Hewlett Packard Enterprise HPE has enjoyed a stellar 41.1% surge year to date (YTD), outperforming the Zacks Computer - Integrated Systems industry’s return of 16.6%. The stock has also outperformed its peers in the space, including Micron MU, Seagate Technology STX and Advanced Micro Devices AMD.

YTD Price Return Performance

Image Source: Zacks Investment Research

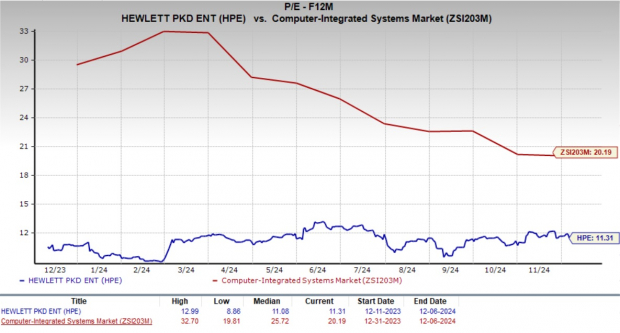

Despite this impressive performance, HPE still trades at a price-to-earnings (P/E) multiple lower than the industry average, raising the question: Is this the right time to buy, sell or hold the stock?

While the company’s discounted valuation may seem like an attractive entry point, a closer look at HPE’s financial results, segmental performance and guidance reveals significant headwinds. For now, selling the stock appears to be the most prudent choice.

Image Source: Zacks Investment Research

HPE’s Impressive Rally: A Reflection of Past Strength

Hewlett Packard Enterprise’s YTD rally has been supported by strength in key segments, particularly GreenLake and AI systems. There is massive traction in the adoption of HPE GreenLake as organizations are benefiting from the flexibility and scalability of this IT transformation solution.

GreenLake’s customer base grew nearly 34.5% year over year to 39,000 in the fourth quarter of fiscal 2024. This growth in customer base has contributed to an annualized revenue run rate that has increased 48% year over year, reaching more than $1.9 billion at the end of the fiscal fourth quarter.

Hewlett Packard Enterprise is experiencing persistent demand for its AI system offerings. In the fourth quarter of fiscal 2024, Hewlett Packard Enterprise reported that it had $6.7 billion in cumulative orders for AI products and services since the first quarter of fiscal 2023. HPE’s new AI orders in the fiscal fourth quarter of 2024 have brought its backlogs to a value of $3.5 billion.

However, much of this growth appears to be baked into the stock price, given the 41% YTD gain, which has already outpaced the broader technology sector. With limited near-term catalysts and intensifying competition, HPE’s valuation advantage may be less of a bargain than it seems.

Near-Term Headwinds for HPE

While Hewlett Packard Enterprise is capitalizing on the rise of AI and making strides in this space, the company is also facing certain challenges. HPE’s intelligent edge division is facing pressure from the accumulation of inventory levels among HPE’s customer base. Revenues in the Intelligent Edge division plunged 20% year over year in the fourth quarter of fiscal 2024. In this segment, HPE’s switching and campus solutions are experiencing weak demand.

Moreover, due to the low mix of high-margin Intelligent Edge revenues, HPE’s gross margin is also pressured. In the fiscal fourth quarter, HPE’s non-GAAP gross margin contracted 390 bps on a year-over-year basis and 90 bps on a quarter-over-quarter basis to 30.9%.

HPE’s financial services division is also experiencing a lower single-digit growth. The Financial service segment’s revenues of $893 million increased 2% year over year in the fiscal fourth quarter of 2024. The weakness in these two segments has partially been due to softening IT spending.

Higher interest rates and inflationary pressures are hurting consumer spending. On the other hand, enterprises are postponing their large IT spending plans due to a weakening global economy amid ongoing macroeconomic and geopolitical issues.

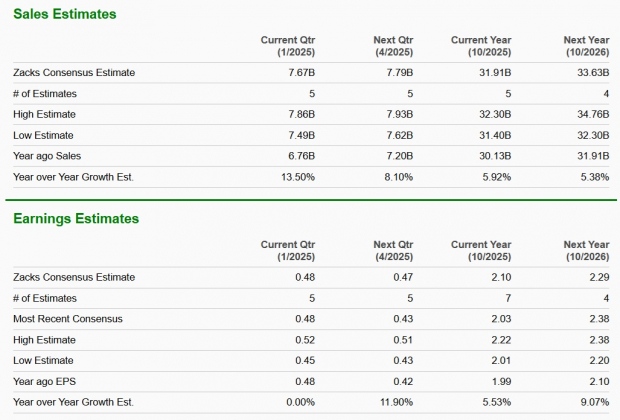

The Zacks Consensus Estimate for fiscal 2025 and 2026 top and bottom lines does not depict a strong financial recovery in the near term for the company.

Image Source: Zacks Investment Research

What Should Investors Do?

Hewlett Packard Enterprise has had a strong run in 2024, driven by impressive gains in AI systems and hybrid cloud solutions. However, it is going through a myriad of transitions and challenges, making the stock’s current market position a little volatile.

Given the challenges, selling HPE stock now allows investors to lock in gains from this year’s rally while avoiding potential downside risks. Hewlett Packard Enterprise carries a Zacks Rank #4 (Sell) at present.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Free Today: Profiting from The Future’s Brightest Energy Source

The demand for electricity is growing exponentially. At the same time, we’re working to reduce our dependence on fossil fuels like oil and natural gas. Nuclear energy is an ideal replacement.

Leaders from the US and 21 other countries recently committed to TRIPLING the world’s nuclear energy capacities. This aggressive transition could mean tremendous profits for nuclear-related stocks – and investors who get in on the action early enough.

Our urgent report, Atomic Opportunity: Nuclear Energy's Comeback, explores the key players and technologies driving this opportunity, including 3 standout stocks poised to benefit the most.

Download Atomic Opportunity: Nuclear Energy's Comeback free today.Advanced Micro Devices, Inc. (AMD) : Free Stock Analysis Report

Seagate Technology Holdings PLC (STX) : Free Stock Analysis Report

Micron Technology, Inc. (MU) : Free Stock Analysis Report

Hewlett Packard Enterprise Company (HPE) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.