News & Insights

We recently talked about how stock market liquidity differs across countries. When converting “liquidity” to a share-turnover-per-year metric, we saw the U.S. isn’t quite as liquid as some think – although it still ranks very high.

Liquidity is important for keeping trading costs low, which helps to reduce the costs of capital for companies. According to Virtu, the U.S. has the lowest trading costs, and based on valuations, it may also have the lowest costs of capital.

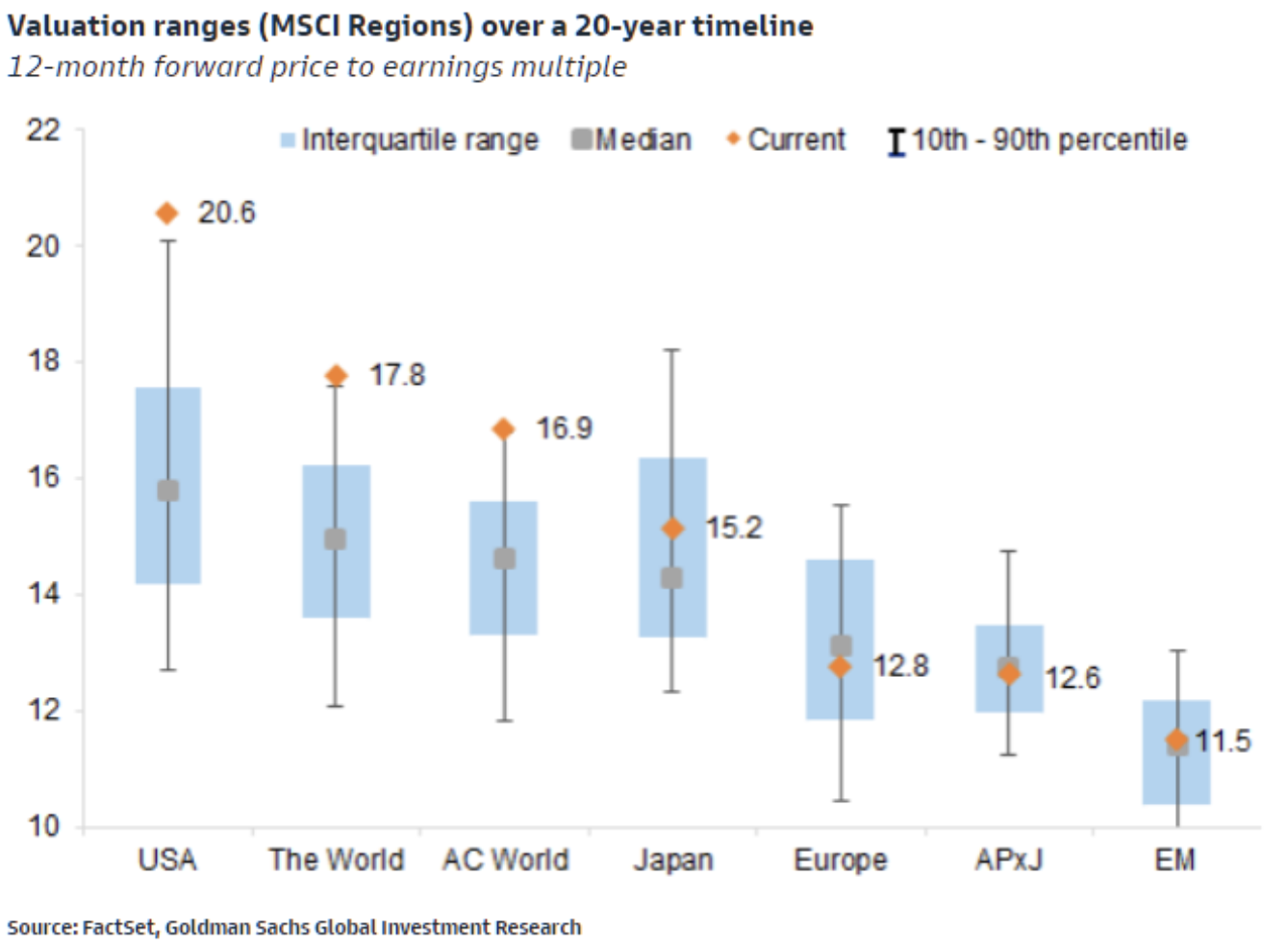

Chart 1: U.S. stocks tend to have the highest valuations, which translates to a lower cost of capital

The U.S. also has a large source of investment capital, with a mature fund (buy-side) industry, retirement plans, and retail investors making up a larger source of investors than many other countries.

All of that makes the U.S. an attractive market for companies to source cheap capital.

However, not all companies want to move their whole listing to the U.S. market. For some, a dual listing or ADR is a more appealing way to gain exposure to U.S. investors and their costs of capital, especially if inclusion in a U.S. index isn’t a concern, as only the Nasdaq-100 includes foreign stocks.

