Gold saw incredible price gains in 2024, rising from US$2,000 per ounce to close to US$2,800.

Various factors have lent support, including 75 basis points worth of interest rate cuts from the US Federal Reserve, geopolitical instability in Eastern Europe and the Middle East and uncertainty in global financial markets.

Of course, it wasn't all an upward climb for gold — following the US presidential election, Donald Trump emerged victorious, and the gold price experienced volatility as investors flocked to Bitcoin.

Read on for more on what factors moved the gold price in Q4, followed by a look back at the entire year.

Gold price in Q4

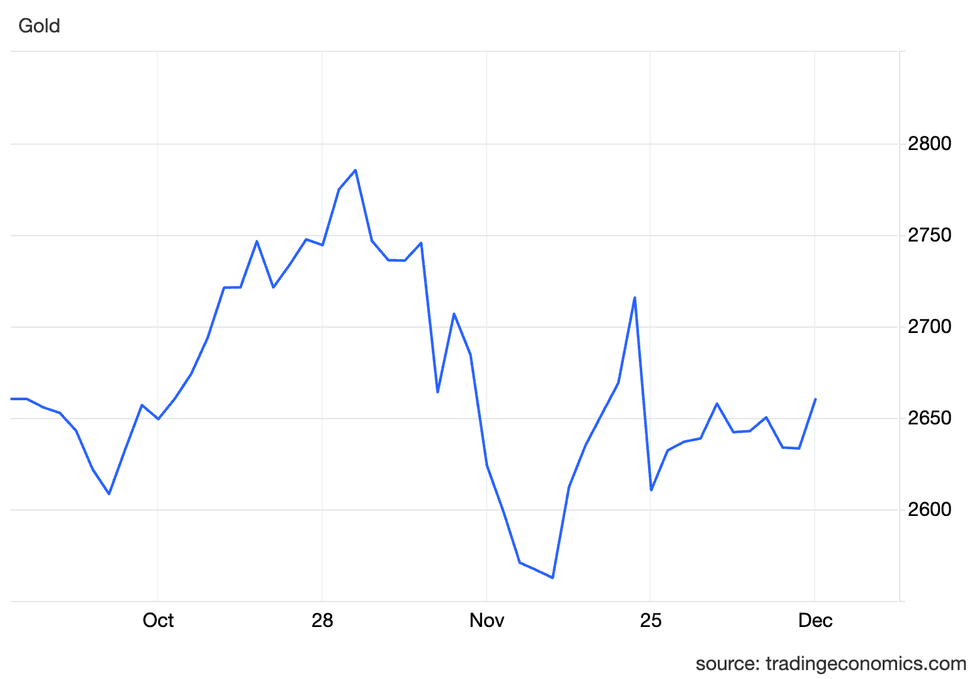

The gold price began Q4 at US$2,660.30, but quickly saw a retraction to US$2,608.40 on October 9. However, the decline didn't last, and gold again rose, setting a new record high of US$2,785.40 on October 30.

The surge upward was fueled by a weaker-than-expected September US consumer price index report, which showed annual inflation of 2.4 percent and monthly inflation of 0.2 percent. These numbers were higher than analysts' forecasts of 2.3 and 0.1 percent, raising expectations that the Fed would cut rates at its November meeting.

Gold was in retreat to start November, dropping to US$2,664 on November 6 after Trump’s victory. The next day, it briefly surged above the US$2,700 mark as the Fed cut interest rates by 25 basis points on November 7.

By November 15, the price of gold had fallen to its quarterly low of US$2,562.50.

The end of the month saw gold leap to US$2,715.80 on November 22. Following this peak, gold entered December below the US$2,700 mark, closing at US$2,660.50 on December 9.

Chart via Trading Economics.

Gold price, Q4 2024.

Geopolitical impacts have been important to gold in Q4.

In addition to Trump's re-election, which has caused turmoil in various forms, on November 17 the US authorized Ukraine to use ATACMS long-range missiles to attack targets deeper into Russian territory. The UK and France mirrored this move, giving Ukraine the green light to use long-range missiles in the ongoing conflict.

