News & Insights

Key Points

- July saw a meaningful rotation within the equity markets spurred by increased expectations of Fed rate cuts beginning in September.

- U.S. small caps (tracked by the Russell 2000 Index) outperformed the Nasdaq-100 Index® by 11.7% in July—the largest relative monthly outperformance since April 2002 and the sixth largest monthly outperformance of all time going back to 1985.

- While other 2024 laggards and rate sensitive areas benefitted as well in July amidst the rotation, concerns over an economic slowdown have intensified leading to a near-term reversal of some popular strategies that have worked year-to-date.

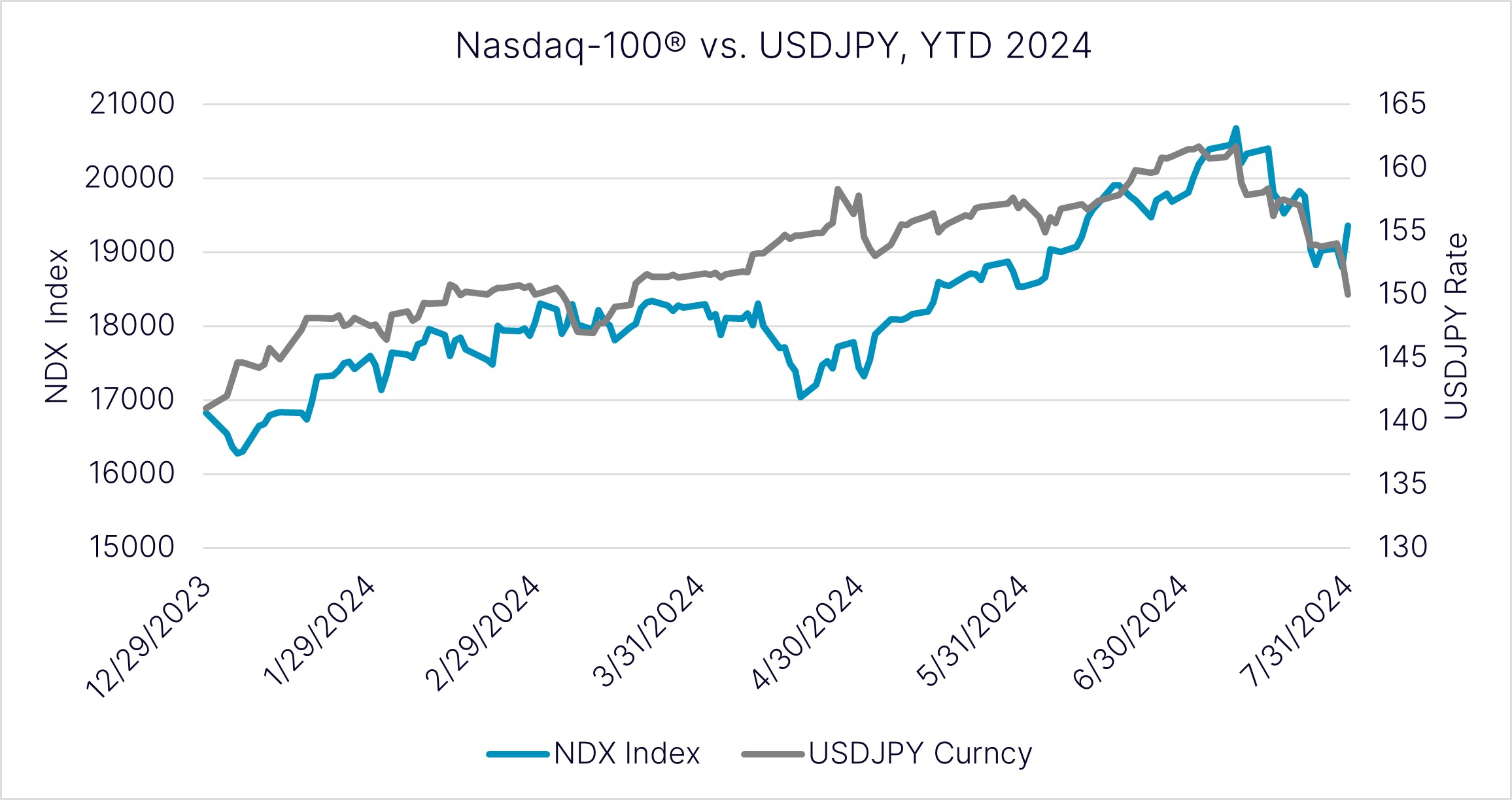

Chart of the Month

Executive Summary

July 2024 was a volatile month and has continued thus far in August as equity volatility (VIX Index) had its largest intraday spike in history going back to 1992 on August 5th—even eclipsing March 2020. This volatility was reflected in July with performance across Nasdaq’s suite of indexes displaying a pronounced level of variability across different markets and strategies, exacerbated by positioning and heightened geopolitical risks. Following a softer June CPI report, a weaker July ISM manufacturing report, and then an increase of 114,000 jobs versus expectations of 175,000 and the U.S. unemployment rate rising to 4.3% in July—highest level since October 2021—the markets have, again, moved aggressively in pricing in up to four Fed rate cuts over the final three meetings in 2024, beginning with expectations of a 25 to 50 basis point cut in September. This caused a meaningful leg down in U.S. Treasury yields as the 10-year yield closed the final week of July with its largest weekly drop since March 2022. Concurrently, the Bank of Japan increased the cost of borrowing for only the second time in 17 years, spurring the yen to appreciate by 11% since its low versus the U.S. dollar in mid-July. The yen’s recovery this month has been accelerated by the unwinding of popular carry trades, where investors borrowed in yen to fund the purchase of higher-yielding currencies and other risk assets. This yen unwind fed into Japanese equities—a favored strategy in 2024—as the Nikkei 225 has fallen by over 25% since its peak which coincided with the yen lows in mid-July. As