Credit: Shutterstock photo

Credit: Shutterstock photoBy iMFdirect :

By Era Dabla-NorrisDivision Chief in the IMF's Fiscal Affairs Department,and Romain Duval,advisor in the IMF's Research Department.

Weak productivity growth in many advanced and emerging market economies in the wake of the global financial crisis is raising concerns about future growth prospects. New research indicates that easing barriers to international trade and foreign direct investment ((FDI)) could boost productivity and output.

Efforts to lower trade barriers have been stalling, but a push toward new agreements promises to reverse the trend. The recent Trans-Pacific Partnership ((TPP)) agreement between the United States, Japan, and 10 other Pacific Rim countries, along with the ongoing negotiations between the U.S. and Europe on the Transatlantic Trade and Investment Partnership (TTIP), place productivity and growth high on policymakers' agendas.

Past multilateral trade liberalization rounds have helped boost productivity, so these recent agreements - albeit not global - could do the same, given their broad geographic coverage, both as a percentage of total world GDP and total world trade. Policymakers, however, need to be mindful of the distributional effects of open trade and take steps to mitigate the impact on those displaced to realize the full potential of lower trade barriers on productivity and economic well-being.

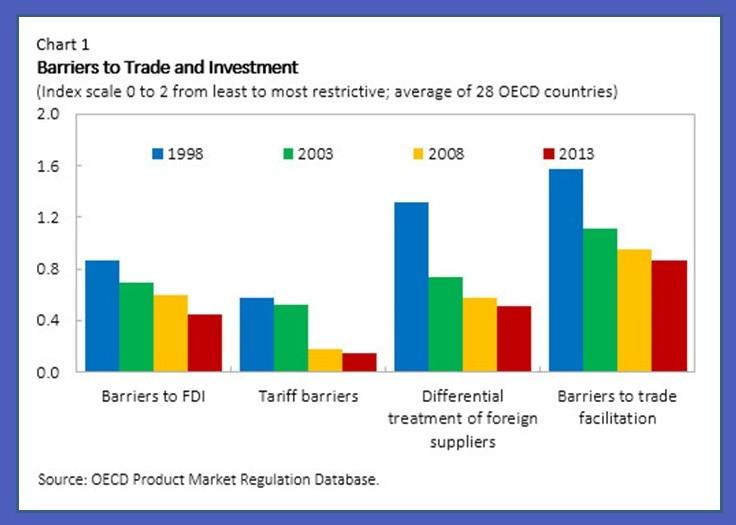

As shown below in Chart 1, even in advanced economies, which have already liberalized tariffs in the past, further reductions in nontariff/regulatory barriers to trade and FDI offer scope for additional productivity gains.

How liberalization of trade and FDI lifts productivity and output

There is wide consensus that liberalization of trade and FDI can lead to improved resource allocation across firms and sectors, boosting productivity and output. For instance, existing evidence suggests that more-productive firms tend to gain market share at the expense of less-productive firms. But two specific effects of liberalization additionally enhance productivity:

- Increased competition - Lower trade and FDI barriers on final goods can strengthen competition in the liberalized sector(s). This can help firms exploit economies of scale, improve efficiency, absorb foreign technology, and innovate.

- Enhanced variety and quality of available inputs - Trade liberalization can also boost productivity by increasing the quality and variety of intermediate inputs used in final goods production.

So which of these two effects is more important?

New research, based on our unique database of effective tariffs in 18 sectors across 18 advanced countries spanning more than two decades, sheds light on this issue. We find that productivity gains arising from tariff cuts on intermediate inputs outweigh the gains arising from cutting "output tariffs," which capture competitive pressures from liberalization in the sector considered. In other words, trade liberalization in upstream industries that use intermediate inputs matters more for sector-level productivity than liberalization in the sector itself. Specifically, a one per cent reduction in input tariffs raises total factor productivity levels by about two percent. The productivity gains from liberalization appear to materialize rather quickly, within 1-5 years, with the estimated impact leveling off over time.

Size of productivity gains

For advanced economies, tariff reductions have clearly been important drivers of productivity growth in the past. For the countries in our sample, input tariffs fell on average by 0.5 percentage point over the decade 1997-2007, which translates into an average productivity gain of about 1 percent.

