News & Insights

LBMA Precious Metals market volumes, November 2024, and their significance

Rhona O’Connell, StoneX Financial Ltd; 16 December 2024

Any views expressed here are of the writer and do not reflect a house view from NASDAQ.

Daily November average compared with daily average for November 2023—October 2024

Source: LBMA

Source: LBMA

Welcome to our monthly round-up of the LBMA OTC trading volumes in gold, silver, platinum and palladium, as recorded on a daily basis by the Association. These are split into spot, swap/forward, options and LoanLeaseDeposit (LLD) and give a flavour of the markets’ activity and how they were influenced by external forces and news items.

All references to COMEX or NYMEX positioning refer to Managed Money, not commercial positions.

General introduction: -

The swiftness of the US Presidential results and the clarity of the Republican / Donald Trump victories strengthened the dollar, boosted yields and extended the corrections from the October rallies in the precious metals, at least through the first half of November. All then recovered to one degree or another, but each lost ground over the month as a whole. Gold ended almost 3% down, silver by closer to 4%, platinum by 5% and palladium continued toflounder, shedding 11%. As the table above demonstrates, gold and platinum volumes picked up the most smartly in the options division, with silver and palladium gaining the most in spot.

Year-to-date, the price changes were as follows:-

Silver +29%

Gold +28%

Platinum minus 4%

Palladium minus 9%

Clearly the US election was the primary driver across the board to kick off with as a result of the impact on the collateral aeras of currencies and yields; by mid-month the dust had settled and fundamentals moved back in again. Palladium clearly continues to struggle although the recent evolution of the hybrid engines vs the batteries; plus the additional possibilities around the impact of the Trump administration on the auto sector may – may - mean that the PGM as a whole have something of a stay of execution. Gold continues to look at geopolitical risk and it is worth noting that some senior bankers in different regions are speaking publicly about the potential stresses in the system; and while silver remains on gold’s coat-tails to a large extent, it is still hampered by the state of the European economy and the slow crawl in the Chinese economic recovery.

Economic and Political Background

The United States

The swift result to the US elections, when the markets had been expecting a close call, possibly disputes, and a few days’ delay in a final result, brought about plenty of market activity. The dollar gained 4.5% from the 5th through to the 22nd of November as the ”Trump Trade” took over, also boosting equities (S&P 500 gained 5.2% over the month) and also boosting bond yields -(although that went into reverse towards month-end. Topics of debate obviously included the prospect for tariffs, although there is a groundswell of opinion that some of the more robust proposals that have come forth are likely to be opening salvos for negotiation.

There is also a widespread view that a number of President-elect Trump’s Cabinet selections include a number of individuals that could be regarded as “heavyweights” with plenty of experience, most notably Scott Bessent, who is the nominee for Secretary of the Treasury.

Meanwhile Fed Chair Powell, in his Press conference following the November meeting in which the FOMC cut rates again, noted in response to a question from the floor that the Fed has watched the run-up in bond rates and it’s nowhere near where it was a year ago, and also it is too early to really say where they will settle. He takes the view that the recent moves have not been driven by inflationary expectations, but more on a likelihood of stronger growth and perhaps less in the way of downside risks. He also made the clear statement that “We don’t guess, we don’t speculate and we don’t assume”. The employment numbers for October were reasonably solid, although a big drop in payroll gains resulted from hurricanes and strikes (subsequently the numbers for November were also sound, but not as strong as the market had been expecting).

In Europe the powerhouses of the zone, notably Germany and France, continued to return disappointing economic numbers and while they contributed to an independent weakness in the euro (thereby benefiting the dollar), leaving the European Central Bank with little choice but to implement back-to-back rate cuts in December. The Governing Council is reluctant to cut too quickly (although there is of course a variety of views among the members), but prevailing conditions meant that they have probably had little choice. On the political front the German Chancellor came under increasing pressure and the three-way coalition effectively collapsed; by month-end he had called a snap election for this coming February.