investors have scrambled to mitigate losses from faltering carry trades, they have been compelled to liquidate assets in other markets, intensifying the sell-off in global tech and AI-related stocks. At the same time, mega cap tech earnings have come in mixed, with an uptick in investor concerns around the outlook for AI-related investments and expenses. The Nasdaq-100® (NDX®) retreated by 1.6% in July and, as of the time of this writing, has fallen deeper into correction territory as it is now down by around 12.5% from its mid-July peak—though it remains up about 7.5% for 2024 (as of August 6).

Nasdaq Indexes July 2024 Performance Recap

Among the 119 indexes tracked in this report, 84 finished positively, while 35 ended the month with negative returns. The average return across all indexes was 2.6%.

Nasdaq Featured Indexes

Last month’s laggard played catch up in July, with investors pivoting to small cap equity stocks, which are more sensitive to interest rate cuts. The small-cap Nasdaq Innovators Completion Cap™ (NCX™) gained 12.8%, making it the best-performing of the Nasdaq Featured Indexes in July. Conversely, the Nasdaq-100 Dorsey Wright Momentum™ (NDXDWA™) fell 8.3%, making it the worst performer among all indexes covered by this report as the momentum factor suffered in July amidst the rotation.

Nasdaq Global Indexes

The Nasdaq Global Indexes had an average gain of 2.8% in July. As investors shifted into small caps, the Nasdaq US Small Cap™ (NQUSS™) was the standout performer, gaining 9.4%. The Nasdaq Emerging Markets™ (NQEM™) was the only index that delivered a negative return in the group, falling 0.6%--driven by declines in the technology space.

Nasdaq Thematic Tech Indexes

Performance was mixed across the Nasdaq Thematic Tech lineup, which finished July with an average return of 0.6%. The ISE Mobile Payments™ (IPY™) was the top performer overall, rising 6.8%. Other areas of strength included the Nasdaq Biotechnology® (NBI®) and KBW Nasdaq Financial Technology™ (KFTX™), up 6.6% and 5.6%, respectively. With over one-third of its constituents (including AMD, Lam Research and Applied Materials) seeing double-digit losses in July, the PHLX Semiconductor™ (SOX™) was the laggard of the group with a decline of 4.4%, reflecting the aforementioned rotation out of tech in July.

