News & Insights

Professional asset managers – those who manage mutual funds or pension assets – are often known as the “buy-side” because they tend to buy and hold companies for their customers.

Data shows the buy-side makes up the majority of shareholders in most companies. But how much do they actually trade?

The answer might surprise you (it’s a lot less than you might think).

Professionally managed funds account for more than 50% of all shares

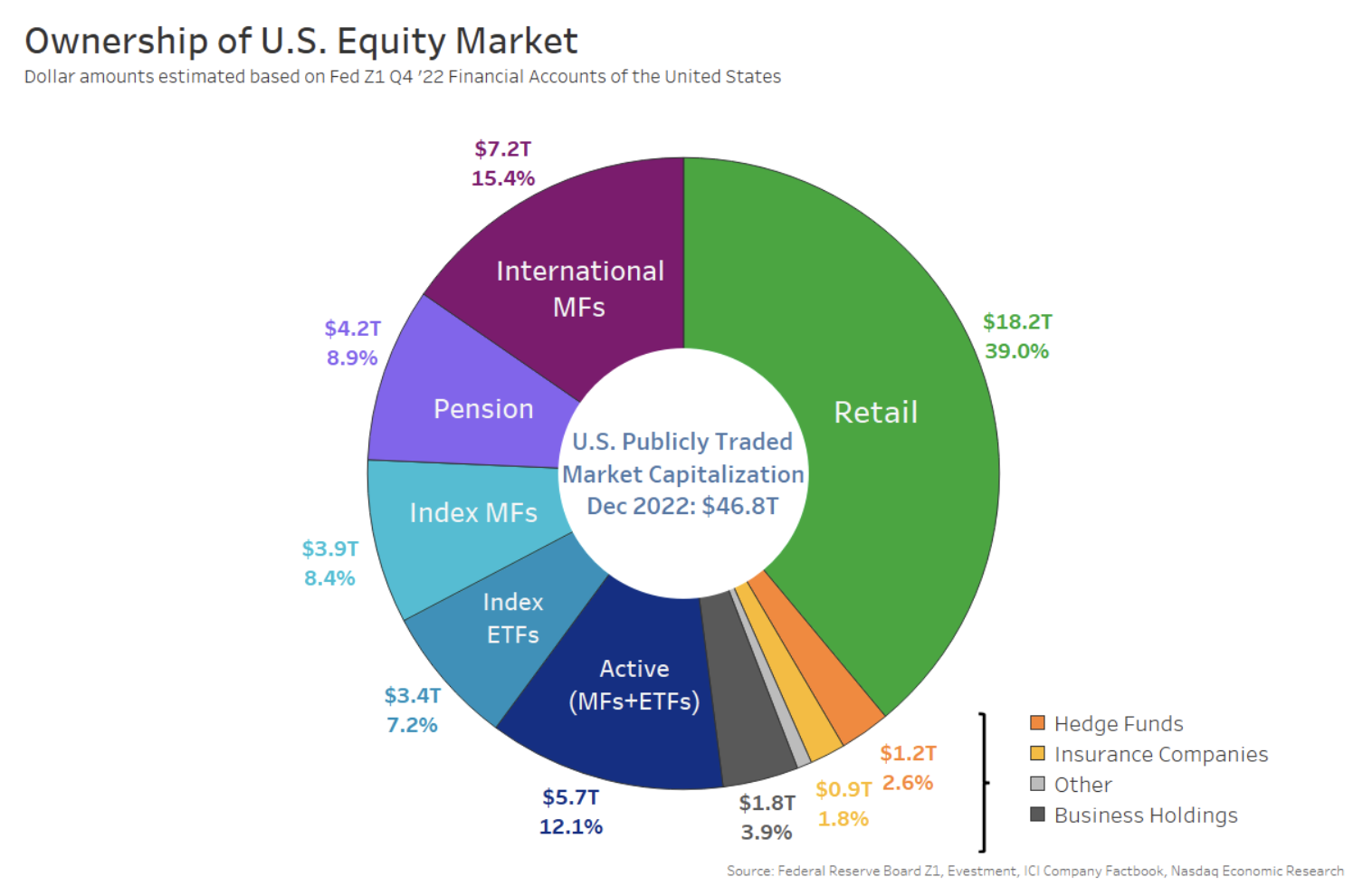

According to Fed data, professionally managed assets (if we include U.S. mutual funds, ETFs, pensions and foreign investors) add to around $24.4 trillion (Chart 1).