On the other side of the world, the Chinese Government continued to address the weakness in the economic recovery and continued concerns over the property market in particular and has implemented a series of stimulus measures, a programme that continued into November and went further in early December, with proposals to loosen monetary policy. – which helped to prompt a rally in gold.

So that more or less sets the scene for the development in the metals markets in November. Geopolitical uncertainty revolved around anticipation of which of Mr. Trump’s more robust programmes would be implemented and which would be watered down by a finely balanced Congress, plus continued concern over the febrile conditions in the Middle East. Allied to this was a number of central bankers voicing concerns about potential volatility or instability in parts of the banking sector and the moves towards shadow banking in some areas.

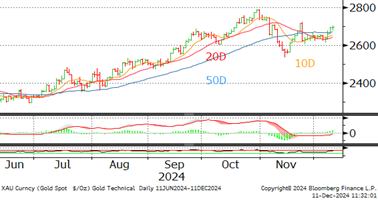

GOLD –consolidating post-election

Overall volumes and spot price, November

Source: LBMA

- By comparison with the daily average for the preceding 12 months, gold posted healthy gains in all sectors, notably options, which were up by 29%, with 21% gains in swaps/forwards and 13% in spot, while LLD was quiet, posting just 3% higher volume.

- Spot was at its busiest by far on the day after the election, with a massive 46.1M ounces (1,434t or the equivalent of five months’ global mine production). This was a three-month high, but even if this day’s trading were removed the daily average would have been 10% higher than the previous twelve months’ average. On the day in question gold dropped by $100 or 3.2% to just over $2,650.

- The fall continued to a low of $2,537 on the 14th, also in generally lively volume, suggesting profit taking and the clearing out of some weak-handed holders.

- The rally that ensued over the following week was in thin spot volume, until $2,700 was cleared, at which point more profit taking came in and volume in the forwards rebounded, suggesting that the market was not convinced of further upside potential

- Forwards and options had also been busy in the first part of the month, helping to push prices lower after the late-October failure at $2,800. It was when this had run its course on 14th November that the price started a sharp week-long rally .spurred by increased tension over Ukraine.

- Cementing the markets’ uncertainty over gold’s near term upside potential was lively activity in LLD during that rally.

- Eventually prices turned down again with a sharp drop on reports of a ceasefire agreement between Israel and Hezbollah. The rest of the month was quiet in all sectors.

Gold technical pattern; year to date

Source: Bloomberg, StoneX

ETFs: mixed; 15 days of net creation from a total of 23 trading days; net gain of 24t for a year-to-date loss of seven tonnes.

CFTC: fresh longs and fresh shorts. Longs dropped at the start of the month with prices easing, then reinstated and eased latterly, more or less in parallel with price action. Shorts rose steadily through the month, but not by much. End-month; longs at 771t and shorts at 104t.

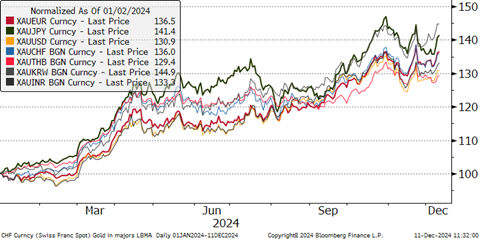

Gold in local currencies, year-to-date

Source: Bloomberg, StoneX

SILVER; shook out weaker holders – tamed by Europe, China economies

- November was the other way round from October as far as silver’s relationship with gold was concerned; initially they came off together and silver did rally with gold in the latter part of the month, but to a lesser extent. November opened on the high of $33.12, while the low was the day before month-end at $29.64, before finishing at just below $31.00.