Tensions continued to ratchet up in the days following as Russia announced it was lowering the threshold for nuclear retaliation to include conventional attacks from countries backed by nuclear nations. In a demonstration of its capabilities, Russia launched an intermediate-range ballistic missile for the first time on November 21. While the missile appeared only to carry inert warheads, it is capable of delivering both conventional and nuclear armaments.

The threat of a significant escalation has bolstered gold’s appeal as a safe-haven asset and store of value.

How did gold perform for the rest of the year?

Gold price in Q1

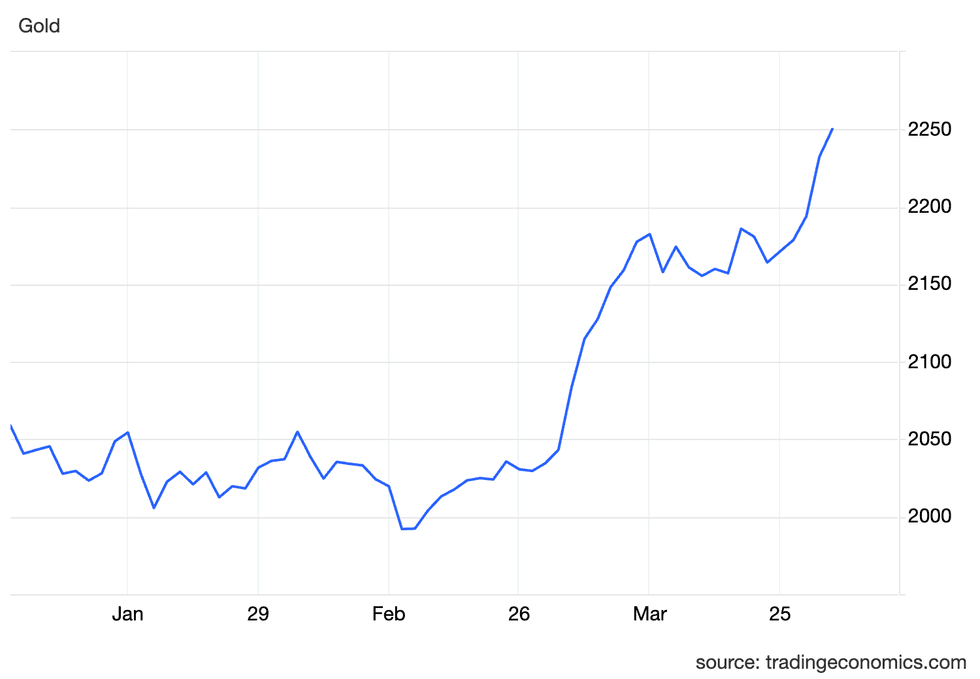

Gold set its first record price of the year at US$2,251.37 on March 31.

Central bank buying, notably China's purchase of 22 metric tons of gold in the first two months of the year, supported the price. Turkey, Kazakhstan and India also significantly increased their holdings at the start of the year.

Further momentum came from Chinese wholesale demand, which jumped to 271 metric tons in January, the strongest ever recorded. Investors were turning to the yellow metal as a defense against falling real estate and stock prices. At that time, the country's stocks had lost nearly US$5 trillion in value over the past three years.

Chart via Trading Economics.

Gold price, Q1 2024.

“As central banks continue to be significant buyers and geopolitical risks and global uncertainties drive investors towards the perceived safety of gold, the current environment underscores gold’s importance as a strategic asset for portfolio diversification and risk mitigation. Therefore, while there may have been a perception of western disinterest in gold, recent developments indicate a sustained and broad-based demand for the precious metal,” Joe Cavatoni, market strategist, Americas, told the Investing News Network (INN) in an email at the time.