That means professional asset managers own over 50% of all shares in most companies, making them an important source of capital for issuers.

Chart 1: The buy-side owns a significant percentage of most companies

Market volumes have increased

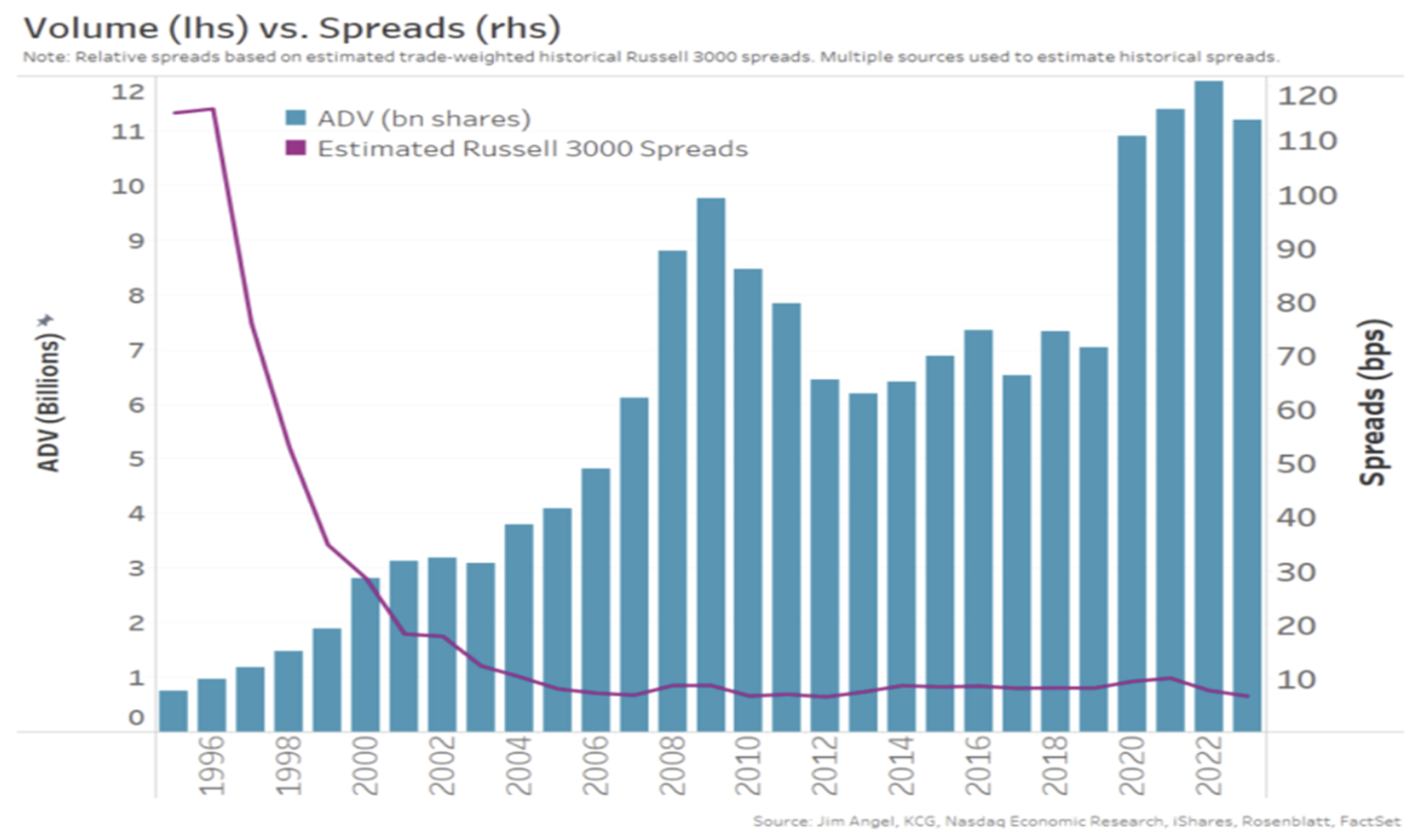

Today, we’ll use a similar approach to that used to estimate who traded U.S. stocks back in 2021 (using 2019 data). Since then, though, some things have changed significantly:

- Average daily volumes (ADV) have increased from around 8 billion shares per day to almost 12 billion shares per day.