- Perhaps unsurprisingly after the price action of the previous months and lively activity in the swap/forwards and LLDs, November, saw a contraction of 15% in swaps/forwards against the daily average of the previous 12 months, and LLDs were down by 9%. Options were up by just less than 2% but spot was better, posting volumes that were higher by 18%. The majority of the action, in all sectors, was at the start of the month, although spot and LLD did see a pick-up at month end as prices forced their way up through $30, suggesting a change of heart in spot, but continued desire to lock in any price strength in LLD.

- The liveliest action to start with came from swap and forwards, and silver’s drop through $33 is likely to have triggered this action – which then turned into something of a vicious circle as those sales capped any attempt at the upside.

- This then segued into the spot action on day four, where, in line with gold in the face of a clear US election result, silver dropped, with stale bull liquidation generating a 6% fall to below $32. A somewhat confused market then tried to rally, and this too was in high volume, but $32 proved insurmountable and generated a fall to just below $30 on the 14thh, the same day as gold bottomed.

- There was a minor uplift in LLD activity as silver went through $31, and prices faded thereafter.

- This mixed activity continues to reflect silver’s relationship with gold, but also the fact that it is still troubled by the weak economic activity in Europe and China; there may also be some concern creeping in over the potential for a change in “green” philosophy under the new US Administration given the importance of solar, and to a lesser extent, electrified vehicles, to silver demand.

Total silver volumes, September, M ounces

Source: LBMA

ETFs; the buyers had the upper hand; 13 days of net creation for a gain of 716t; year-to-date gain of 1,368t. Global annual mine production is ~26,000t.

CFTC: longs traced a similar path to gold – and to the silver price, for a small net gain overall, while shorts contracted over the first half but then expanded again especially towards month-end as prices challenged $35.

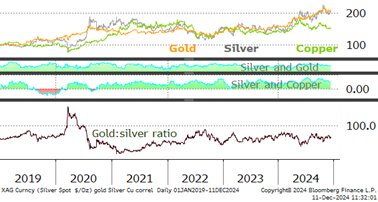

Silver, gold and copper; the correlations and the gold:silver ratio, medium term

Source: Bloomberg, StoneX

Gold:silver ratio averaged 84.5 in January to October; in November it was.85.4

Silver’s correlation with gold averaged 0.80 in January to October; in November it was 0.79.

Silver’s correlation with copper was 0.54 in January to October and 0.58 in November.

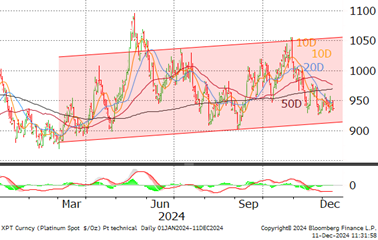

PLATINUM – still struggling but building scope for a short-covering rally - eventually

Total platinum volumes, November, 000 ounces

Source: LBMA

- Platinum traded more or less in line with gold in November, initially outperforming gold, but then crossing below it (on a rebased basis) on the 20th. Ironically this reversal of fortune coincided with press coverage of a major water supplier in South Africa introducing “demand-management” its supplies. The company in question has contracts for bulk-supply to Impala and Northam. Thus far there has been no media statement from either company but the news, along with public comment about Eskom looking to raise its electricity tariffs by up to 40% (not expected to be that high) highlighted that continued risk / cost implications in the South African PGM mining industry.

- With the exception of the 26th November, which was the final downward day before an attempted change in trend, the busier period in spot trade came in the first half of the month, especially straight after platinum’s drop below $1,000. This move also prompted activity in the options markets, although the other derivative segments were quiet.

- In fact the LLD market, at 29% below the previous 12-month average, was more or less dormant right through the month, reflecting reduced industrial activity. A similar case can be made for swaps and forwards, at 5% below the previous average and in which there was only one day of noticeable volume. And it was a big day, with over a million ounces going through against an average over the rest of the month of just over 451,000 ounces. This came on the 8th, (options were still busy at this point) when platinum traded to the downside, from $1,002 down to $966 before a small rebound into the close. This was largely ascribed to profit takngi and stale bull liquidation.