Nasdaq Thematic Renewables and Energy Transition Materials

Performance was mixed across the lineup, which finished July with an average return of 1.1%. The Nasdaq Clean Edge Green Energy™ (CELS™) was the top performer of the suite with a gain of 7.5%. The laggard of the group was the Nasdaq Sprott Junior Uranium Miners™ (NSURNJ™), falling 6.9%.

Nasdaq Dorsey Wright

Most indexes in the suite rose in July, delivering an average return of 3.0%. The best performer was Dorsey Wright Financials Technical Leaders™ (DWFN™), rising 9.9%. The Dorsey Wright Emerging Markets Technical Leaders™ (DWAEM™) underperformed its peers, dropping 4.2%. Consistent with the broader market trend, financials and small caps gained strength, while technology and emerging markets struggled last month.

Nasdaq Dividend and Income Indexes

Overall, July was a strong month for the suite which rose 4.8% on average—benefitting from the decline in rates which makes higher dividend and income areas more attractive. The Nasdaq US SMID Cap Rising Dividend Achievers™ (NQDVSMR™) led the way in terms of performance, rising 9.9%. The Nasdaq Emerging Markets High Equity Income™ (NQEMHEI™) was the sole index in the group to post a negative return, declining by 3.1%.

Nasdaq Multifactor Indexes

All indexes in the group posted a positive return, which finished July with an average gain of 4.7%. The Nasdaq Victory US Small Cap High Dividend 100 Volatility Weighted™ (NQVWSD™) substantially outperformed its peers, gaining 11.3%, while the Nasdaq AlphaDEX Large Cap Growth™ (NQDXUSLCG™) only rose 0.5%.

Nasdaq Financial Sector Indexes

Performance for financial sector indexes was overwhelmingly positive in July, as all the indexes finished in positive territory with an impressive gain of 10.6% on average. The best-performing index of the group was the KBW Regional Banking™ Index (KRX™), rising 18.6%. This was followed by the KBW Premium Yield Equity REIT™ Index which rose by 12.0% as this higher-yielding, “bond proxy” cohort benefited from the decline in rates, and then by the PHLX Gold/Silver Sector™ Index as precious metals rose amidst the increased prospects of Fed rate cuts.

Nasdaq Options and Other Quantitative Indexes

Performance for the group was mixed in July, achieving an average return of 0.01%. The Credit Suisse Nasdaq Gold FLOWS103 TR™ (QGLDITR™) was the top performer of the suite with a gain of 3.8%. The Credit Suisse Nasdaq WTI Crude Oil FLOWS106 TR™ (QUSOITR™) had the worst performance in the group, declining by 1.7%.

Nasdaq Crypto Indexes

Performance was mixed across the Nasdaq Crypto lineup, which finished July with an average return of 4.0%. The Nasdaq Bitcoin™ (NQBTCS™) emerged as the top performer with a gain of 8.5%. The Nasdaq Ethereum™ (NQETHS™) was the only index that delivered a negative return in the group, falling 3.4%.

Disclaimer:

Nasdaq® is a registered trademark of Nasdaq, Inc. The information contained above is provided for informational and educational purposes only, and nothing contained herein should be construed as investment advice, either on behalf of a particular security or an overall investment strategy. Neither Nasdaq, Inc. nor any of its affiliates makes any recommendation to buy or sell any security or any representation about the financial condition of any company. Statements regarding Nasdaq-listed companies or Nasdaq proprietary indexes are not guarantees of future performance. Actual results may differ materially from those expressed or implied. Past performance is not indicative of future results. Investors should undertake their own due diligence and carefully evaluate companies before investing. ADVICE FROM A SECURITIES PROFESSIONAL IS STRONGLY ADVISED.

© 2024. Nasdaq, Inc. All Rights Reserved.

Latest articles

This data feed is not available at this time.

Data is currently not available