- The market has seen increases in retail and options trading (both of which require more market-maker hedging).

- We also see strong ETF trading and even an increase in low-priced stock trading (where a lot of shares might represent a small value of trade).

- We have also seen continued growth of index assets, which directly affects buy-side trading, as we detail below (Chart 5).

Chart 2: Volumes significantly increased after Covid started in 2020

Before we get too far, though, we want to note that in this study:

- We are only looking at trading in corporate (company) stocks, so we exclude ETFs.

- We are looking at value traded (not shares) as that better reflects the actual liquidity in the market.

- Every trade has a buyer and a seller: market-wide trading of companies adds to $386bn each day in 2022, which means total market liquidity (buys + sells) is $772 billion per day.

Index funds’ share of assets has been growing

One thing that has changed significantly over the past few decades is the size of index funds.

Based on data from ICI, the proportion of mutual funds (including ETFs) assets that are indexes has increased from almost zero in the early 1990s to over 50% of all mutual fund assets in 2022 (Chart 5).

We think that trend is likely consistent across pension and international assets, too.

How much do index funds trade?

This is important because index funds trade a lot less than “active” mutual funds.

“Active” funds employ portfolio managers who research stocks. They try to select stocks that will outperform passive funds with similar strategies and objectives, looking at characteristics such as relative value, quality of growth, or price volatility to overweight names that they think will provide superior performance relative to passively selected strategies.

That makes active mutual funds trade more. It also means active funds should contribute to price efficiency by keeping stock prices tied to market fundamentals.

