Credit: Shutterstock photo

Credit: Shutterstock photoBy Rakshiet Jain, CFA :

I am not an interest rate strategist or an economist, but I am generally curious about interest rate policy as it has an effect on all asset types, including commercial real estate ((CRE)). The purpose of writing this article is to understand and explain in simple terms the mechanics of how interest rates are set in the current regime and what impact the process is expected to have on CRE asset prices.

There are two big determinants of CRE pricing: net cash flow ((NCF)) and interest rates. In most simple terms, the value of a CRE asset (whether a public REIT or a private asset) is the present value of NCF discounted at a discount rate. The discount rate is the sum of a base rate (which I consider is the then prevailing interest rate on longer duration U.S Treasuries) and a spread that reflects the credit risk of the asset ( Discount Rate = Base Rate + Risk Spread ). The typical reaction to CRE asset prices whenever there is chatter about raising rates is that prices will fall. This reaction is more pronounced in the public REIT markets versus private assets and this creates very attractive opportunities in the public REIT space from time to time and investors should take advantage of the same.

In this article I try to cover the base interest rate aspect of CRE pricing and what it means when the Federal Reserve comes out and says that they will increase rates and/or reduce their balance sheet. In doing so, I do not intend to provide any statistical analysis of the correlation between cap rates and interest rates, but rather use simple examples that are easy to grasp to prove my point.

By no means does this article cover all the nuances of how interest rates are set. I welcome if there are any interest rate strategists on this forum to comment on the below and provide a better understanding.

What Rate Is Set By The Federal Reserve?

Whenever the Federal Reserve comes out and announces that they are increasing or decreasing interest rates, they are talking about the fed funds rate. Per Investopedia , below is the definition of the fed funds rate:

To keep things simple, one should know that this is a short term interest rate, which impacts other short term rates like LIBOR, prime rate etc. The longer term rates like the 10 or 30 year U.S Treasuries have not been that much correlated to the fed funds rates in the recent past, i.e., short term and long term rates have taken different paths.

