Credit: Shutterstock photo

Credit: Shutterstock photoBy Peter E. Greulich :

Most long-term shareholders seek a balance between risk and reward. It is one of the most basic questions an investment adviser asks a potential customer: "What is the amount of risk you want to bear for any given reward?" As was covered in a previous article, even though IBM (NYSE: IBM ) has spent $190 billion on share buybacks, its twenty-first century returns have underperformed some common indexes. So far in this century, a long-term shareholder would have received higher returns by investing in a low-cost, index mutual fund.

In addition to these subpar returns, there is a new, ever-growing risk: shareholders' equity less goodwill. This risk is exaggerated at IBM because of the corporation's: (1) opaque handling of the successes and failures of its 177 acquisitions since 2001 and (2) inability to retain or make more productive the best-of-the-best of these acquired human assets. This means that IBM's executive team has suffered the ongoing loss of what financial analysts consider an "intangible."

IBM for almost two decades has been suffering continual losses of its most valuable, intangible asset: its human assets. Too many analysts downplay this trend not only at IBM but within the knowledge industry in general because, to them, human assets are intangible. But because of an accounting change in 2001, these human assets are now quite tangible.

Shareholders need to hold IBM's executive team accountable for its handling of this important corporate asset because even as their investment returns stagnate, risks are climbing.

Shareholders' equity less goodwill is significantly negative

Understanding shareholders' equity less goodwill

An intangible asset is something that, if dropped on your toe, doesn't leave a mark. Its value is open to personal interpretation, imagination, and creative thinking. For the purposes of this article, intangible assets are considered in two ways: first, the goodwill that arises from an acquisition; and second, all other intangible assets - such as patents, brand image, customer relations, non-binding contracts, and strategic alliances. Goodwill is the difference between the full amount paid for an acquisition, less all other intangible and tangible assets.

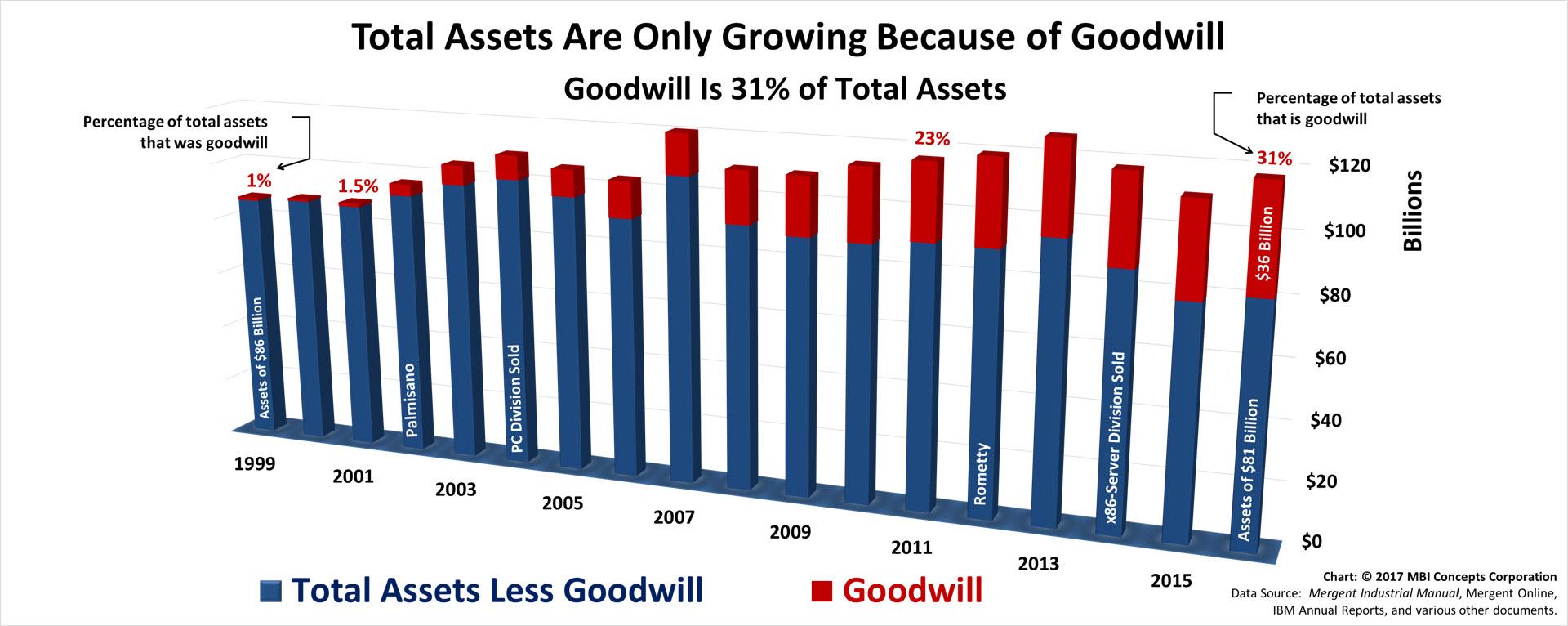

For instance, in its 2004 annual report, IBM documented the 2002 acquisition of PricewaterhouseCoopers Consulting (PwCC) for $3.89 billion. Of the purchase price, IBM estimated that PwCC had $320 million in tangible assets (current and fixed assets - chairs, desks, computers, buildings, etc. - less current and non-current liabilities), and $410 million in "other" intangible assets (strategic alliances, client relationships, and customer contracts). The remaining $3.16 billion - 81% of the purchase price - was listed as goodwill: specifically, the value of the acquired assembled workforce, synergies gained from combining PwCC and IBM, and the premium paid to gain control.