Today, we look at how much liquidity a U.S. dual listing or American Depository Receipts (ADRs) adds to a company’s total turnover. The answer is that a lot of ADRs and dual listings turn out to be surprisingly liquid on their own.

How does U.S. liquidity compare to the world?

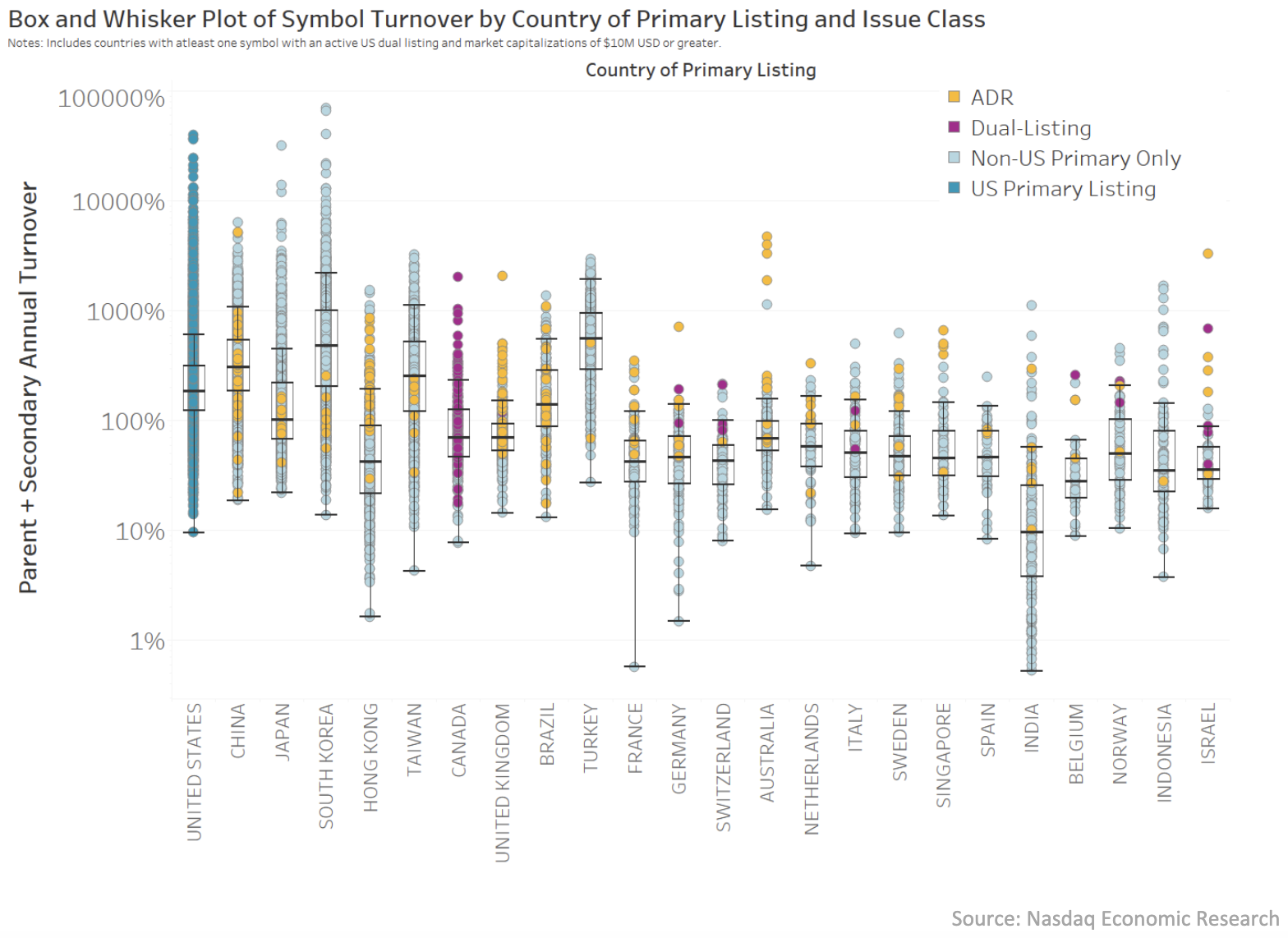

Recall in our earlier study, we showed turnover data by country based on local primary listings (see Chart 4).

In the chart below, we show those same companies without dual listings in blue. We then add the additional incremental turnover of companies with ADRs (yellow) and dual listings (pink) that are traded in the U.S. market. So, in the chart below, we show their combined liquidity in terms of the total shares outstanding in each company and relative to each country’s local market.

The colors show that Canada only has dual listings trading on the U.S. market, while most other countries only have ADRs trading on U.S. markets. A few countries (including Germany, Austria and Israel) have a combination of both.

We also see that for some countries, like the U.K., the stocks that have ADRs typically have relatively high liquidity compared to local-only stocks. In contrast, Japanese stocks that issue ADRs tend to have relatively lower liquidity than local listings that chose not to cross-list on U.S. markets.

Chart 2: Dots show turnover for all companies globally, with those with cross listings into the U.S. colored

How much liquidity does cross listing in the U.S. add?