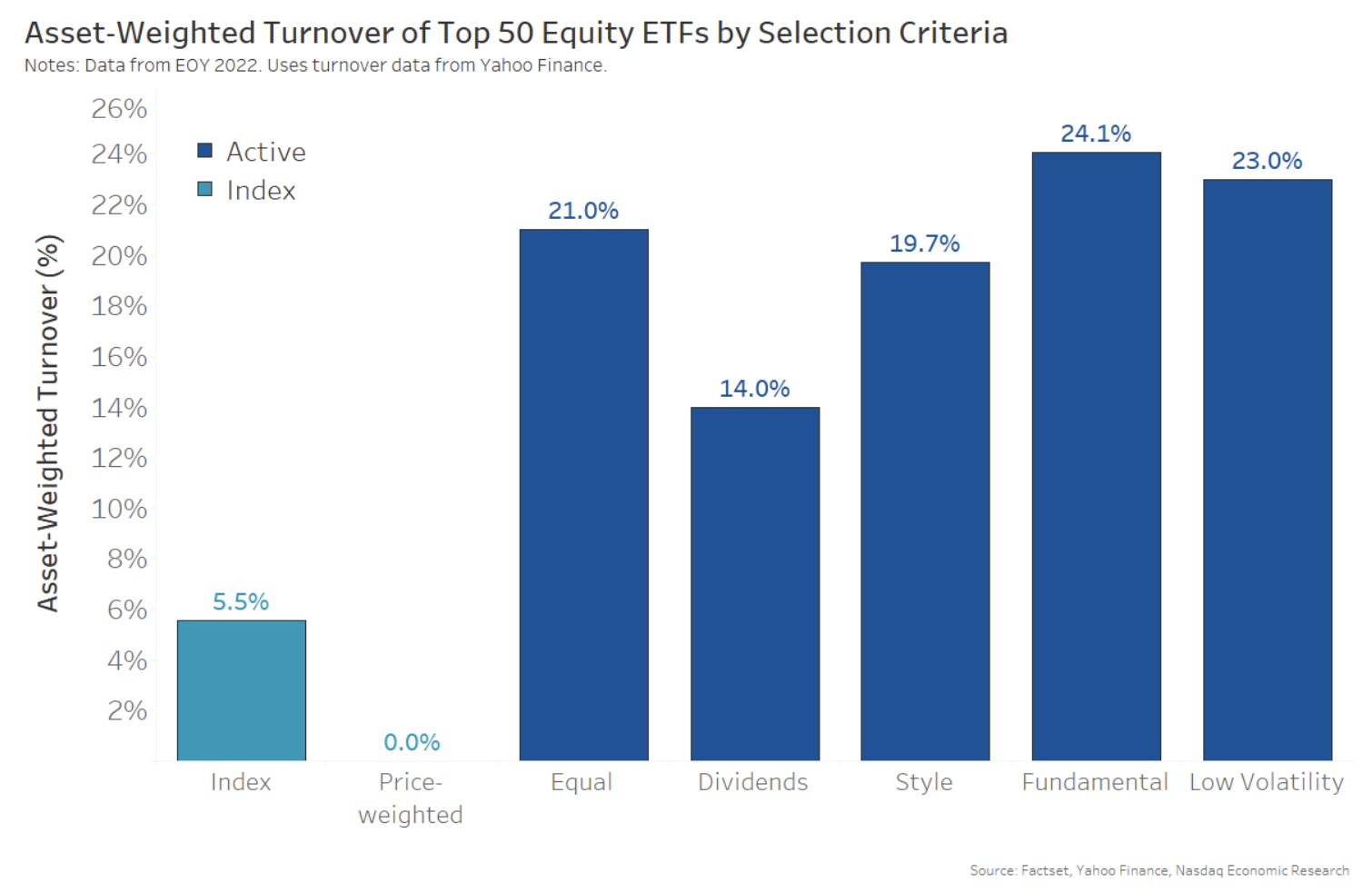

Looking at the asset-weighted turnover of popular ETFs, we see that even style (value or growth indexes) and fundamentally weighted portfolios trade much more than index funds.

Chart 3: Indicative portfolio turnover for typical strategies shows index funds trade very little

In theory, a market cap-weighted index fund shouldn’t need to trade at all. That’s because as a stock's price rises, its weight in the index increases, and its weight in the index fund rises by the same amount. So, no trading is required to continue following index weights.

However, indexes do still change. Stocks need to be added and removed for a variety of reasons – and companies issue and buy back stock constantly – changing their actual market cap, which increases their index weight regardless of stock price.

The data above suggests that index funds’ typical asset-weighted turnover is close to 5%. That’s consistent with index research from Brokers, S&P and Russell.