Of the $52 billion paid for its 177 acquisitions since 2001, $36 billion is still carried today as goodwill - 70% of all acquisition dollars. This goodwill carries no inherent value and, in a worst-case scenario such as bankruptcy, it would have little or no monetary worth. Although IBM's total assets have grown by 34% since 1999, this growth is a mirage created by an ever-increasing percentage of goodwill. In the same time frame, its total assets less goodwill has declined from $86.5 billion to $81.3 billion.

From IBM there has been only silence for too long. Since 2001, goodwill has been a growing industry problem, and IBM is the industry's poster child for bad behavior. To believe that every one of its monthly acquisitions for the last sixteen years has been handled appropriately and still retain their goodwill valuation, some of which was assigned more than a decade ago (like the $3 billion for PwCC), breaches the boundaries of the believable and credible. The executives of the corporation seem to deem it better to remain dense, silent and opaque rather than shining a light into the darkness. As a result, IBM's goodwill by being too much of a good thing wrapped for too long in too little transparency should be regarded as an exposure to a significant goodwill impairment.

IBM's goodwill smells rank: it is goodwill gone bad.

IBM's drill presses are growing legs and walking out the door

The oxymoron - bad goodwill - may only become more prevalent within the high-tech and knowledge industries as the century progresses. When a high-tech corporation takes a goodwill impairment, it should be asked if its leadership understood that the success of their acquisition depended on integrating the knowledge and expanding the productivity of the acquired workers.

Peter F. Drucker predicted the growing value of these knowledge workers. He believed that the knowledge worker would become this century's critical asset and now, because of a goodwill accounting change, it is finally possible - like never before - to visualize their expected economic impact in charts and graphs derived from data living in a financial spreadsheet. Drucker's intangible is now completely tangible: in the case of IBM, it has acquired employees that it has estimated are worth some $36 billion in goodwill. Unfortunately, they are being involuntarily exited without regard to their individual value, performance or productivity, and increasingly, they are hitting the exits under their own power.

Shareholders investing in a manufacturing concern expect the executive team to care for its material assets. An ongoing loss of manufacturing assets is the sign of an incompetent management team. Bookkeepers see red when a tool - such as a drill press that is purchased to get a job done - suddenly disappears because of theft or poor maintenance. If a manufacturing executive tried to explain away decades of such losses, the chief executive would be the first to ask emphatically, "What! Did the drill presses grow legs and walk out the door? Did you not hear the bearings squeaking from the lack of maintenance?"

IBM's dropping sales and profit productivity is a result of the latter - the lack of proper lubricants to maintain and improve employee productivity. In the case of the former, each of IBM's fastest growing intangible assets came fitted with a pair of legs and a quite elegant, functional brain that serves double duty as a smoke detector. More and more often these brains are telling their owner's legs to evacuate the premise before the corporate building collapses upon itself. Figuratively, IBM's drill presses - the people the company purchased to get a job done - are walking out its exit doors on their own volition.

Financial analysts that cover the knowledge industry should be seeing red when human assets that are acquired at a premium are misused, discarded or lost through poor human relations practices. Failing to acknowledge this red ink on a timely basis, if not an accounting mistake, is an ethical lapse that exposes an investor to long-term, unnecessary financial risks.

Without fundamental change, IBM's decline, although slow, will continue

When a new chief executive takes charge, he or she must do what other successful executives at IBM have done to ensure a fresh start: wipe the slate clean of his or her predecessor's non-productive processes, products, and tangible and intangible assets (In 1956, Watson Jr. called a constitutional convention for feedback from his executive team on how to move forward). One of these actions should be to write off the corporation's bad goodwill. When this impairment is finally taken, it will punctuate a two-decade long deterioration in employee productivity, and the outright loss of critical employees through resource actions and resignations.

These goodwill impairments will reveal to the chief financial officers in the knowledge industry something that has been intuitively obvious to their manufacturing counterparts for over a century: warehouses, even virtual warehouses, need to be continually refreshed and refilled with new products of significantly higher value, not filled with the stale vestiges of value remaining from yesteryear; manufacturing facilities, especially virtual, high-tech manufacturing facilities distributed worldwide in home offices, need human assets that are self-motivated, creative, engaged and passionate about their work; intangible human assets, like their tangible counterparts, need investment and ongoing maintenance to perform their jobs and to achieve their estimated goodwill value; and, finally, the business must first invest in making people more productive, processes more effective, and products more valuable, before exchanging one form of paper - greenbacks - for another form of paper through stock buybacks.

To Drucker's credit, the twenty-first century growth of goodwill in the knowledge industry is documenting his twentieth century assertion of the growing value of human assets to a corporation. The disregard IBM's chief executives have shown in valuing, retaining and making these assets more productive demonstrates how they have lost touch with their corporation's institutional memory: they no longer understand the essence of the most basic of human financial equations - that an enthusiastic, engaged and passionate employee is a productive employee.

As a result, factor into your investments a significant goodwill impairment at IBM. It is just a matter of time and transparency, or one triggering event that the board of directors should ensure comes sooner rather than later: a change of direction and leadership.

This article is an excerpt (with some changes and additions) from THINK Again: IBM CAN Maximize Shareholder Value .

See also The Vision Is Clear: Listen To Merck And Invest In Microcap KalVista Pharmaceuticals on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}