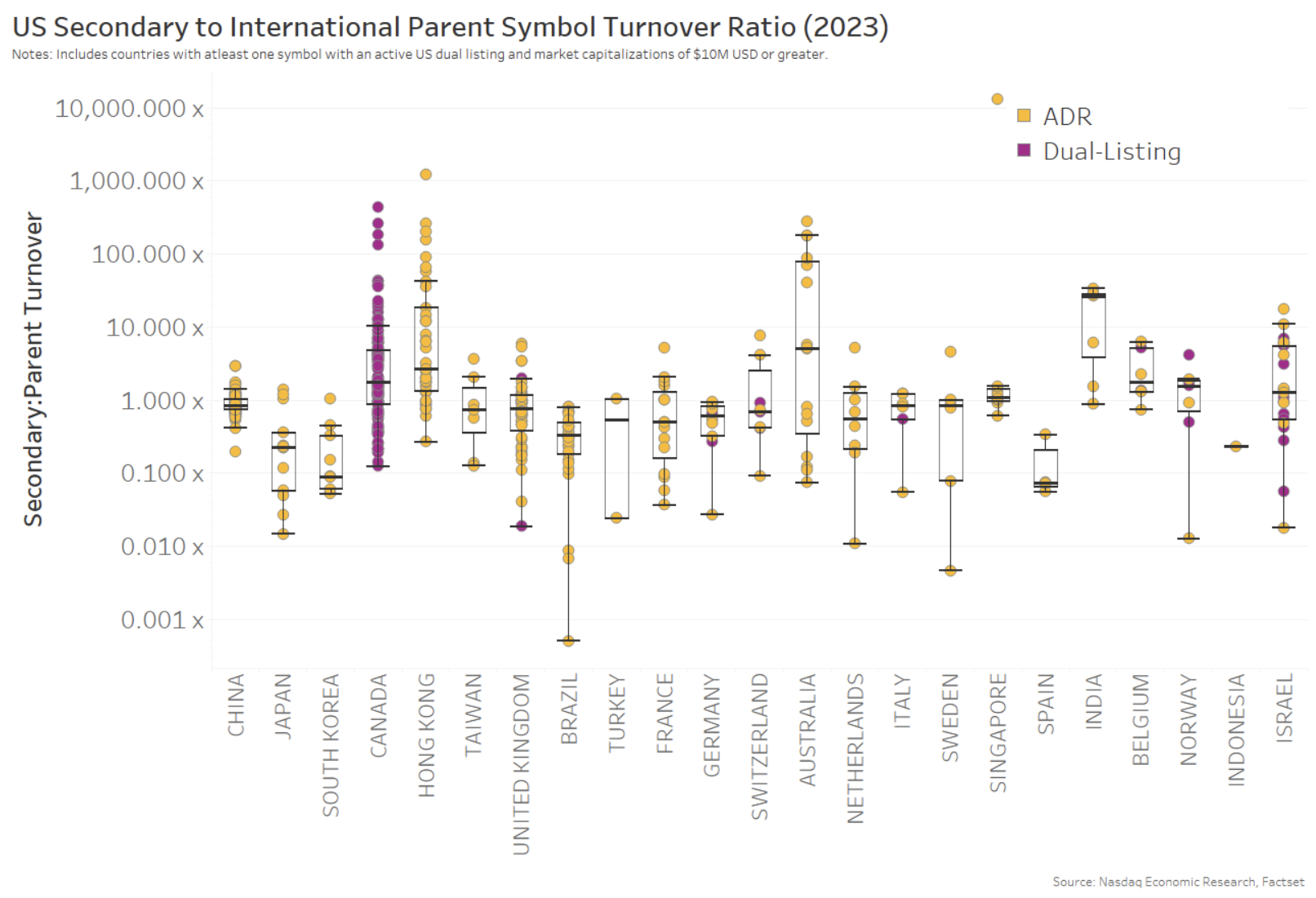

It’s easier to see how much additional liquidity the U.S. listings add by comparing the trading on the U.S. market to the trading on the local (primary) listing.

We do that in the chart below. This also allows us to redraw the box and whisker statistics for just the cross-listed stocks.

We see that cross-listings of stocks from Canada and Hong Kong tend to add multiples to the liquidity of the underlying stock. The wide range of the box around the dots for Australia shows that some Australian companies see a large boost from their U.S. cross listing (relative to their local listing), while others benefit much less.

For a typical company, a U.S. cross listing increases turnover by around 50% – when compared to their primary listing in their local country – although the range of impact is wide.

Chart 3: Ratio cross-listing turnover to primary turnover by cross-listed stock and country

Dual listings add to overall liquidity

The key takeaway from this analysis is that dual listings allow for access to additional investors from the U.S., which may sometimes add to material new liquidity.

That’s potentially helpful for companies looking to broaden their investor base or access cheaper and deeper sources of capital in U.S. markets.

Latest articles

This data feed is not available at this time.

Data is currently not available