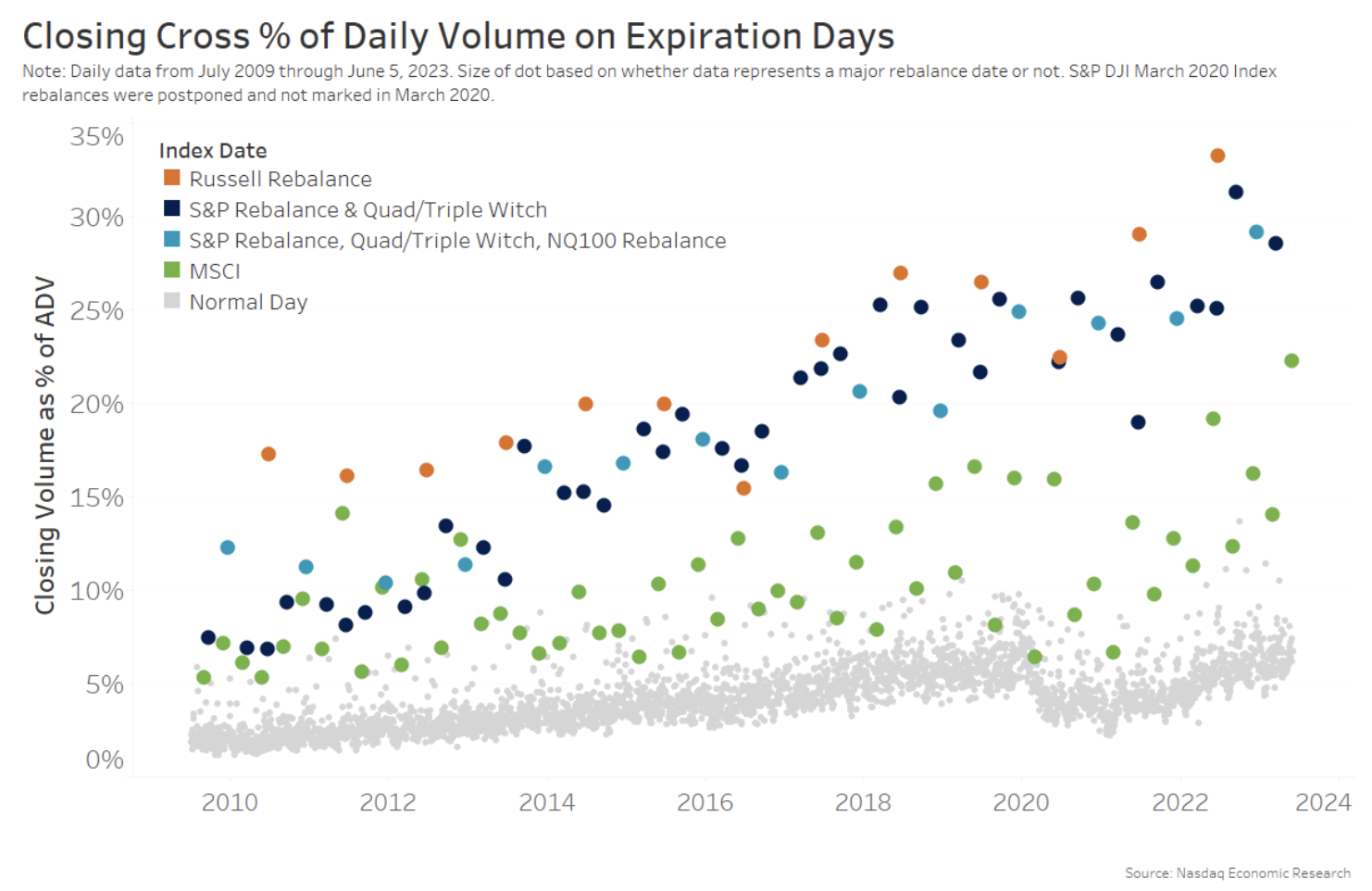

Not only do index funds trade a lot less, but we also see that Index funds tend to concentrate their trading around the close and trade mostly on index rebalance dates (Chart 4).

However, that also makes index funds good shareholders for companies – as they are increasingly large shareholders who tend to buy and hold for a long time.

Chart 4: Market close volumes spike only on index rebalance days

How much do mutual funds trade?