- In the second half of November, once again the strongest volume was on the day when platinum put in a low of $928 as the trend turned and a half-hearted rally ensued, up towards $980. Industrial activity was lame, however, and the market continued to struggle to find support.

- In the background Anglo American continued with its divestment of Amplats, implementing an accelerated book build for the sale of 6% of the company (~16M shares) after selling a slightly smaller amount in September. The company has said that it will not reduce its holding any further until the demerger in mid-2025.

Platinum technical pattern, one-year view

ETFs: picking up some interest with eleven days of net creations; monthly gain of 2.5t to 99.4t and year-to-date gain of 7.6t. Global mine production is ~170tpa.

CFTC: the reverse of ETFs with light liquidation of Managed Money longs (some bargain hunting in mid-month). Shorts, by contrast, increased sharply, fanning out from 30.2t to 47.6t.

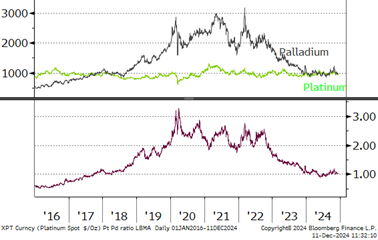

Platinum, palladium and the ratio, January 2016 to date,

Source: Bloomberg, StoneX

PALLADIUM - still beleaguered and encountering continued industrial de-stocking

Palladium spot volumes, November, 000 ounces

Source: LBMA

- Palladium slithered lower in the first half of November, dropping from $1,150 to the month’s low of $921 (on the 14th) as the market initially came to terms with the strong unlikelihood of any sanctions on Russian material and the reality of the longer-term fundamentals re-established itself. The evolution of the electrified vehicle sector continues to work in the PGMs’ favour with hybrids doing better than BEVs, and increasing signs that consumer resistance is having its inevitable impact; add to this the potential dilution of the Inflation Reduction Act by Trump Administration and the picture is not as dark as it was. There is a long way to go through before – if – we can say that palladium’s prospects are getting much better.

- Spot volumes were 30% higher than the previous 12-month average although they were skewed by two particularly heavy days (over a million ounces each) that lifted the average. Excluding those days the daily average would have been just over 666,0000 ounces, which is still a healthy 22% higher than the previous 12 months.

- The first really heavy day was the day after the Presidential election and one would have thought, if anything, that the result thereof might have given palladium a respite. Not a bit of it. The downward path continued with spot dropping through $1,050 oni that day aided by lively action in the LLD and the crossing of the 50-day average.

- As the $1,000 level came into view, volumes in options picked up as did swaps/forwards, suggesting some industrial interest, but that was not enough at that stage to stem the tide.

- As we see so many times, the next big day in spot was when the trend changed as bargain hunting developed at below $950 and as prices turned upwards, so the options segment revived again, suggesting that $1,000 was the target for the second time. The approach to $1,050 saw more industrial selling and, with the 20-Day average having moved below the 50-Day in the “Death Cross”, the month ended on a sombre note. Dropping below $1,000 once more.

Palladium technical pattern, year-to-date

ETFs: seeing steady but slower interest, with 13 days of net creations for the addition of 0.9t to a total of 24.7t. Global mine production is ~190t.

CFTC: heavy liquidation early in the month, reversing the buying interest of late October on the lack of price follow-through, accompanied by increasing shorts until some light covering in the final week.

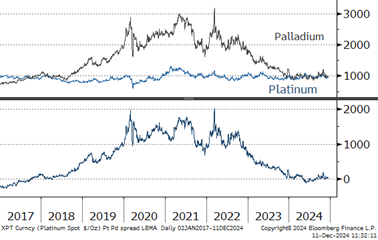

Spot platinum, palladium and the spread, January 2017 to date

Source: Bloomberg, StoneX

Latest articles

This data feed is not available at this time.

Data is currently not available