Just because a business does not make any money, does not mean that the stock will go down. For example, although software-as-a-service business Salesforce.com lost money for years while it grew recurring revenue, if you held shares since 2005, you'd have done very well indeed. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

So should Jumia Technologies (NYSE:JMIA) shareholders be worried about its cash burn? For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. First, we'll determine its cash runway by comparing its cash burn with its cash reserves.

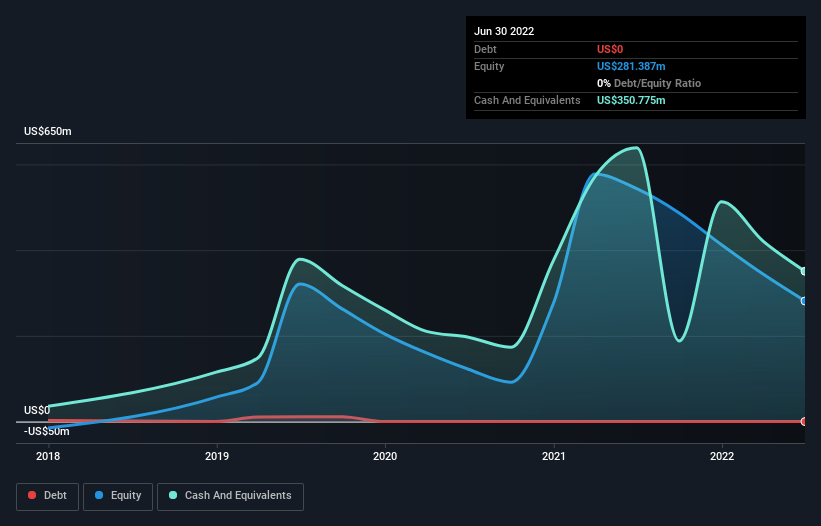

When Might Jumia Technologies Run Out Of Money?

You can calculate a company's cash runway by dividing the amount of cash it has by the rate at which it is spending that cash. When Jumia Technologies last reported its balance sheet in June 2022, it had zero debt and cash worth US$351m. In the last year, its cash burn was US$254m. Therefore, from June 2022 it had roughly 17 months of cash runway. Notably, analysts forecast that Jumia Technologies will break even (at a free cash flow level) in about 4 years. That means unless the company reduces its cash burn quickly, it may well look to raise more cash. The image below shows how its cash balance has been changing over the last few years.

How Well Is Jumia Technologies Growing?

Notably, Jumia Technologies actually ramped up its cash burn very hard and fast in the last year, by 102%, signifying heavy investment in the business. But the silver lining is that operating revenue increased by 25% in that time. In light of the data above, we're fairly sanguine about the business growth trajectory. Clearly, however, the crucial factor is whether the company will grow its business going forward. So you might want to take a peek at how much the company is expected to grow in the next few years.

Can Jumia Technologies Raise More Cash Easily?

Even though it seems like Jumia Technologies is developing its business nicely, we still like to consider how easily it could raise more money to accelerate growth. Companies can raise capital through either debt or equity. Commonly, a business will sell new shares in itself to raise cash and drive growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Since it has a market capitalisation of US$718m, Jumia Technologies' US$254m in cash burn equates to about 35% of its market value. That's not insignificant, and if the company had to sell enough shares to fund another year's growth at the current share price, you'd likely witness fairly costly dilution.

So, Should We Worry About Jumia Technologies' Cash Burn?

Even though its increasing cash burn makes us a little nervous, we are compelled to mention that we thought Jumia Technologies' revenue growth was relatively promising. Shareholders can take heart from the fact that analysts are forecasting it will reach breakeven. Summing up, we think the Jumia Technologies' cash burn is a risk, based on the factors we mentioned in this article. Taking an in-depth view of risks, we've identified 2 warning signs for Jumia Technologies that you should be aware of before investing.

Of course Jumia Technologies may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.