Credit: Shutterstock photo

Credit: Shutterstock photoBy SC Capital Group :

Greystone Logistics ( OTCQB:GLGI ) Writeup

About the Business

Greystone provides the highest quality, lowest cost plastic pallets to the consumer products and retail industries. Unlike competitors, its pallets are made from 100% recycled materials which gives the company a cost advantage and is attractive to environmentally conscious customers. At its manufacturing plant in Bettendorf, IA, the company has twelve Milacron ( MCRN ) injection molding machines with two more on order which each produce 15,000 pallets per month. Greystone will produce over 2.5 million plastic pallets per year once these machines are installed in the next few months. I estimate the company sells its pallets for about $45/pallet.

Industry Background

Retailers and consumer products companies are investing to automate their distribution centers, increasingly choosing plastic pallets over wood because plastic pallets function better in automated facilities, are cheaper to ship because of their lighter weight, are more hygienic with no mold/bugs, and have no nails or splinters which is safer for the products and workers. In addition, Greystone's plastic pallets appeal to environmentally conscious businesses which is a growing trend.

The biggest hurdle to plastic pallet adoption in the past was the higher up-front cost. Historically, a quality plastic pallet cost about $100/unit compared to an A-grade block wood pallet at $25/unit. Greystone's efficient operations enable the company to sell their plastic pallets for about $45/unit which flips the economics over the lifetime of the pallet in favor plastic pallets (lower shipping costs, less product damage, fewer injuries, etc).

Greystone's customer base is almost entirely U.S. customers. Protectionist trade policies enhance Greystone's competitive position because of a reduced threat of imported plastic pallets. The company uses 100% recycled plastic materials sourced from the U.S. Greystone's pallets are primarily used for domestic shipments. International shipments typically use cheap whitewood pallets or lower quality plastic pallets which is a low single-digit portion of Greystone's business.

Customer Adoption

Just three years ago, Greystone had one anchor customer, MillerCoors, that accounted for 60% of its sales. The company has seen rapid adoption of its pallets by major retailers and consumer products companies. The company now has three anchor customers with iGPS, MillerCoors, and Walmart which has diversified its revenue stream and enabled strong sales growth which I expect to continue.

Walmart and Costco, the two biggest physical retailers in the U.S., are two of Greystone's biggest advocates. I think that Walmart recently started buying pallets from Greystone as they invest in next-generation fulfillment centers to more effectively compete with Amazon. iGPS is a pallet pooling company that charges shippers per "pallet issue", collects the empty pallets, and drops them off for the next "pallet issue". Costco prefers that its shippers use iGPS given the advantages of plastic pallets noted above, listing iGPS as the first choice among CHEP, PECO, and whitewood pallet options. Given every major consumer products company sells through these two retailers, I expect plastic pallets will continue to gain share from wood. Plastic pallets have just low single-digit penetration vs the longer-term opportunity to penetrate over 30% of the market, giving a long runway for growth.

Greystone is seeing strong demand for its products with sales +33% y/y in the last year and +77% y/y in the last quarter. The company can barely keep up with orders given the secular trend toward plastic pallets and the large increase in customer adoption in recent years.

Gross Margins

This growth does not come without a price. Greystone's gross margins have fallen in the last 12 months as start-up costs from adding new machines have weighed on margins. I expect two factors will cause margins to improve over the next 12 months. First, the company has more injection molding machines producing pallets, so adding a new machine will have less impact on the overall costs. Second, management has placed orders for equipment to automate labor-intensive parts of the pallet manufacturing process. I estimate this automation investment will only be a few million dollars and has a 12-18 month payback period (66%-100% ROIC), resulting in a boost to gross margins in a few quarters. These two factors should cause gross margins to start improving in the next 12 months and trend toward the company's 18% longer-term average.

Capital Investment to Support Growth

To support the strong demand, Greystone has increased capital investment in new injection molding machines because their current machines are running at full capacity utilization. Greystone has grown from six machines three years ago to twelve machines today. In addition, two more should be installed in the next few months, and I expect the company to continue to add two machines per year. This growth has caused Greystone's debt and capitalized leases to increase from $13mm three years ago to $26mm. However, leverage has remained stable around 3x net debt/EBITDA over the last three years as Greystone generates strong incremental return on invested capital. Importantly, Greystone has financed this growth entirely through borrowing and has not diluted shareholders (shares outstanding have grown at less than a 1% CAGR over the last decade). The management and board are the largest shareholders, so they are well aligned with shareholders to create value.