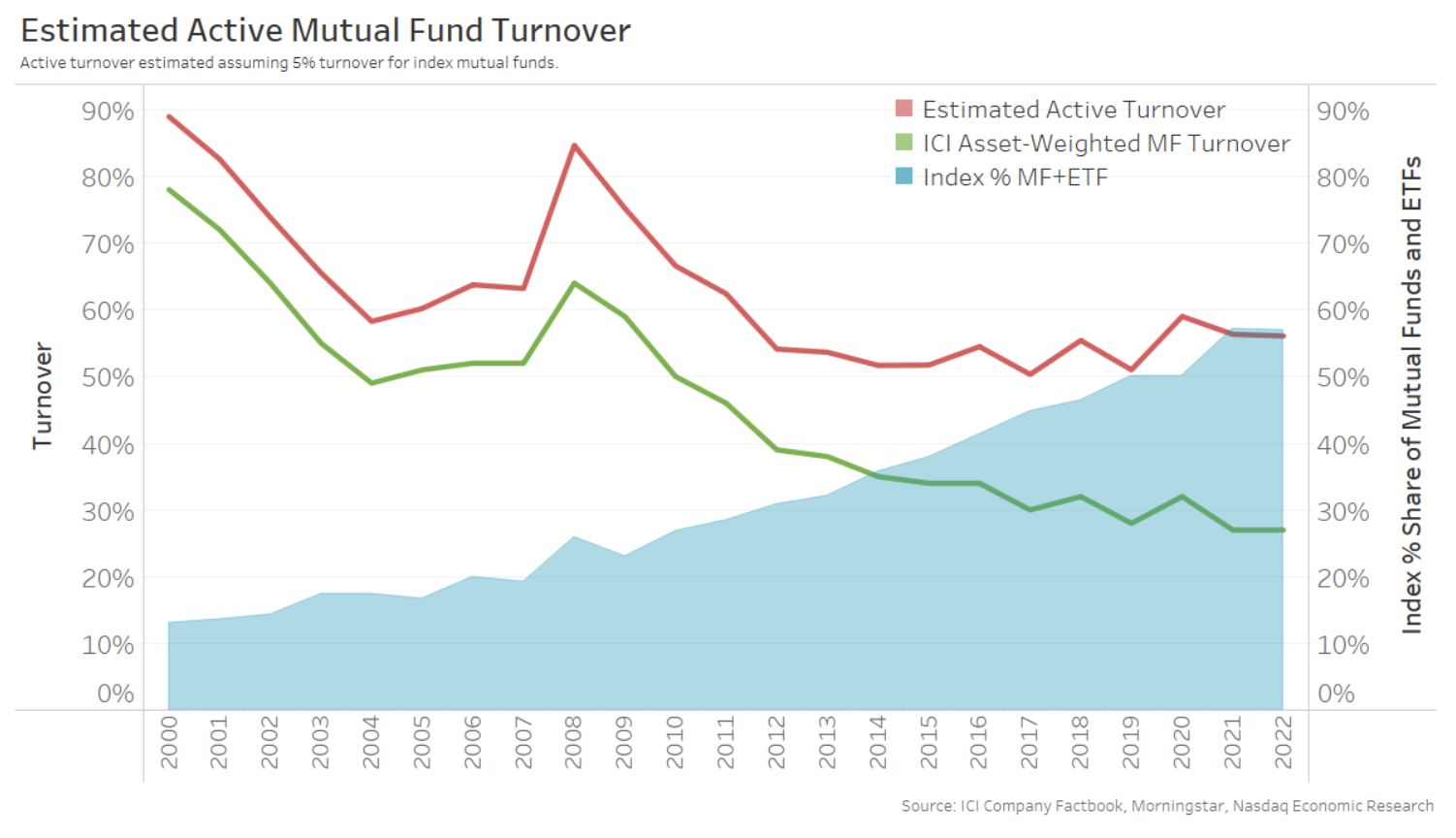

ICI has tracked the average turnover of all mutual funds for years. Their data shows that the average turnover has steadily declined for most of the past 35 years and now sits around 27% per annum (green line on Chart 5).

However, we also know that index funds trade a lot less than that, and the proportion of all funds that are index funds has increased over time (blue area).

We can reverse engineer the turnover rate of active mutual funds based on this data. The result suggests that active funds turnover is closer to 56% and relatively unchanged for more than a decade (red line).

This seems to confirm that the decline in mutual fund trading is mostly due to the rise in index funds.

Chart 5: Mutual fund turnover has declined to around 30%

Turnover excludes cash flows

Mutual funds tend to stay “fully invested,” so their returns don’t fall behind the market. Generally, that means when a portfolio manager wants to buy a new stock, they need to sell something else to pay for the new trade. Turnover metrics capture one side of this trade. However, turnover metrics exclude deposits and withdrawals from the fund. (Technically, ICI measures turnover as the smaller of the buy and sell legs of each trade.)

It’s difficult to find public data on gross cash flows (the sum of flows in and out of mutual funds).

