Honeywell International’s HON growth is supported by strong demand and backlog levels. In the third quarter of 2022, backlog increased 9% year over year, owing to strength in Aerospace, Performance Materials and Technologies and Honeywell Building Technologies.

The company’s investments in digital transformation, aimed at driving commercial and operational actions, are helping in margin expansion. Segment margin expanded by 60 basis points year over year to 21.8% in the third quarter. Pricing actions and cost-control measures are also supporting the company’s margin performance. HON expects a segment margin of 21.6-21.8% for 2022 compared with 21.3-21.7% anticipated earlier.

Strong commercial aftermarket demand owing to a recovery in commercial flight hours is aiding Honeywell’s Aerospace segment despite volume softness due to supply-chain woes. Continued improvement in flight hours and build rates should drive the segment’s performance. For the full year, the company, carrying a Zacks Rank #3 (Hold), expects Aerospace sales to increase in mid-single-high single digits year over year.

Strong fire products and building management system sales are driving growth of the Building Technologies segment despite parts shortages due to supply-chain woes. The company predicts double-digit organic sales growth for the segment in 2022.

While the Safety and Productivity Solutions segment is weighed by lower personal protective equipment and warehouse automation volume, strength in advanced materials business and UOP operations is fueling growth of the Performance Materials and Technologies segment. The UOP business growth is led by strength in gas processing orders, while strong demand in the Marine Products business is a key growth driver for Advanced Materials.

Honeywell’s upbeat guidance raises optimism in the stock. For the fourth quarter, the company expects sales to increase 10-13% on an organic basis. For the full year, HON expects organic growth of 6-7%. Adjusted earnings are estimated to jump 18-22% year over year in the fourth quarter. For the full year, the company improved its adjusted earnings per share guidance to $8.70-$8.80 from $8.55-8.80 expected earlier. This indicates year-over-year growth of 8-9%.

Honeywell’s consistent measures to reward its shareholders through dividends and share buybacks are encouraging. In the first nine months of 2022, HON rewarded shareholders with $2.8 billion through share repurchases. For 2022, the company expects to buy back shares worth at least $4 billion. The quarterly dividend rate was hiked by 5.1% in September 2022, marking its 13th increment since 2010. Strong free cash flow generation supports the company’s shareholder-friendly activities. It expects free cash flow of $4.70-$5.10 billion in 2022. Such diligent capital deployment strategies boost shareholders' wealth.

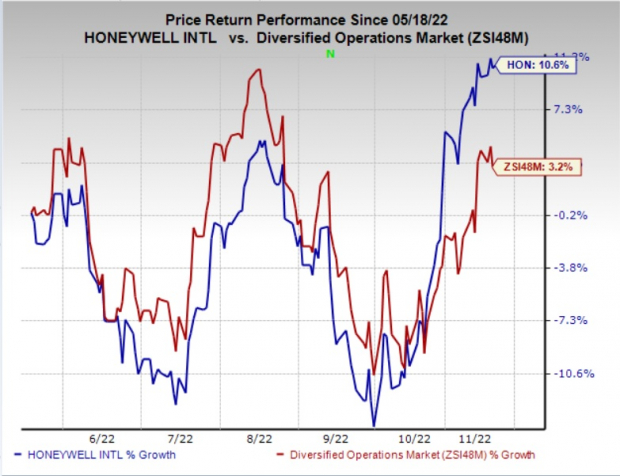

Due to the above-mentioned tailwinds, shares of Honeywell have gained 10.6% in the past six months, outperforming the industry’s 3.2% increase.

Image Source: Zacks Investment Research

Key Picks

Here are some better-ranked companies for your consideration:

Enerpac Tool Group Corp. EPAC delivered an average four-quarter earnings surprise of 3.4%. EPAC presently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks.

Enerpac Tool’s estimated earnings growth rate for the current fiscal year is 44.6%. Shares of the company have jumped 21% in the past six months.

Applied Industrial Technologies, Inc. AIT presently carries a Zacks Rank #2 (Buy). The company delivered a trailing four-quarter earnings surprise of 24.8%, on average.

Applied Industrial has an estimated earnings growth rate of 14.3% for the current fiscal year. Shares of the company have gained 22.7% in the past six months.

IDEX Corporation IEX presently has a Zacks Rank of 2. IDEX pulled off a trailing four-quarter earnings surprise of 5.7% on average.

IDEX has an estimated earnings growth rate of 28.3% for the current year. Shares of the company have rallied 27.5% in the past six months.

Zacks Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s a little-known chemical company that’s up 65% over last year, yet still dirt cheap. With unrelenting demand, soaring 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail investors could jump in at any time.

This company could rival or surpass other recent Zacks’ Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Honeywell International Inc. (HON): Free Stock Analysis Report

Applied Industrial Technologies, Inc. (AIT): Free Stock Analysis Report

IDEX Corporation (IEX): Free Stock Analysis Report

Enerpac Tool Group Corp. (EPAC): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.