Swiss healthcare company Roche Holding (OTC: RHHBY) doesn't trade on the NYSE or NASDAQ, so the company is sometimes overlooked considering its size, scope and consistent revenue growth.

Roche, with its roughly 140,000 employees, has increased revenue by 36% over the past 10 years and annual earnings per share (EPS) by 27% in that period.

However, over the past year, its shares have fallen 27%.

There are two likely reasons for the decline of Roche's shares. One, despite an up year for revenue in 2022, it is likely that its diagnostics sales will drop in 2023 because of fewer COVID-19 tests. The company, in its annual report, said the impact of reduced COVID-19 sales would bring down 2023 group sales to the low single digits.

The second reason is the company's trial failures last year. The best-known was the shuttering of trials for Alzheimer's therapy Gantenerumab. That decision came after the company announced in its mid-yearearnings callthat it was ending trials for prostate cancer therapy RG7440, metabolic disease drug G6338, breast cancer drug Giredestrant, and asthma drug RG6173.

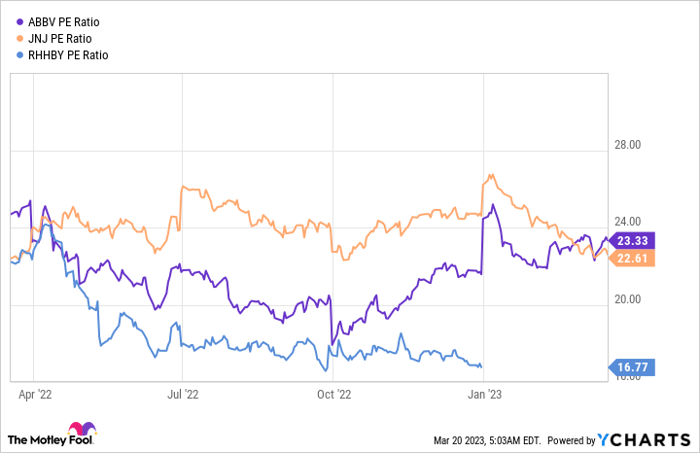

Despite the negative news, there are plenty of reasons to like the 125-year-old company's stock, which trades at around 17 times earnings, below the pharmaceutical industry average and below similar competitors such as Johnson & Johnson and AbbVie.

ABBV PE Ratio data by YCharts.

Here are a few reasons to like Roche stock:

Consistently strong performance

The company, which operates in two segments, Pharmaceutical and Diagnostic, had strong earnings in 2022, with CHF 62.3 billion in revenue, up 1%, and yearly EPS of CHF 20.30, up 2%.

While Pharmaceutical sales were up 1% to CHF 45.5 billion, Diagnostic sales were CHF 17.7 billion, flat year over year. The company said it expects declining revenue this year from COVID-19-related tests, but that should be made up by increasing revenue from two new products. Vabysmo, approved by the Food and Drug Administration (FDA) last January to treat two serious eye diseases, brought in $639.4 million in revenue, and Lunsumio, approved on Dec. 28 by the FDA to treat relapsed or refractory lymphoma, has the potential for $2 billion in peak annual sales.

Big portfolio, huge pipeline, recent approval success

The company's top-selling drug is multiple sclerosis therapy Ocrevus, which had CHF 6 billion in revenue in 2022, up 17%.

The company has a particular focus on oncology therapies, which makes sense. According to a report by Precedence Research, the oncology market is expected to grow from $286 billion in 2021 to over $581 billion by 2030, a compound annual growth rate of 8.2%.

Roche has multiple oncology blockbusters, led by breast cancer therapy Perjeta (CHF 4.087 billion in 2022 sales) and Tecentriq, approved for urothelial carcinoma and non-small cell lung cancer (CHF 3.717 billion). Roche's other top-selling oncology therapies include Herceptin, approved to treat stomach cancer and breast cancer (CHF 2.142 billion), and Avastin, approved to treat ovarian cancer, cervical cancer, kidney cancer, and glioblastoma (CHF 2.122 billion).

The most promising drug in the pipeline may be Glofitamab, which has shown promise to treat patients with relapsed or refractory diffuse large B-cell lymphoma (DLBCL). Glofitamab is a bispecific antibody that recruits T cells to fight tumor cells.

Another drug showing potential is Fenebrutinib, which is in a Phase 3 trial to treat relapsed and primary progressive multiple sclerosis. The drug is a Bruton's tyrosine kinase (BTK) inhibitor.

Since the start of the year, the company's newer drug candidates have made big news. On March 10, Polivy, used in combination with Rituxan plus cyclophosphamide, doxorubicin, and prednisone (R-CHP) on previously untreated patients with DLBCL, gained an 11-2 approval vote from the FDA's Oncologic Drugs Advisory Committee. It's the first treatment in over two decades to show clinically meaningful improvement over the standard of care for first-line DLBCL. The FDA is expected to make a decision on the drug's approval by April 2. The drug has the potential for $2.4 billion in peak sales, analysts have said.

In February, Vabysmo met its primary endpoint in two trials to treat macular edema from branch and central retinal vein occlusion. If approved, it would be the third indication for the therapy, in addition to "wet" age-related macular degeneration and diabetic macular edema.

The company also received a label expansion from the FDA for Ventana PD-L1 as an assay to identify non-small cell lung cancer patients eligible for treatment with Libtayo, a PD-1 inhibitor developed by Regeneron.

Roche has a huge pipeline of 160 programs, including 47 in Phase 3 trials. Some of those late-stage therapies will likely pay off, helping the company to replace sales of its top drugs that are facing biosimilar competition, such as Rituxan, Herceptin, and Avastin.

An above-average dividend

Roche just raised its annual dividend by 2% to $1.29 per share, which equates to a yield of around 3.5%, double that of the typical S&P 500 dividend. Its dividend payout ratio of roughly 49% means the company can likely continue to increase its dividend.

Roche spends big to stay big

The reason Roche's pipeline is so large is that it is willing to spend more money on research and development than other pharmaceutical companies. In 2021, the magazine Drug Discovery and Development studied the top R&D pharmaceutical spenders, and Roche spent 27% of its revenue on R&D, a much larger share than any other large pharmaceutical.

Coming up with new therapies isn't cheap, and there are bound to be a few failures along the way, but Roche spends to keep finding novel therapies to replace the ones that will eventually lose exclusivity. It's already looking long down the road, and this stock is a good pick for long-term investors, particularly at its current price.

10 stocks we like better than Roche Ag

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Roche Ag wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of March 8, 2023

Jim Halley has positions in AbbVie and Johnson & Johnson. The Motley Fool recommends Johnson & Johnson and Roche Ag. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.