News & Insights

During the first quarter, we saw stock markets around the world hit new all-time highs. Today we update how retail traders have tracked the rally, looking at flows based on data from Nasdaq Data Link.

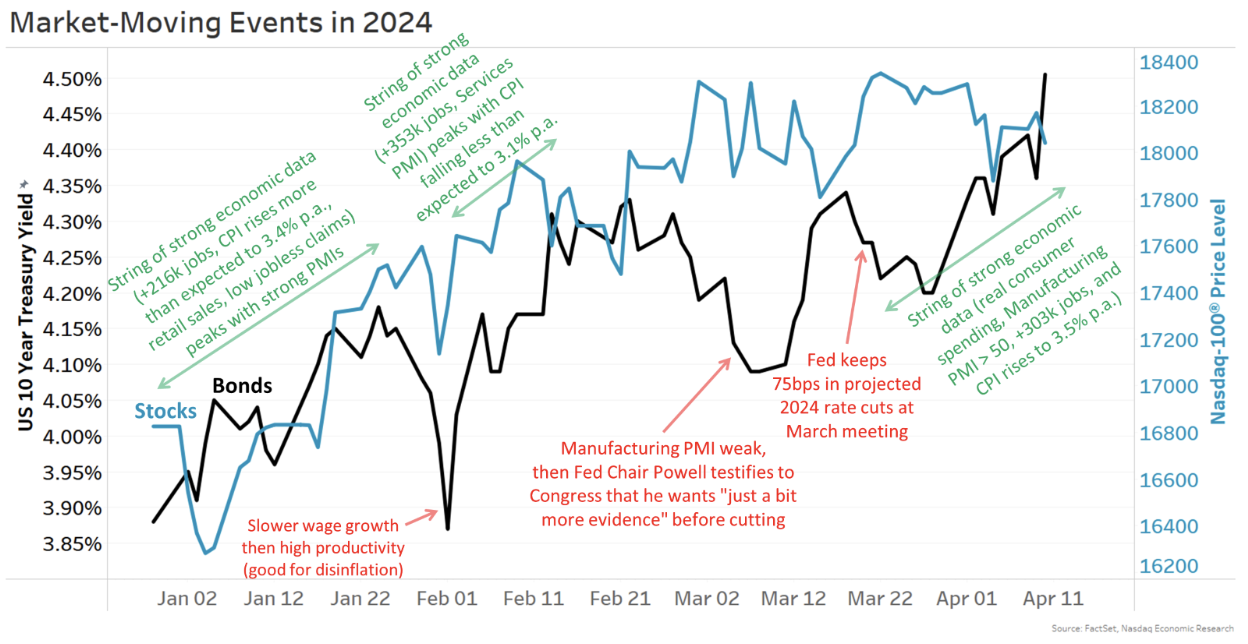

Q1 was a strong month for stocks despite rates rising

In contrast to last year, stocks have rallied despite rates rising.

A string of positive data showed the economy remaining much stronger than expected, seemingly unaffected by the Fed’s higher interest rates. Layoffs and unemployment have remained low, while spending has held up, helping core inflation to track sideways rather than fall.

That economic strength pushed out the expected timing of the Fed’s first rate cut and changed the number of cuts expected in 2024. As a result, longer-term rates have mostly increased this year, from below 3.9% to over 4.4%.

Chart 1: Performance of stocks and 10-year interest rates in Q1 of 2024

Retail buying picked up as market rally extended

In contrast, the rally in 2023 occurred as long-term rates fell, and the general uptrend was interrupted in Q3 of last year when 10-year bond rates climbed toward 5%. The rally then resumed as long-term bond rates fell back to 3.9%, where they started this year.

As the rally extended into 2024, a number of stock markets around the world hit new all-time highs.

The U.S. retail trading data shows that retail investors have been net buyers of stocks in each of the first three months of 2024. In addition, the concentration of buying in Consumer Discretionary (which was mostly Tesla) has broadened now to include other sectors (notably Technology, but also Energy, Healthcare and Financials).

Chart 2: Net retail stock flows by month and sector (line shows SPY price)

