News & Insights

LBMA Precious Metals market volumes, October 2024, and their significance

Rhona O’Connell, StoneX Financial Ltd; 13 November 2024

Any views expressed here are of the writer and do not reflect a house view from NASDAQ.

Daily October average compared with daily average for January-September 2024

Source: LBMA

Source: LBMA

Welcome to our monthly round-up of the LBMA OTC trading volumes in gold, silver, platinum and palladium, as recorded on a daily basis by the Association. These are split into spot, swap/forward, options and LoanLeaseDeposit (LLD) and give a flavour of the markets’ activity and how they were influenced by external forces and news items.

All references to COMEX or NYMEX positioning refer to Managed Money, not commercial positions.

General introduction: -

All four metals posted gains during October, although platinum only just ended in the plus column while palladium took the spotlight with a spectacular run of almost 21% to its peak before reversing to post a net monthly gain of 11% (although this was then lost in early November). Silver also posted a reasonably aggressive bull run in the first half before closing 4% ahead, while gold posted new highs but in a narrow range, ending the month up 3%. Platinum gained just 1%, after trading broadly in line with gold.

Year-to-date, the changes were as follows:-

Silver 31%

Gold 27%

Platinum minus 4%

Palladium minus 12%

Influences on the gold price became increasingly closely focused on the imminent US Presidential election, with the race appearing to be tightening and therefore stoking the fires of uncertainty and taking gold to a fresh record in nominal terms. Mid-month’s heightened tension in the Middle East was also supportive. Silver shook off much of its fundamental concerns over the state of the Chinese and European economies, preferring to dance to gold’s tune. Platinum fundamentals remained broadly underpinned but uninspiring, while palladium had a spiralling run on the back of fanciful suggestions over possibly sanctioning Russian PGM exports.

Economic and Political Background

The United States

The NonFarm Payroll numbers were the centre of attention in early October and came in much stronger than expected, at +254k after a consensus expectation of +145. It is worth keeping in mind that NonFarm can (not unlike JOLTS, the Job Openings survey) be volatile, especially with revisions – most of which have been downward over the past few months. As October wore on the Presidential race looked to be tightening and the markets were increasingly pricing in a contested victory and / or a divided Congress. In the end of course the Presidential outcome was clear although as we write there is still a slim possibility that the House might be Democrat-controlled, so some uncertainty persists. Despite commentators arguing that the position was tight, and most of the polls falling well within the degrees of tolerance, the financial markets were ramping up the Trump-trade as October wore on, with bond yields rising and the dollar moving higher, although the equity markets were more cautious.

Meanwhile banking stresses have not gone away; the Swiss regulator Finma is now warning UBS to boost its emergency measures due to the risks involved after it was required to acquire Credit Suisse last year (the integration process is scheduled to last three years and is therefore half-way finished), while US banks are reported to be thinking of reducing interest payments on corporate deposits in an effort to bolster balance sheets. And an area that captures this writer’s concern is the fact that some stressed liabilities are being handed off from commercial banks into the Shadow banking Sector.

The European Central Bank cut its key rate by 25 points again and although at least one member of the Governing Council is reluctant to continue with back-to-back cuts the European economy – especially Germany, the EU powerhouse - remains very much in the doldrums. Since the start of 2021 Germany’s month-on-month Industrial production changes have been negative 56% of the time and although there are signs of improvement it is still oscillating on either side of zero and there is some degree of pressure for the ECB to cut rates again, and soon.

On the other side of the world, the Chinese Government has been addressing the comparative weakness in the economy and persistent concerns over the property market in particular and has implemented a series of stimulus measures, a programme that has continued into November. Thus far the markets have been disappointed and remain unconvinced that the 5% growth target can be achieved this year.

So that more or less sets the scene for the development in the metals markets in October; geopolitical uncertainty (some of which has now dissipated, of course), a bullish undertone for the dollar (now much more marked) and weakness in the other two regional blocs.

GOLD –over-extended by month-end, needing to correct (and it did!)

Overall volumes and spot price, September

Source: LBMA

- By comparison with the daily average for the preceding 12 months, gold posted healthy gains in all sectors apart from LLD, in which there was a negligible contraction.

- The largest gain was in options, although this is possibly misleading since the boost came from just four days of very heavy volume, in each case well exceeding the (average+one standard deviation) measure for an outlier. The first two of these days were the 9th and 10th, when gold was trading flat, just above $2,600, suggesting call activity .