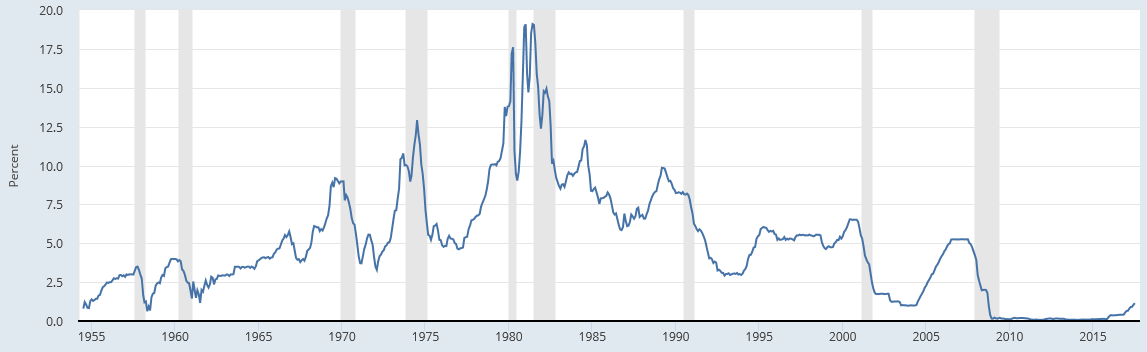

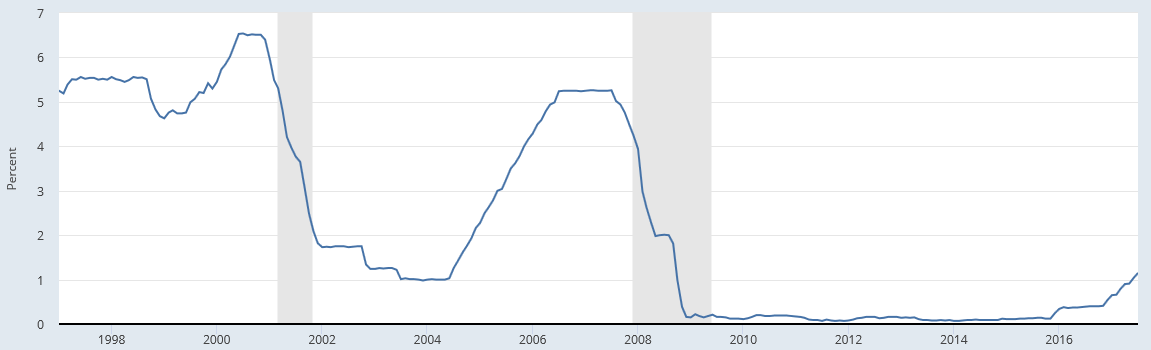

Brief History Of Fed Funds Rate

In response to the global financial crisis ((GFC)), the Federal Reserve cut fed funds rates from about 5.25% in 2006/2007 to 0%. Below is a chart showing the history of the fed funds rate.

Effective Fed Funds Rate History (1954 - 2017)

Effective Fed Funds Rate History (1997 - 2017)

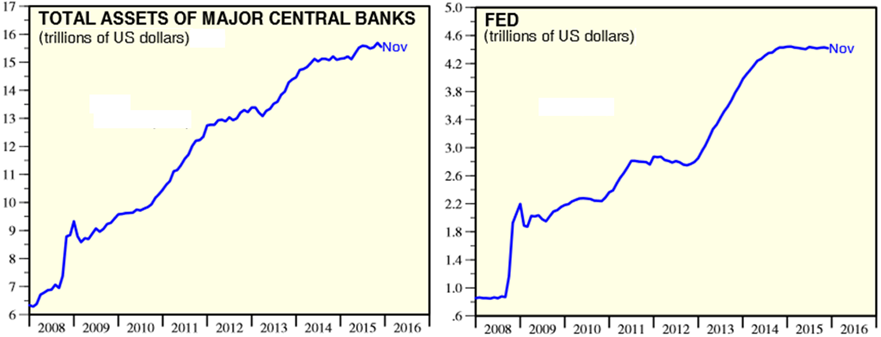

After reducing the fed funds rate to effectively 0%, there was not much room for the Federal Reserve to reduce rates that would stimulate the economy. As a result, they embarked on four rounds of Quantitative Easing ((QE)), where they ended up buying mortgage backed securities ((MBS)) and U.S treasuries. In doing so, the Federal Reserve (and other central banks as well), significantly increased its balance sheet from $0.8 trillion to about $4.4 trillion:

Yardeni Research, Haver Analytics

Below is a current snapshot of the Federal Reserve Balance Sheet:

On Dec 16th, 2015, the Federal Reserve decided to raise the target range for the federal funds rate 1/4 to 1/2 percent OR about 0.25%. The last time the Federal Reserve increased rates was over eight years ago. In addition, more recently the Federal Reserve also said they intend to begin reducing their balance sheet soon.

So what does all this mean?

Dissecting The Jargon

Let me try to explain all this jargon in a little bit more detail (can't promise if I will be successful). The Federal Reserve essentially tries to increase or decrease economic activity by controlling the supply of money, which in turn determines the interest rates. For e.g., if the economy is slow, the Federal Reserve will increase the supply of money, which will lower the cost of money (interest rates), which will spur economic activity as it becomes cheaper to borrow. Conversely, if the economy is too strong (leading to high inflation), it will decrease the supply of money, which will increase the cost of money (or increase interest rates) and cool down economic activity.

The next logical question is how does the Federal Reserve increase or decrease the supply of money? To do so, it must be buying or selling "something" with money. That "something" is MBS and U.S Treasuries and they become the assets of the Federal Reserve. So looking at the above balance sheet, the Federal Reserve has $2.465 trillion of U.S Treasuries and $1.769 trillion of MBS. During the last few years Federal Reserve has been buying Treasuries and MBS and releasing $'s in the system.

So the way I (layman) think about it is say the government is running a $1 trillion deficit. To fund this deficit, the government will have to issue bonds and then "someone" has to buy it. That "someone" is the Federal Reserve (could be other buyers too). I do not want to go in the details of how the Fed buys the treasuries from the government via the banks as I don't think I am qualified enough to explain it. But note two things: first, the Federal Reserve does not create a pile of cash to buy these bonds, but instead a few entries on the liability side of its balance sheet; second, the new money that is created ultimately ends up at one of the depository institutions (like Bank of America ( BAC ), Wells Fargo ( WFC ) or JPMorgan ( JPM ) etc.).