Unit Economics and Incremental Return on Invested Capital

A new Milacron injection molding machine costs about $2.6mm for the machine ($2.3mm) and molds ($0.3mm). This machine produces 15,000 pallets per month or 180,000 per year. At $45/pallet and 75% revenue capture rate, the machine generates $6.0mm in sales each year. There is little to no incremental SG&A cost to support the machine. Greystone is currently operating with 20% cash gross margins (gross margin plus depreciation % of sales) which means new machines have 20% incremental EBITDA margins even without the margin improvement initiatives mentioned above. At $6.0mm of sales, a new machine will generate $1.2mm of EBITDA or an EBITDA creation multiple of 2.2x vs businesses in the industry worth 8.8x EV/EBITDA (ie capex investments are worth 4x what Greystone spends). I estimate maintenance capex is $0.15mm/year per machine for replacing molds, screws, and barrels every couple years, and to account for the average life of an injection molding machine which is over 20 years. Based on my estimates, unleveraged, pre-tax FCF after maintenance capex is $1.05mm per machine on a $2.6mm investment or a 40% pre-tax return on incremental invested capital. Greystone finances these capital investments with debt that costs 6.5%. This is one of the best carry trades I've seen - borrowing at 6.5% to finance an investment that returns 40% - which is hugely accretive for Greystone's owners.

Greystone's current ROIC is 16.9% vs industry average 12.4%. In addition, I estimate new capital investments are generating returns 40%. I expect that Greystone's ROIC will drift higher toward 20-30% over time. One of the primary drivers of strong stock performance is strong topline growth and improving ROIC. Greystone has both of these factors in spades.

Future Growth Financed from Operating Cash Flow

I estimate that Greystone has reached a scale where growth capex will be fully funded from operating cash flow, debt will stabilize at $25mm, and EBITDA will continue to increase 25-30% each year for the next four years. I forecast Greystone will generate $11mm of EBITDA in the next 12 months, less $1.65mm of interest, less $0.6mm of VIE and preferred payments, less $1.8mm maintenance capex ($0.15mm per machine), and less $1.0mm of cash tax, driving $6.0mm of FCF after maintenance capex. This FCF supports adding 2.3 new injection molding machines per year at a cost of $2.6mm per machine. I expect Greystone will add two machines per year going forward which means growth will be self-financed. I forecast leverage will fall from 2.9x today to 2.3x in 12 months and 1.7x in 24 months vs the industry average 2.7x net debt/EBITDA.

100% Recycled Plastic is a Competitive Advantage

Greystone's plastic pallets are made of 100% recycled plastic. This is an advantage over competitors that use virgin material because Greystone has lower and more stable raw materials costs as recycled plastic prices are less volatile than virgin plastic. Greystone has pelletizing machines at their factory that process and purify scrap plastic into pellets that can be used in the injection molds. In addition, Greystone's "100% recycled" branding helps win environmentally conscious customers.

Greystone offers customers a credit of $10-15 per damaged pallet which reduces the net cost of a new pallet to $30-35/unit. A customer like MillerCoors might have $20mm of pallet credits in their plastic pallet fleet. This recycling credit program makes it very difficult for a competitor to take Greystone's customers because most competitors use virgin materials and typically cannot offer customers a credit for damaged pallets. This creates highly sticky and loyal customers. MillerCoors has been a customer for 20 years. I expect Greystone's newer large customers iGPS and Walmart (and future large customer wins) will remain customers for decades in part because of Greystone's recycling credit program.

Cost Discipline

Greystone's SG&A % of sales is 5.5% vs the industry average 13.2%. In the last 12 months, Greystone grew sales +33%, yet SG&A grew less than 1% resulting in operating leverage. This allows the company to convert gross profits into EBITDA at a much better rate than its larger peers. It's remarkable that a company with 1/80 th of the sales of its larger peers is 2.4x as efficient, as measured by SG&A % of sales.

How does Greystone do it? The company has a culture of cost control with managers who are owners and spend money accordingly. In addition, the company does not have a large sales force. Instead, the CEO does most of the selling and for smaller customers, Greystone takes orders from its distribution partners.

Management Team

Management owns over 50% of the shares, most of which was acquired in the open market over the last decade at prices only slightly below the current price. Management is well-aligned with shareholders and feels an obligation to deliver good returns for its owners. This stewardship mindset is apparent when looking at Greystone's cost discipline, less than 1% annual shareholder dilution over the last decade, and management and board members providing personal guarantees on loans to the company to improve the borrowing cost.

In addition, the CEO and CFO are paid $248k and $138k, respectively, and the board pays themselves just $30k per year. The CEO and chairman, Warren Kruger, personally owns 30% of the common stock, worth over $5 million, and is only paid $278k in compensation for CEO and chairman (18x equity / comp ratio). The management team and board intend to generate their profits alongside shareholders rather than profiting from a large compensation package at the expense of owners.

Customer Mix

Source: Author based on forecasted next 12 months sales mix

iGPS operates in the pallet pooling industry (more details below). I estimate Costco ( COST ) is one of the biggest receivers of iGPS pallets.