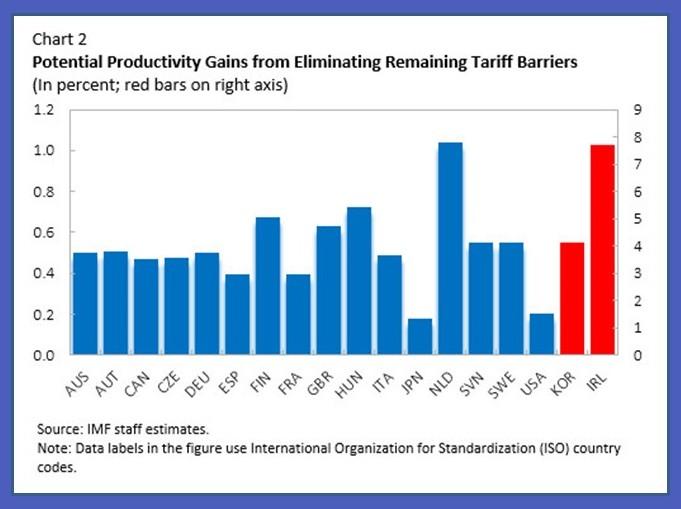

While trade barriers in advanced countries have been reduced substantially over the last two decades, further reduction would lead to additional productivity gains in some sectors in some countries. A simple back-of-the-envelope calculation of the potential gains from total elimination of remaining tariffs indicates that aggregate productivity could rise by around 1 percent, on average, across advanced economies. This varies from a 0.3 percent gain in Japan to a 7 percent gain in Korea. Potential gains for Ireland and Korea are estimated to be larger than for other advanced economies: Korea has higher remaining effective tariffs than other advanced countries in the sample; Ireland's strong reliance on imported inputs, especially in specific sectors, such as chemical and pharmaceutical industries, would drive the potential gains.

The analysis of productivity gains that would follow from tariff liberalization is only an illustration of how trade liberalization, more broadly, could bring about even larger gains in productivity. Indeed, our estimated productivity gains from tariff liberalization should be viewed as lower bounds, because they do not account for the gains that would arise from reallocation of resources across industries, that is, from more efficiently capitalizing on each country's comparative advantage or, most importantly, from a reduction of non-tariff barriers.

Why complementary policies are important

The productivity dividend from the liberalization of tariffs depends, importantly, on complementarities between FDI and trade. In particular, our research suggests that the productivity gains arising from a reduction in both "output" (final goods) tariffs and input tariffs tend to be higher in those countries that have less restrictive FDI regimes. One reason for this result could be that foreign firms use imported inputs more effectively and pay a lower fixed cost for importing: their presence, which benefits from lower barriers to FDI, thus magnifies the productivity impact of tariff liberalization through the input channel.

These results are economically significant. For instance, when the FDI restrictiveness index is at the 75th percentile of its cross-country and cross-sector distribution, the impact of a 1 percentage point drop in input tariffs on total factor productivity ranges from zero to -1 percent, while it ranges from 3 percent to 4 percent when FDI restrictiveness is at the 25th percentile of its distribution.

Policy takeaways

Our findings provide a case for further liberalization to raise productivity and output in advanced economies. That the estimates vastly understate potential gains by overlooking the much larger economic benefits of easing non-tariff barriers makes the case all the stronger. Indeed, recent trade liberalization efforts have increasingly centered on reducing non-tariff barriers, particularly in services sectors, and from expediting customs procedures. Given the emerging and low-income countries' comparatively higher barriers to trade, productivity gains for them could conceivably be even higher.

Reducing barriers to FDI in parallel would amplify the positive impact of lower tariffs and reduced non-tariff barriers on productivity. The productivity gains from trade liberalization may also benefit from reforms in other areas, such as in labor or product markets. For instance, the effect of tariff liberalization could be greater when domestic product market ("behind-the-border barriers") regulations are less stringent. This highlights the need for a broad liberalization agenda cutting across different areas.

Compensating policies for those affected

Trade and FDI liberalization can have costs. While this kind of reallocation of resources between firms and industries is a source of productivity growth, workers in specific locations, industries, or with skill mismatches could face serious costs, including wage cuts and job losses. Increased mobility of capital from FDI liberalization could also lower the bargaining power of less mobile workers. This highlights the importance of supportive labor market policies (e.g., education and training) and other interventions to compensate those that are displaced and achieve a more equitable adjustment. Including labor standards or other labor provisions, as is done increasingly in trade agreements, could help to distribute the benefits more widely.

See also Oil Can't Go Higher on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}