Let me give you an (layman) explanation of the second point on how the new money eventually ends with the banks. Lets say of the $1 trillion deficit that the government is running, $100 billion is marked for some infrastructure projects. The government gets $'s from the Federal Reserve from selling the bonds and the government distributes it to the various contractors responsible for building the projects. The contractor in turn pays the money to its workers, subcontractors, vendors, materials etc. Whoever is getting money for its services or materials, will ultimately deposit that money in a bank. So the more the government runs deficits and the Federal Reserve buys bonds, money starts piling up on the depository banks balance sheet.

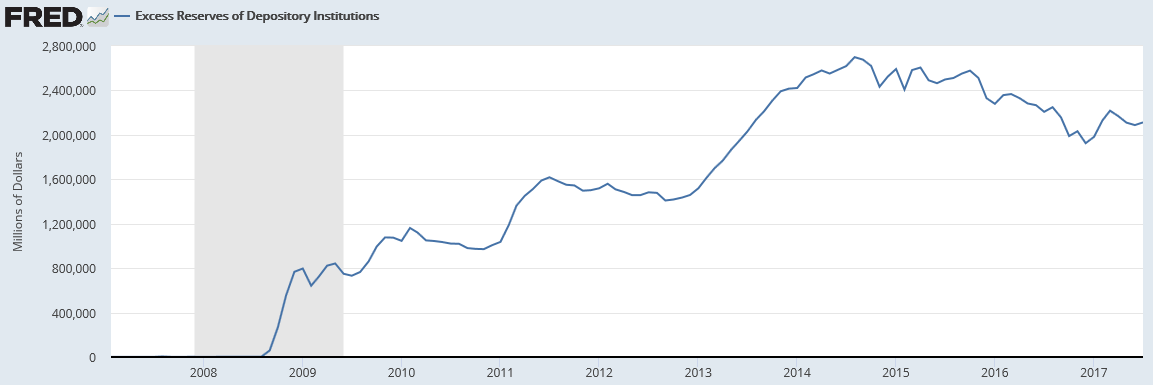

So what do the depository banks do with this excess cash as they cannot instantly find opportunities to lend that money? They park it with the Federal Reserve and earn an interest on it. It creates a liability on the Federal Reserve balance sheet shown as "Other deposits held by depository institutions" above. Depository banks are required to park some cash at the Federal Reserve and that is a reserve requirement. Anything above that is called excess reserves. Due to all the QE, money creation and the mechanisms described above, the excess reserves have really gone up. They reached a peak of $2.7 trillion in April 2014 and are still at an elevated level of $2.1 trillion now (Aug 2017).

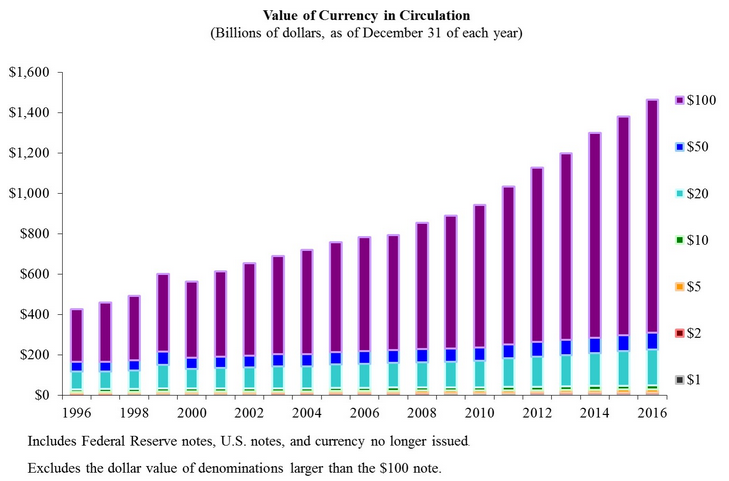

One other line item on the liability side of the Federal Reserve balance sheet is the Federal Reserve notes in circulation. In my (layman's) opinion, they are pretty much created in the same way as described above, just that the Federal Reserve actually prints them and we see and feel them as $1, $5, $10, $100 etc. notes in our wallets. The supply of actual currency has also gone up over time as well, but not as rapidly as the excess reserves.