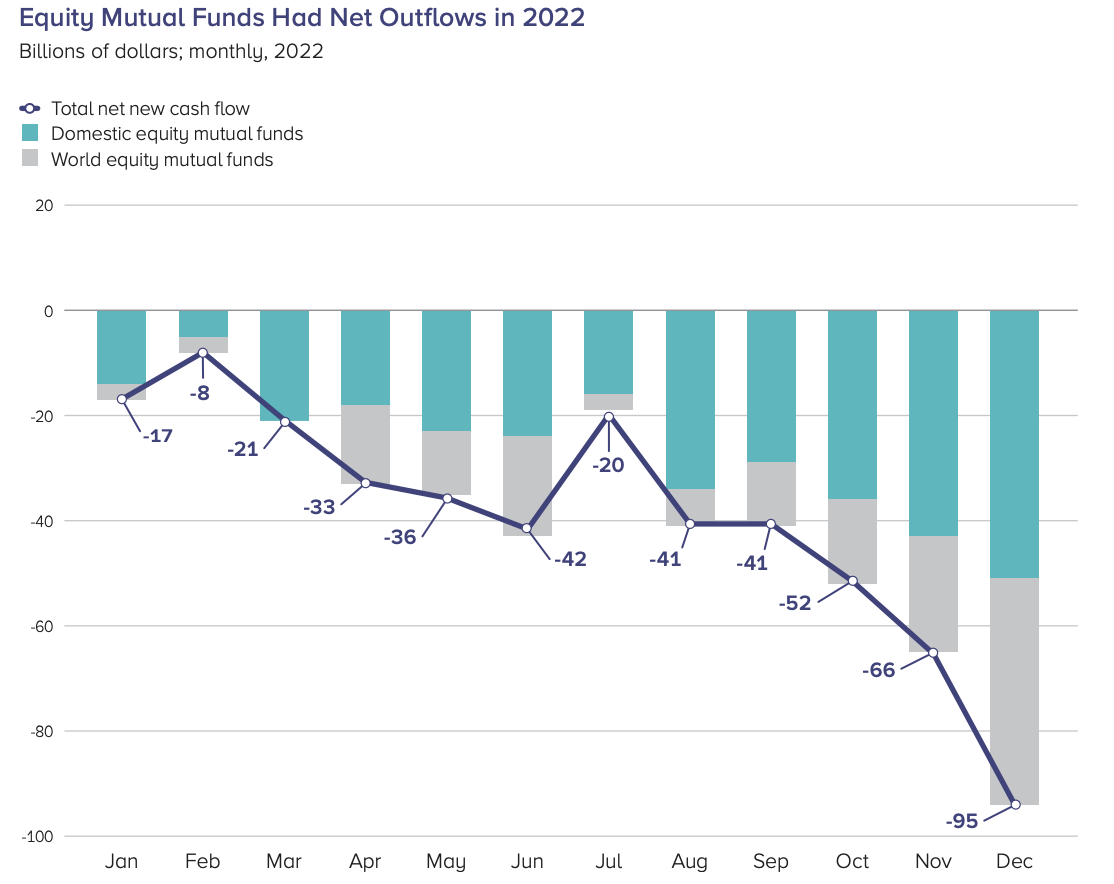

However, there is data on net mutual fund flows. That suggests that active U.S. equity mutual funds saw withdrawals that averaged around $1 billion per day (Chart 6). Similar data suggests inflows into index mutual funds are much smaller, adding to just $140 million each day in 2022.

Chart 6: Net U.S. equity mutual fund flows add to around $1 billion selling each day in 2022

According to ICI, “Index ETFs have seen faster growth — attracting nearly three times the amount of net inflows of index domestic equity mutual funds since 2013.” However, because ETFs grow via creations and redemptions, when the ETF is “rich” versus the underlying stocks, their impact on stock trading occurs via ETF arbitrage. We also suspect ETF arbitrage is mostly done by hedge funds and market makers, but sophisticated retail investors likely participate, too.