Gold price in Q2

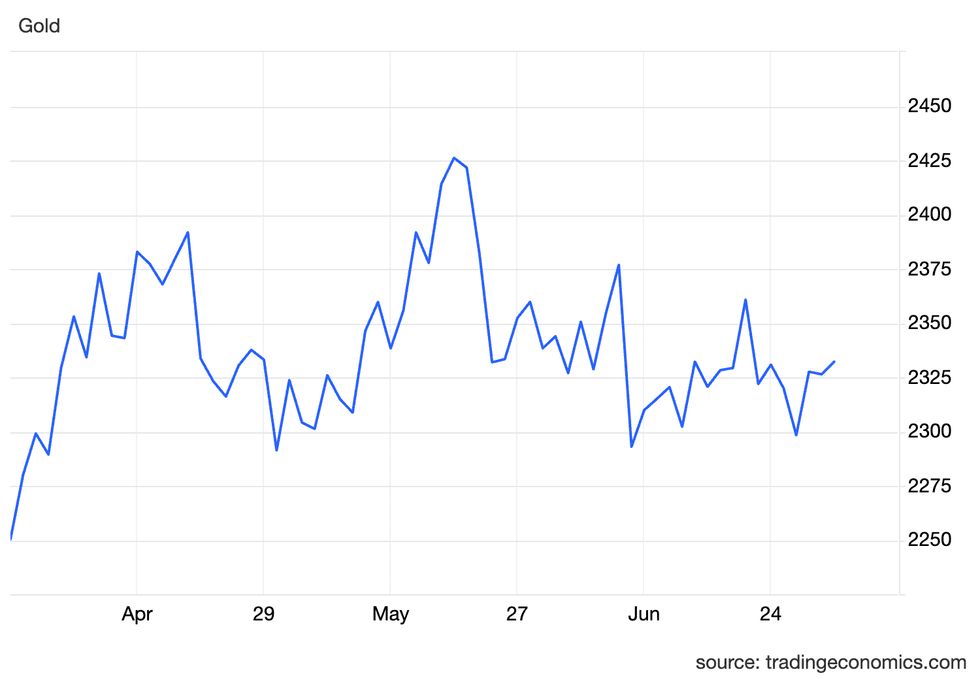

The gold price saw increasing momentum in Q2, setting a new all-time of US$2,450.05 on May 20.

Gains through the quarter were influenced by strong central bank demand. Investor sentiment toward the yellow metal also shifted, with outflows from western exchange-traded funds starting to slow.

Although European funds still saw significant declines, it wasn’t all bad news — the US-based SPDR Gold Shares (NYSE:GLD), the Sprott Physical Gold Trust (NYSE:PHYS), Ireland’s Royal Mint Responsibly Sourced Physical Gold ETC (LSE:RMAU) and Switzerland’s UBS ETF Gold (SWX:AUUSI) all saw increases.

Chart via Trading Economics.

Gold price, Q2 2024.

In a May interview with INN, Jeff Clark, editor of Paydirt Prospector, noted several other market dynamics that caused the price of gold to rise dramatically. He said the real starting point for the precious metal's gains was the end of February, when the Fed indicated it was expecting three or four rate cuts in 2024.

“All of a sudden, gold was off to the races. It jumped so high that suddenly, you had some short covering that needed to happen then as well. So you had short covering, which means they’re buying. And then you had momentum chasers and traders jumping all in. That was a pretty good spike ... that's what kind of started all of this,” he said.