MillerCoors is owned by Molson Coors ( TAP ) and has been a customer for 20 years.

Walmart ( WMT ) is the world's largest retailer and I think recently became a customer.

Distributors typically do not carry inventory. Instead, they take orders on behalf of their customers, and Greystone fulfills the order. Sonoco Products ( SON ) is one of many distributors.

Direct sales include all other customers.

Pallet Pooling Industry - Context for iGPS's Business

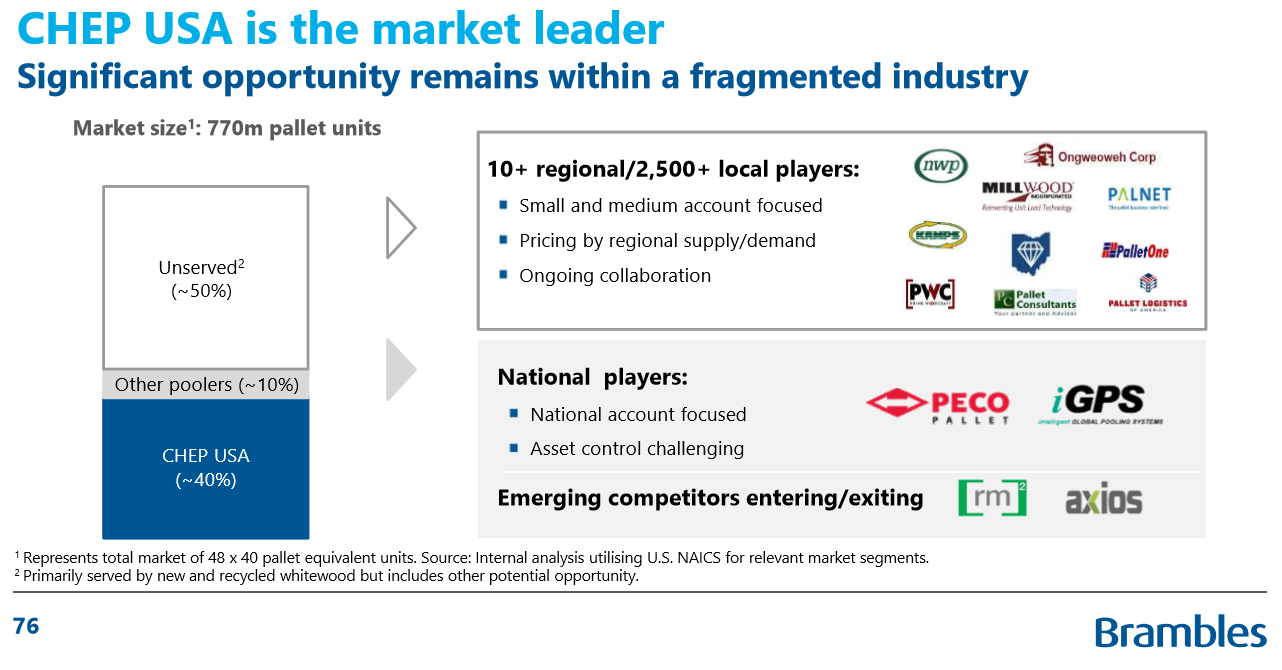

Pallet pooling companies enable shippers to save money on their pallet costs by charging customers about $5 per "pallet issue", rather than paying $25 for a new A-grade block wood pallet that the shipper will likely never recover. There are 770mm "pallet issues" per year in the U.S., half of which are done by the pallet pooling industry. CHEP, a subsidiary of Brambles (BXB AU), is the incumbent pallet pooler with 100mm wood pallets in the U.S. and 300mm "pallet issues" per year, 80% market share of the pallet pooling industry. PECO is the #2 pallet pooler with ~17% market share of the pooled pallet industry and also only offers wood pallets. iGPS is #3 with about a 3% market share and exclusively offers plastic pallets with tracking capabilities. iGPS has been taking market share from the incumbents for the last five years as certain industries such as the beverage industry realize plastic is a better option than wood.

I forecast that iGPS will continue to take market share from wood pallet pooling incumbents and eventually reach over 10% market share of the pooled pallet business (3x its current size). iGPS sole sources their pallets from Greystone. The only way for iGPS to gain market share is to grow their pallet fleet which means more orders for Greystone.

Pallet Pooling Industry Backdrop

Source: Brambles 2018 Investor Day Slides

Plastic Pallet Competitors

Privately-held: Rehrig Pacific, Orbis, Litco International, Shuert Technologies, Sohner Plastics, MDI, and Polymer Solutions International

Public: Buckhorn which is owned by Myers Industries ( MYE )

Greystone vs Packaging Industry

Below, I compare Greystone to other companies in the packaging industry. The company compares favorably versus the packaging industry across quality and valuation metrics.

