely less “equitable” than how exchange volume tiers work.

How dark pools price trades available via Form ATS-N

Apart from execution quality from 605 and routing in 606 reports, little is known about how pricing to different customers really works for non-ATS-TRF trades (the “mostly retail” in Chart 1).

However, thanks to Form ATS-N, which dark pools need to file, there is some transparency into how dark pools work.

Table 2: Form ATS-N disclosures for different pricing and cost decisions

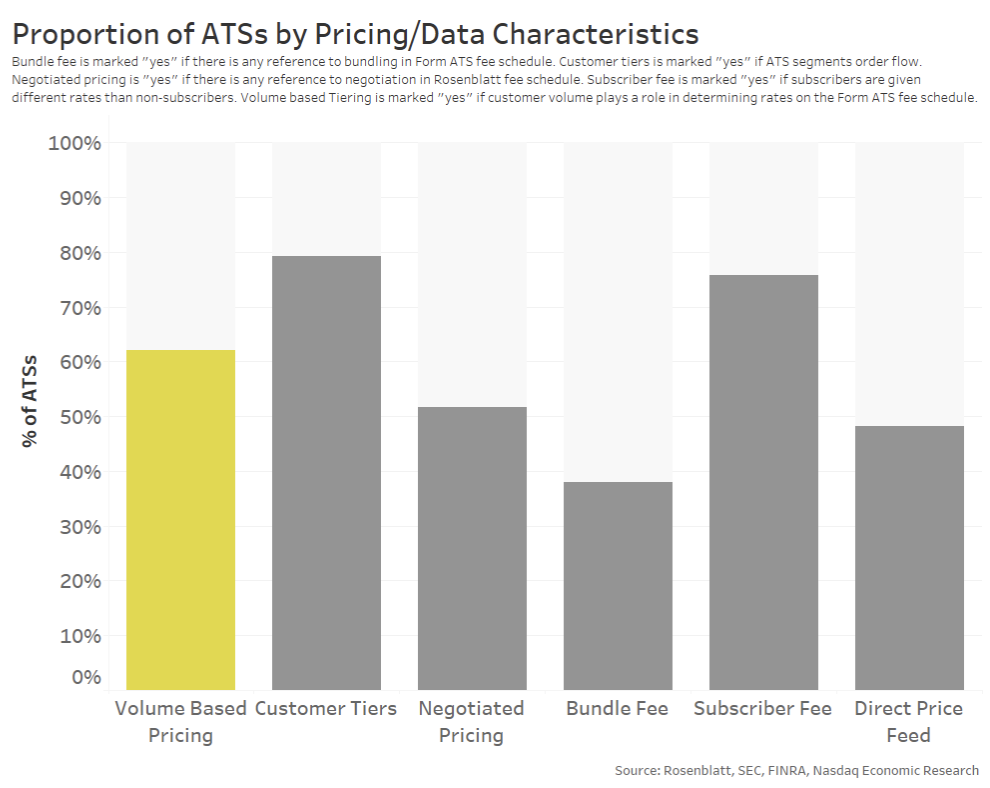

As we show in Table 2, ATSs compete across a number of pricing and cost dimensions – and many offer volume-based pricing.

The data also shows that most ATSs offer some form of customer segmentation categories, allowing for spread capture to be increased, removing the need to pay rebates to offset adverse selection.

Many ATSs also offer subscriber pricing, which allows for lower per-trade fees after a fixed fee or even bundled pricing.

Chart 2: ATS volume by pricing/data characteristics

Trading rates vary on ATSs

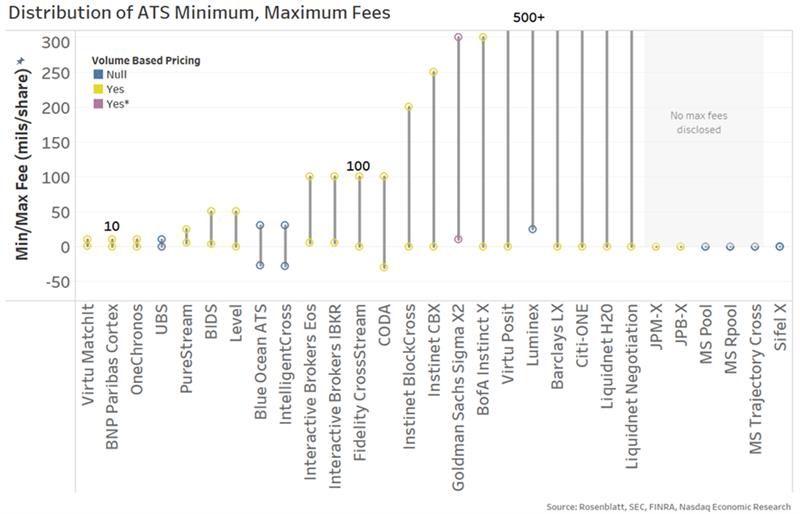

The data also suggests ATS fees are unlikely to be equal to all agency customers (like this proposal requires of exchanges). In fact, the majority of venues seem to offer volume-based discounts, with many having totally negotiable prices.

In addition, the data shows fees can range from rebates to as much as 600mils (or 6 cents) per trade – much more than the current cap on exchanges. Details in the filings often suggest that “affiliates” trade free. Affiliates represent the broker that owns the dark pool, which helps them achieve economies of scale that help cover the fixed costs of running an ATS as part of their platform.

Interestingly, though, given the Volume Tier pricing ban is meant to address broker routing conflicts, research shows that preferencing your own dark pool also creates a conflict of interest. This could be even larger than the conflict created by differences in exchange fees.

Chart 3: ATS fee schedules have a lot of variation- often tied to volume

Per-trade fees aren’t the whole picture

Also important to this debate is that per-trade fees are just a piece of the puzzle.

It’s true that exchanges charge fixed costs for hardware – things like connections, colocation, and data. It’s also true that brokers choose a range of different fixed-cost setups depending on their needs and specific cost-benefit decisions. By definition, those fixed-cost decisions are excluded from the volume tier rule; however, they are linked to the rationale of offering high-volume clients lower ongoing trading costs.

The ATS-N data shows that dark pools also make different fixed costs decisions in order to compete. For example, some buy proprietary data while others use SIP, which allows them to save over $1 million in fixed costs each year.

Fixing one fee for a sliver of the market won’t level the playing field

As we’ve discussed before, the market for trading is competitive, and that competition forms across the whole platform that exchanges and their customers operate.

What seems clear, now we’ve dug a little deeper into the data, is that fixing a single fee won’t level the playing field. It’s more likely to create distortions and inefficiencies. Given that this topic is tied to a competitive NBBO and tight spreads, it could harm investors and U.S. capital markets.

Latest articles

This data feed is not available at this time.

Data is currently not available