Even stronger net buying in ETFs

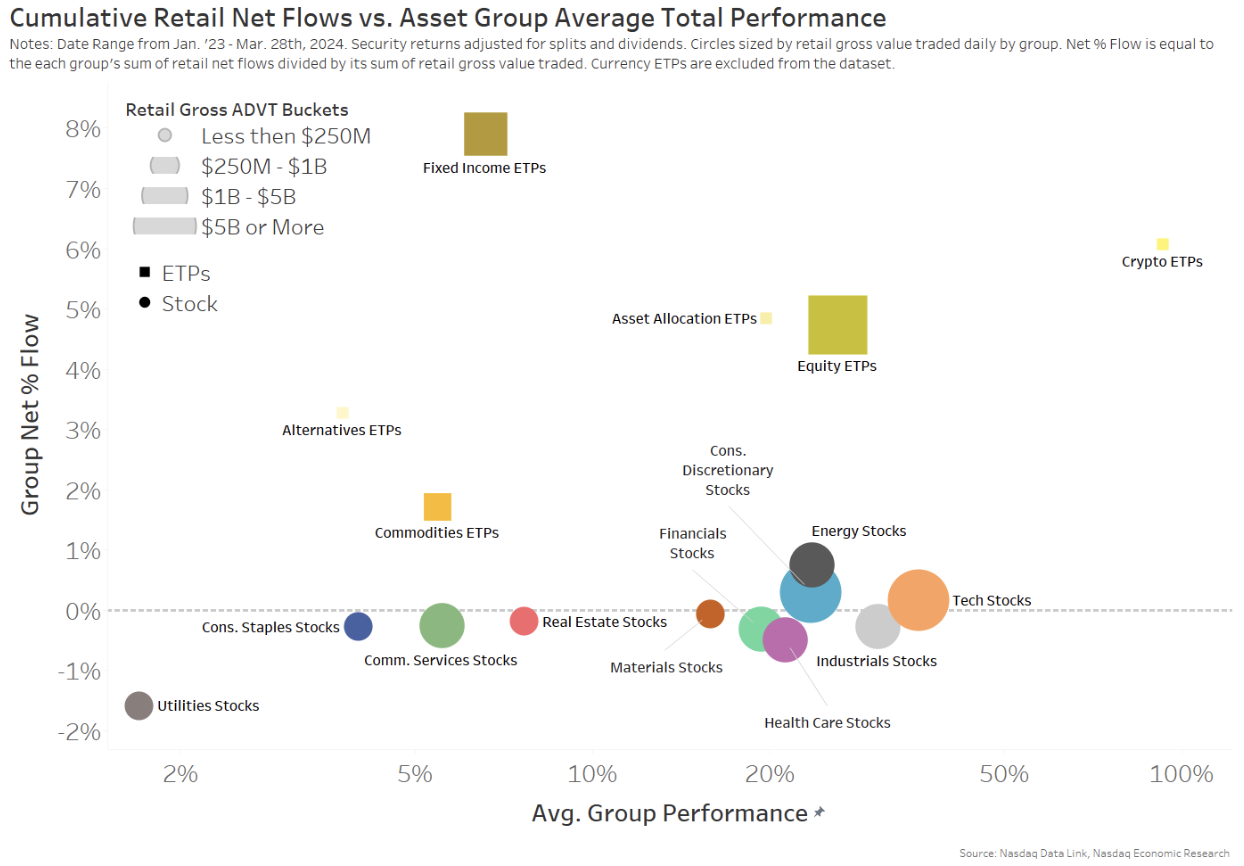

Interestingly, if we look over the whole 15-month period at retail flows (vertical in Chart 3) and returns (horizontal), we see all sectors have had positive returns. Despite that, most sectors have seen small net selling (as a proportion of total trading). However, strong gains in energy, consumer discretionary, and technology stocks were combined with marginal net retail buying.

Chart 3: Past 15 months of returns and net flows across stock sectors and ETF asset classes

In contrast, all categories of ETFs (boxes) have seen much stronger net buying, with the strongest ratio of buying to selling in bond ETFs, as investors look to (finally) capture positive real interest rates.

Interestingly, the newly approved crypto ETFs have also seen a strong net-buy ratio, which came with a rally in the underlying asset class that beat all other sectors and asset classes in this chart.

But retail have net bought ETFs consistently

Another way to look at the stronger net buying of ETFs is to look at daily flows. This shows ETFs rarely see a day of retail selling — while stocks frequently do — despite the generally strong start to 2024.

Chart 4: Net retail buying of ETFs and stocks by day

Gross retail trading picking up

The data also suggests that retail value traded has again picked up, helped in part by higher stock prices:

- Daily retail trading has increased to almost $41 billion per day since the start of Q1, which is close to peak post-Covid levels.

- Market-wide value traded also increased (blue line below) to about $625 billion per day in Q1.

Chart 5: Gross retail trading value remains above pre-covid levels (market-wide trading in blue, right axis)

Retail continues to add liquidity to U.S. markets and assets to U.S. ETFs

Many people expected retail to tire of the stock market as soon as their portfolio saw losses. However, with earnings improving, underlying strength in the economy and rates expected to fall later this year, retail seems to have returned to the market.

They remain a sizable part of the U.S. stock liquidity story and a significant buyer of U.S. stocks across a number of sectors.

Latest articles

This data feed is not available at this time.

Data is currently not available