Below is a time series showing how the excess reserves and currency have grown over time. As it can be seen from below, before the financial crisis, Federal Reserve's assets consisted of primarily treasuries and liabilities was mainly currency. But since the GFC, the asset side now also includes MBS and other assets and the liability side now includes significant excess reserves.

Federal Reserve

Before the beginning of the GFC, the federal funds rate market was small and was governed by one bank's need for cash and other banks need to lend excess cash. This supply and demand of cash would then determine the cost of money, i.e, the fed funds rate. The Federal Reserve would enter this market with funds to balance out the supply and demand of funds and bring the fed funds rate closer to its target fed funds rate. Essentially, if the federal reserve wanted to increase rates, it would sell treasury bonds and take money from banks. This would decrease the supply of money (remove liquidity out of the system), resulting in a decrease in loanable funds, thereby making money more expensive (read higher interest rates). Fed funds rate would then determine a lot of the other ancillary short term rates.

However, this mechanism appears to have broken because all the banks are sitting with excess reserves for which they do not have immediate use, i.e, there is an immense supply of funds (excess reserves). So how does Federal Reserve control the fed funds rate now? There are two mechanisms by which this done. First one is called interest on excess reserves ((IOER)) and the second one is overnight reverse repurchase operation ((RRO)) or reverse repo. Note that the Federal Reserve does a better job explaining these mechanisms and readers can read about it here . I have greatly simplified this to make it easy to understand.

Still Continuing To Explain The Jargon

Let me give an (laymans) explanation of how all this works. The excess reserves are simply a pile of money that banks have. Technically it is just sitting there and not earning anything, i.e., banks have not lent it or invested it. The Federal Reserve comes in and says that they will pay an interest on this pile of money. That is what IOER is. Simple, right? So whenever Federal Reserve comes out and says they are raising fed funds rate by 0.25%, they are paying 0.25% more in interest on excess reserves held by the Federal Reserve. So why would the Federal Reserve do that? The thought is that if the banks are getting paid for this pile of cash, they will have less incentive to lend at a rate lower than IOER, and set a floor for the short term rates.

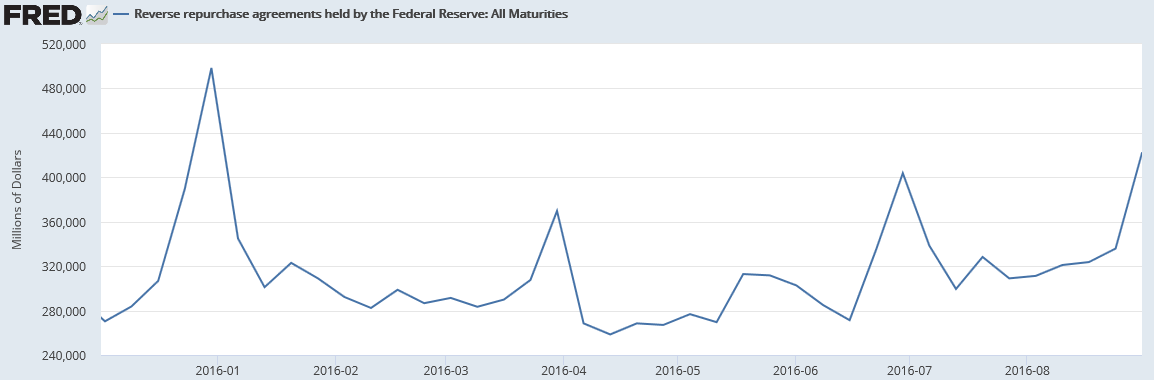

The second one is RRO. What this program does is try to remove liquidity in the system residing outside of the banks. So let's say a big money manager like Fidelity has a money market fund with say $100 and lets say the fed funds rate is 1%. Under the RRO, the Federal Reserve will borrow $100 from Fidelity and pay 1% (annual rate) interest on that money. But Fidelity is smart and would want some type of collateral in return. The Federal Reserve would put the Treasuries it owns as collateral. As the name suggests, the term or length of this lending arrangement is 1 day (overnight). The next day the Federal Reserve returns $100 to Fidelity and pays it 1 day worth of interest. Fidelity returns the Treasuries to Federal Reserve the next day and the whole process starts all over again the next day.