Gold price in Q3

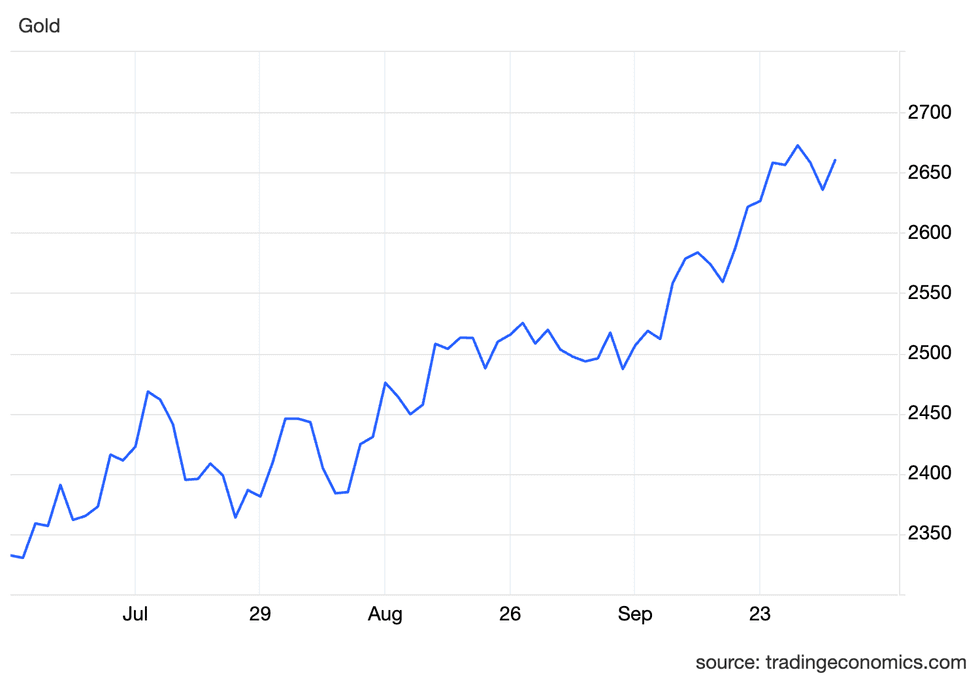

Gold set another record price during the third quarter, reaching US$2,672.51 on September 26.

The high came just a week after the conclusion of the Fed's September meeting, when it announced a jumbo 50 basis point cut to the federal funds rate. While the People’s Bank of China maintained its pause on gold purchases in the third quarter, it granted several regional banks new import quotas in August.

Chart via Trading Economics.

Gold price, Q3 2024.

David Barrett, CEO of the UK division of global brokerage firm EBC Financial Group, suggested at the time that Fed rate cuts were less of a factor for gold than central bank buying. “I still see the global central bank buying as the main driver — as it has been over the last 15 years. This demand removes supply from the market. They are the ultimate buy-and-hold participants and have been buying massive amounts,” he told INN via email.

The quarter also saw significant merger and acquisition activity, with South Africa-based Gold Fields (NYSE:GFI,JSE:GFI) announcing plans to acquire Canada’s Osisko Mining (TSX:OSK) for C$2.16 billion, and South African gold miner AngloGold Ashanti (NYSE:AU) agreeing to purchase UK-based Centamin (TSX:CEE,LSE:CEY) for US$2.5 billion.

Investor takeaway

Overall, uncertainty has been a key driver for gold in 2024.

Central banks have continued to increase their physical holdings against an increasingly polarized political landscape. The most recent data from the World Gold Council shows that they added 186 metric tons of gold to their coffers during the third quarter, with the National Bank of Poland leading the way with 42 metric tons.

The World Gold Council notes that on a rolling four-quarter basis, central bank buying has slowed to 909 metric tons — that's compared to 1,215 metric tons one year ago.

Investors also began returning to the precious metal throughout 2024 as geopolitical tensions and fragile economies pushed them toward gold as a safe haven to help shield their portfolios from volatility.

With the world’s largest economy set to welcome Trump back to the White House in 2025, there are many unknowns. His economic policies could cause inflation to begin creeping up. In contrast, his foreign policies could create new ripples through global trade and financial markets given that he campaigned on more protectionist policies.

Don't forget to follow us @INN_Resource for real-time updates!

Securities Disclosure: I, Dean Belder, hold no direct investment interest in any company mentioned in this article.

Editorial Disclosure: The Investing News Network does not guarantee the accuracy or thoroughness of the information reported in the interviews it conducts. The opinions expressed in these interviews do not reflect the opinions of the Investing News Network and do not constitute investment advice. All readers are encouraged to perform their own due diligence.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.