- Heavy forward volumes on these two days also suggest some forward buying given the sentiment then prevailing in the market.

- The other heavy options days were the 16th and 18th as gold approached, then cleared, $2,700.

- The early part of the month was quiet in all the other sectors. After the early action in the forwards, spot took over the heavy lifting for much of the rest of the month, especially in the middle, then forwards joined in again.

- Spot was busiest in the third week, with a $100 run from $2,660-$2,760, triggered in part by the killing of Hamas leader Yahya Sinwar (plus a supportive moving average crossover) although the move lost momentum as it appeared that this action was not going to trigger over-aggressive responses. The heaviest volume came as the rally started going into reverse, as is so often the case as some positions are closed and opposite positions are opened.

- There was one final push to the highs in the final week, to an intraday record of $2,790; this drew out some hedging activity as well as heavier forward trading. The market was overbought and the appearance of hedging activity was no surprise, and also contributed to the correction that had already started before the results of the Presidential election.

- The Diwali Festival was at end-October and ran into November, and a good monsoon plus pent-up demand meant that offtake was healthy (monsoon is significant as the Indian farming community is a key buyer of gold and of course the quality of the crop dates available expenditure).

- Meanwhile the latest figures from the World Gold Council show that the Chinese have been the largest buyers of gold ETFs in the year to end-October (and beyond) with a 87% or 51t gain, to 105t.

Gold technical pattern; year to date

Source: Bloomberg, StoneX

ETFs: mixed ; 15 days of net creation from a total of 23 trading days; net gain of 24t for a year-to-date loss of seven tonnes.

CFTC: fresh longs and fresh shorts. Longs dropped at the start of the month with prices easing, then reinstated and eased latterly, more or less in parallel with price action. Shorts rose steadily through the month, but not by much. End-month; longs at 771t and shorts at 104t

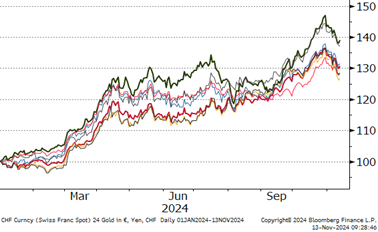

Gold in local currencies, year-to-date

Source: Bloomberg, StoneX

SILVER over-heated and riding for an early October fall

- Silver largely had the same profile as gold during October (often the case when gold is showing a clear trend0 although as gold retreated early in the month, silver continued higher for a few days before meeting resistance at $33, and corrected to the month’s low of $30.1, before rallying to $34.9 on the 22nd and 23rd. A mixed week followed and the month closed at $32.7.

- By comparison with the previous twelve months, spot volumes were up 10%, forwards were virtually unchanged, options were strongly ahead (+35%) and LLD was down, although broadly level with September volumes.

- Spot was quiet in the first half of October as prices more or less consolidated in a range oscillating around the $31 level, but burst into life on the 18th-20th as prices added 10% in three days. Siler is notorious for this kind of move (and downwards can be even more vicious); this one was prompted by gold’s response to the problems in the Middle East (see above) and was almost certainly extended by some gold:silver ratio trading.

- The LLD number s suggest that hedging was active in the prior period, when silver was between $30 and $31 and may well have contributed to the inability to clear to the upside. Activity then faded into the ensuing rally.

- Options were busiest in the second half, probably targeting $34 and $35 on the way up.

- Forwards were generally quiet apart from a lively day right at the start of October, and here, too, this action may have accounted for the narrow range in the day in question, leading to resistance at $23.

Total silver volumes, September, M ounces

Source: LBMA

ETFs; the buyers had the upper hand; 13 days of net creation for a gain of 716t; year-to-date gain of 1,368t. Global annual mine production is ~26,000t.t.

CFTC: longs traced a similar path to gold – and to the silver price, for a small net gain overall, while shorts contracted over the first half but then expanded again especially towards month-end as prices challenged $35.

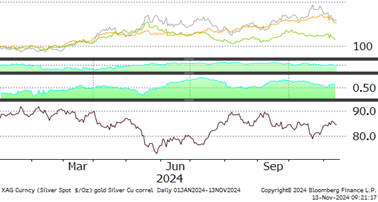

Silver, gold and copper; the correlations and the gold:silver ratio, year-to-date

Source: Bloomberg, StoneX

Gold:silver ratio averaged 84.7 in January to September; in October it was.82.9

Silver’s correlation with gold averaged 0.79 in January to September; in October it was 0.82.