Quality Metrics:

- Greystone is growing revenue 10x faster than the industry with organic sales growth of +33% vs the industry's +3.5% growth.

- Greystone's 14.9% EBITDA margins are slightly below industry average 15.1% driven by lower gross margins, partially offset by lower SG&A costs.

- Greystone's ROIC is 16.9% vs industry 12.4%. Capex % of sales is 2.8x the industry average, though that is supporting organic sales growth 10x the industry average and is why Greystone's ROIC continues to improve. I estimate that Greystone's maintenance capex is 3% of sales ($0.15mm per machine) roughly in-line with the industry average 2.5% maintenance capex (plus industry spends 2.4% of sales on growth capex for total 4.9%).

- Greystone's leverage is slightly higher than average at 2.9x net debt / EBITDA vs peers 2.7x. I expect leverage to fall below 2x in the next 24 months.

Valuation Metrics:

- Greystone sells for 4.3x EV/EBITDA vs peers 8.8x, 0.7x EV/sales vs peers 1.5x, and 5.7x P/E vs peers 14.7x.

- FCF yield is trickier because Greystone is spending capex to grow 10x the rate of the industry. Once Greystone's growth rate slows, I estimate capital intensity is similar to peers at 2.5% maintenance and 2.5% growth. If Greystone slowed its growth rate to the industry average, I estimate that the business trades at a 24% FCF yield vs peers selling for 5.8% FCF yield.

Source: Bloomberg

Greystone Long-Term Model

I forecast sales growth of +21% from FY18 to FY22, rising to $105mm by FY22, based on injection molding machines added and productivity per machine. I forecast gross margins will stabilize in FY19 and return to 18% by FY22 as new machine startup costs fall and management implements cost-saving automation in its pallet production lines. I forecast EBITDA will grow +28% from FY18 to FY22, rising to over $20mm by FY22. This leads to a +64% EPS CAGR over that horizon to over $0.30/share by FY22. I forecast capital expenditures and FCF based on maintenance capex of $0.15mm per machine plus $2.6mm growth capex per new machine added.

Note: capex includes machines and molds financed with leases.

Source: SEC filings and author's forecasts

Valuation

Greystone is a higher quality business than peers given much stronger organic growth and higher ROIC (and rising) which warrants a premium to peers. However, I am valuing Greystone in-line with peers for the purpose of this analysis. I estimate Greystone is worth $2.30 in 12 months, 300% upside potential, based on EV/EBITDA, EV/sales, P/E, and FCF yield valuation in-line with peer multiples. I estimate fair value rises to $5.50 by FY22, 9x the current stock price, resulting in a +75% CAGR over the next four years.

Source: author's forecasts

Catalysts

- +21% sales growth for the next four years driven by strong customer demand

- Margins expanding from the initiatives mentioned in the article

- These two factors together drive EBITDA growth of +28% for the next four years

- Rising ROIC as incremental capital investments generate >40% ROIC vs current 17% ROIC

- Greystone becoming self-financing which drives leverage to

- Investors realizing the quality of Greystone's business and re-rating the stock to an industry-average (8.8x EV/EBITDA) or better multiple

Risks

- Customer concentration with three customers - iGPS, MillerCoors, and Walmart

- Competitive industry. I think Greystone is the lowest cost and highest quality plastic pallet supplier which is why MillerCoors, Walmart, iGPS, and Costco chose the company's pallets.

- Low gross margin industry that is capital intensive.

- Greystone is a microcap stock that is traded OTC with relatively low liquidity.

Appendix

iGPS

Greystone's largest customer is iGPS. The product is pictured below.

Source: Google images

Source: Google images

Costco's Structural Packaging Specifications - Section 5.0 Pallets is pictured below. It lists iGPS first on the list of choices. Anecdotally, I've heard that Costco prefers plastic pallets because they are safer (no nails in customers' feet) and aesthetics are better.

Walmart

Example of new Walmart distribution centers where Greystone's pallets might be gaining market share.

Walmart Opens New Distribution Center in Mobile, AL

Walmart has 173 distribution centers with plans to open another four. There is a long runway to supply plastic pallets into these facilities given current penetration is low single digits.

Walmart Distribution Center Network USA | MWPVL

Plastic Pallets at a Walmart warehouse

Source: Google images

MillerCoors

Greystone's plastic pallets are pictured below at MillerCoors which is one of Greystone's top three customers

Source: Google images

Greystone's facilities

Milacron injection molding machine and finished pallets ready to be shipped to customers at Greystone's Bettendorf, IA plant

Source: company website

Source: Greystone's 2014 investor presentation

See also IPO Update: Qualtrics Files To Raise $400 Million In IPO on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}