Putting this all together

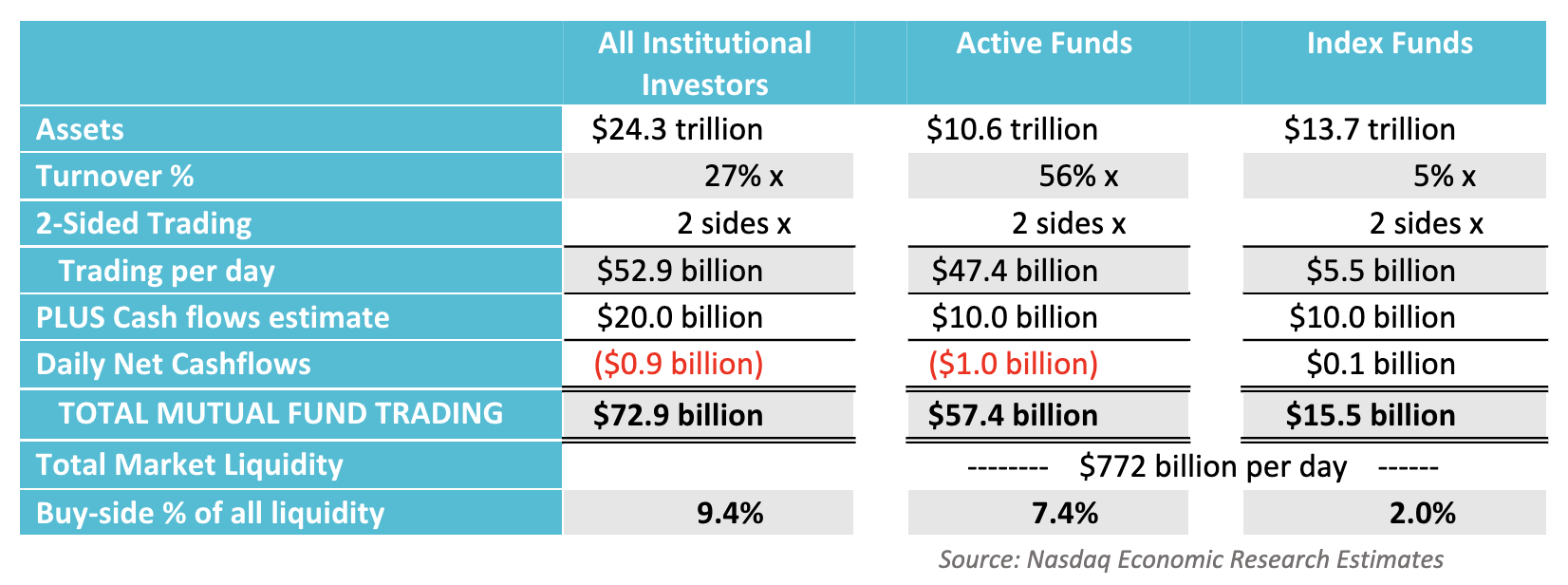

In the table below, we estimate the buy-side adds to less than 10% of all (2-sided) market liquidity.

We show all the math we used to get this result:

- We include all foreign investors in our measure of “buy-side,” which should be conservative (generous to mutual funds).

- Splitting index and active trading and applying the turnover numbers we estimated above, we see that index funds trade just over $5 billion each year to rebalance index weights, while active funds trade closer to $50 billion each year.

- Converting net cash flows of less than $1 billion per day to a gross cash flow number is difficult with available data. However, there are only around 20 days each month, and active mutual funds consistently see monthly outflows in Chart 6 above. We guesstimate daily net cash flow trading at $10 billion per day. That seems conservative - especially considering some cash flows may be invested using futures.

- Because index funds are already 50% of assets and continue to grow, we split gross cash flows equally between index and active mutual funds. We can crosscheck this estimate for reasonableness, knowing that index funds typically trade on close. Total daily cash flows of $10 billion per day equates to about 1.3% of daily liquidity (or 15% of the MOC 2-sided liquidity). That is around the same proportion that MOC trading has increased by in Chart 4 above.

Of course, many of these are guesstimates. If anyone has data that helps achieve a more accurate representation, we would love to see it!

Table 1: Estimates of professional investor trading adds to less than 10% of market liquidity

How much of buy-side trading happens in dark pools?

Interestingly, ATS (dark pool) market share is around 10.6% of all volume. Based on FINRA data, which is available by ticker, we estimate that it adds to trading of around $45 billion (or 12% of value) each day.

To be consistent, that’s (buys + sells) $90 billion of liquidity, which is actually more than our estimate of how much mutual funds trade each day.

However, we think it’s unlikely that all buy-side trading happens in dark pools (ATSs). It’s more likely that:

- Other agency flow is also in ATSs, including some of the more patient hedge fund trading.

- Market makers are on the other side of many ATS trades.

Either way, it’s clear that a lot of buy-side trading happens in dark pools, where counterparties can be segmented, and prices are based on the NBBO and not on the public exchanges where price discovery occurs. However, the buy-side likely does not want to contribute to price discovery while they are entering or exiting their positions, which makes dark pools beneficial for limiting information leakage – potentially decreasing their transaction costs to trade.

Getting the economics right for lit prices is even more important than we thought

We know that the buy side does long-term research and owns the majority of stocks. That makes them really important to price efficiency and capital formation across the whole market.

Despite that, these estimates suggest the buy-side is a surprisingly small part of market liquidity, and especially on-exchange liquidity, than we all think. This data also confirms that:

- Index funds don’t trade much at all and mostly on a few select dates when indexes change.

- Active funds likely contribute more to price efficiency via intermediaries and less to prices on exchange.

That has important implications for thinking about market structure: Who should pay what for spread data, and how does price discovery occur? Retail and buy-side are integral parts of the market ecosystem, and they both benefit a lot from competitive lit prices and tight NBBO spreads, but it also looks like neither group consistently provides information to the market that would improve the NBBO for the majority of stocks.

The very low costs to trade in the U.S., which in turn leads to more attractive valuations for issuers and helps attract more companies to U.S. markets, cannot be taken for granted. Encouraging price discovery and tight spreads is important, especially for the less liquid stocks in the market.

Latest articles

This data feed is not available at this time.

Data is currently not available