Silver’s correlation with copper was 0.52 in January to September and 0.66 in October.

PLATINUM – flattering to deceive?

Total platinum volumes, September, 000 ounces

Source: LBMA

- Platinum traded more in line with gold than it did with palladium, which had its own fundamental issues. Some support, though, from continued headlines about the market share that is being taken up by PHEV vehicles at the expense of BEVs. BEVs are not falling; PHEV are growing more rapidly. The key to the impact on the market is that PHEV vehicles, being hybrid, have their own Internal Combustion Engines, which carry a PGM loading of some 10-15% higher than normal ICE vehicles. On the supply side, South African mine output stabilising and the majors are working off some of the concentrate backlog that built up during the load-shedding era of power cuts going back at least as far as 2021.

- Spot activity was just 2% higher than the January-September average, but down against September. The early price slippage was in thin spot conditions, but that picked up as the price reversal took place, for the usual reasons as outlined above. Forward buying activity picked up at this point also, with the turn not just influenced by gold but by the support at $950.

- Spot activity was then very variable through the rest of the rally, which lasted through to 30th October. Volumes did pick up once platinum was cleanly through $1,000 and as prices moved towards $1,060 forward volumes expanded as some industrial selling appeared.

- Activity in options was liveliest in mid-month as $1,000 was being challenged and the speed of the move higher suggests that long-side activity was dominant, targeting $1,100.

- The LLD sector was also very variable and the only days of any noticeable volume were on the bullish reversal early in the month, suggesting some possible industrial buying. Anecdotal evidence suggests Industry does appear to be on both sides of the market at present and this is borne out by the final increase in LLD activity at the top of the market at month-end.

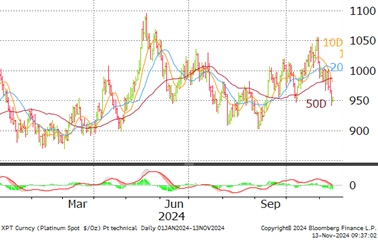

Platinum technical pattern, one-year view

ETFs: still nervous; just six days of net creations; monthly loss of 4.3t to 96.6t and year-to-date gain of 1.9t.

CFTC: gradually increasing confidence illustrated by 15 days of net creations from a total of 23 trading days and an increase of 0.8t over the month, to a total of 97t. Global mine production is ~170tpa.

Platinum, palladium and the ratio, January 2016 to date,

Source: Bloomberg, StoneX

PALLADIUM -spot volumes on 28th were at a near three-year high

Palladium spot volumes, September, 000 ounces

Source: LBMA

- After rallying through $1,100 in September from a low of ~$950, palladium stabilised in early October on a support level of $1,000 (although this gave way in November).after gradual gains in the first three weeks, prices exploded higher thereafter in the wake of suggestions from the US to G7 that sanctions should be imposed on Russian exports of platinum and palladium. Russian is the world’s largest palladium producer with 40% market (by-product of nickel) and of course it is vital in the tailpipe exhaust emission treatment (as indeed are platinum and rhodium). So this will not happen, but the suggestion was enough to light a fire under prices for a peak just before month-end of $1,250.

- The vast majority of the action in spot and forwards was in the days of the very sharp move as of the 14th, and volumes of 1.1M ounces on 28th was the highest since December 2021. There had been some action in the early consolidation above $1,000, suggesting some bargain hunting.

- This was followed by a pick-up in option activity suggesting a target of $1,050 or further. Everything tailed away in mid-month, given that the long-term fundamental outlook is still not good.

- The increased activity in forwards in the final week would suggest some industrial bargain hunting, while the big jump on the 24th, from $1,066 to $1,168, may well have been extended by hedging against a smart pick-up in option activity.

Palladium technical pattern, year-to-date

ETFs: also seeing improved interest, with 17 days of net creations for the addition of 4.5t to a total of 23.6t. Global mine production is ~190t.

CFTC: Outright shorts continued to contract and finished the month at 21t, down from an opening 35t and a record long of 67t just 12 weeks previously. Longs eased in the first half of the month, but then revived for a net gain of 5t or 49%

Spot platinum, palladium and the spread, January 2016 to date

Source: Bloomberg, StoneX

Latest articles

This data feed is not available at this time.

Data is currently not available