Before the GFC, the liquidity removing actions of the federal reserve would result in permanent removal of money from the system, which created all sorts of problems and deflated a lot of bubbles created due to excess liquidity. But the two mechanisms explained above are not (in my layman's view) true liquidity removing events. Lets discuss that.

First, the excess reserves were just a pile of cash before Federal Reserve started paying IOER, they were just sitting there waiting to be deployed. Point being, they weren't sloshing around in the system trying to find a home. Second, the RRO is just an overnight program. In my example above, Fidelity knows that anytime it needs it's $100, it can get the next day. And it's also not that by increasing the RRO or IOER, the Federal Reserve is attracting or removing more funds from the system. If anything, the excess reserves have fallen down since the Federal Reserve started increasing rates. Also, because banks have so much cash, they probably do not need any more deposits and have not increased the interest they give in the checking accounts of its customers. With respect to RRO, the balances posted under the RRO don't seem to have any correlation with what rate is being offered under the RRO program either (see below, starts from Dec 2015):

So if readers are still reading this article, they must be wondering what is the need for all the gibberish above. Well the answer is, first, to make readers aware what really happens when the next time the Federal Reserve comes out and says that they are going to raise rates. Second, to make readers understand that by merely increasing the fed funds rate, the Federal Reserve is not really removing any liquidity from the system that is likely to have an impact on asset valuations. Third, to also point out that the actions of Federal Reserve have not had much of an impact on the long term rates and in fact they have come down since the Federal Reserve started raising rates.

But what about balance sheet reduction that the Federal Reserve intends to start soon. I think that is the 800 pound gorilla that needs to be taken rather seriously. The way I think about it is that will be a true liquidity removal event where Federal Reserve comes out and starts selling the assets on its balance sheet, i.e., Treasuries and MBS. When it sells these assets, there has to be a corresponding decrease in its liability side to balance it and either the currency in circulation will go down or excess reserves will have to go down. So think about it, if the federal reserve wants to sell $100 worth of Treasuries, it can use the $100 that Fidelity had in the above example. The only difference is that now the Fed is out of the picture. To get its $100 back, Fidelity needs to find another money manager who has $100 and not the Federal Reserve. But what if that money manager has also bought treasuries with its $100 and so and so forth. Suddenly we could find the system has been flooded with Treasuries and less cash. So now to raise cash someone might have to offer the Treasuries at a lower price or higher yield.

Did I just create a scenario where long term interest rates went up?

Hope you get the point, that if the Federal Reserve permanently removes liquidity, it probably leads to higher rates, keeping everything else constant (i.e., assuming there is no outflow of cash from stocks to bonds OR assuming no other foreign buyer steps in to fill the void etc.). I am sure some readers will be quick to point that initially the Federal Reserve will only sell very small quantities of Treasuries and MBS and the market should be able to absorb the same without impacting the long term rates. That may very well be the case, but my goal is to isolate the consequences of Federal Reserve sales of Treasuries and MBS.

What are the repercussions of the actions of the Federal Reserve on CRE asset prices?

So now that I have explained how selling of Treasuries by the Federal Reserve could result in higher rates, lets try to answer the question what impact can it have on CRE prices. The answer is not that straight forward as CRE valuation depends both on NCF and interest rates. So let me give you a few examples to make my point and then I will isolate my analysis towards just interest rates.

Example 1: Let's say you have a 50% occupied office building, generating $2/sf in NOI and say you bought it for $100/sf (2% cap rate). Now let's say a new tenant comes in that increases occupancy to 100%, increases NOI to say $10/sf and it costs the landlord $20/sf in leasing costs. Lets say the interest rates increased such that investors are now going to apply an 8% cap rate vs 7% for this property. So the new value is $125/sf ($10 NOI divided by 8% cap rate), which is still higher than the basis of $120/sf ($100 purchase price plus $20 in leasing costs). Point being, the effect of higher rates was neutralized by improved cash flows.

Example 2: Let's say you have a 100% occupied building by a tenant whose credit rating is CCC and a buyer will pay you a 9% cap rate. Lets say, interest rates sold off and the cap rate is now 10% , but Apple comes and buys that tenant and takes on the lease obligation. In this scenario the perceived credit risk goes down significantly and the property could trade for 6%. Point being, the increase in interest rates was neutralized by the improvement in credit.

Example 3: Let's say you have a 100% leased building, but the tenant's lease expires in 2 years and it is not certain whether the tenant will renew its lease or not. For this profile, a buyer may be willing to pay you a 9% cap rate for taking on this uncertainty. Lets say interest rates went up by 1%, but in this time you were able to renew the tenants lease for another 20 years, thereby removing a huge risk and the property could trade for 6%. Point being, the increase in interest rates was neutralized by the removal of uncertainty.

Example 4: Lets say you have an office building that is 100% leased and if you took it to market, it will trade for around a 7% cap rate. Now assume that rates have actually gone down, where the cap rate is now 6%, but someone built a new building across the street and took 50% of your tenants, leaving the building only 50% leased. In this particular case, the price increase you would have gotten due to cap rate compression has been lost due to the loss in occupancy.

Example 5: This is the last one. Lets say you have a hotel in the middle of nowhere and a buyer will pay you a 9% cap rate to buy this property. Lets say interest rates went up by 1%, but in this time Tesla announced that they will open a new plant next to this hotel. Needless to say any erosion in value due to interest rate will be neutralized by the improvement in location.

The point I am trying to make with all the above examples is that interest rates are not the only determinant of price, there are other factors at play as well. So the next time REITs sell-off due to the specter of interest rate hike, think whether there are other factors at play and take advantage.

Now for another big question: If the NCF stays constant along with everything else staying the same (credit, lease term, location etc.), how do you isolate or explain the effect of interest rates on CRE prices? The answer is "it depends".

Isolating Interest Rate Impact On CRE Pricing

The way I think about it is it depends on what is the IRR you are buying a particular asset at . In the private markets, we define acquisitions in four primary risk buckets: Core, Core +, Value Add and Opportunistic.

As shown above, the four risk buckets have varying degree of risk and get compensated commensurate with the risk. Lets say in the current interest rate environment, core investors are looking for a 7-9% return, core-plus is looking for 9-11%, value add is looking for 11-15% and opportunistic investors are looking for 15% plus returns.

I ran a few scenarios for a hypothetical deal where I assumed an investor was looking to make an 8% and 18% IRR for a core and opportunistic deal respectively. For each of the strategies, I kept the leverage constant at about 65% (which probably is high for core), assumed 100% floating rate debt (which might be not true for core as these are stabilized properties) and kept exit cap rates the same in both cases. I further assumed that the interest rates go up by 0.5% every year and had a 5 year hold.

For the core investment, returns go down by about 2% if rates go up vs. staying constant in the scenario above. So to make the same 8% return, the core investor will ask for a price reduction. One could layer in some cap rate expansion due to rising rates and returns will further come down. Contrast this with the returns for an opportunistic investor who is making an 18% return and if rates go up the same way, he will be making a 16% return, which is still a very attractive return. Do you think he will ask for a price reduction? Probably not as it is still above the 15% return threshold for him. Note that in reality, there are other variables involved and this was just a simplistic example to prove my point

So moving this discussion to the public REIT markets. Whenever there is a serious chatter of rates going up, prices of all REIT's fall sharply. When looking at the price drop, one should keep in mind where a REIT was trading pre rate increase talk, i.e., was it yielding like a core investment or an opportunistic investment and trade accordingly. As an example, if you read my article on Brixmor (BRX; link here ), I am making the case that BRX is trading opportunistically (17%+ returns) at the current prices (of around $19/share) and should not be impacted by interest rate hikes that much. However, about a year ago it was trading at about $29/share, at which price it might have been yielding core or core plus type returns. So at price, BRX would be more sensitive to interest rates than at its current price.

Conclusion

If you have reached this far, thanks for reading. What I tried to accomplish was to give a simplistic overview of how Federal Reserve determines interest rates and how it impacts CRE investors. The current mechanisms used by the Federal Reserve (IOER and RRO) are not true liquidity removal mechanisms in my opinion. If and when Federal Reserve starts reducing its balance sheet, that will be the real game changer.

While investing in CRE assets in the public markets, one should understand at what level of returns (core, value add etc.) are the stocks trading and if assets in all risk categories fall by similar amounts, try to pick the one where the chances of falling further is low .

See also Gold Pulls Back From 2-Month Highs; North Korea Tensions In Focus on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}