News & Insights

The U.S. Securities and Exchange Commission (SEC) focuses a lot on some specific words in their mandate – that fees across the market should be fair, equitable and not unfairly discriminatory and not impose undue burdens on competition.

Many seem to think the easiest way to be equitable and non-discriminatory is to make fees equal. But even that’s not so easy and can create distortions, perverse incentives and (ironically) an unfair playing field, as we show today.

Equitable is different from equal

Although these words sound similar, they are actually different enough:

- Equal means each individual or group of people gets the exact same.

- Equitable recognizes that each person has different circumstances and allocates the exact resources and opportunities needed to reach a fair outcome.

But looking at some fees that already exist in the U.S., before we consider what is fair, we need to ask what kind of equal do you mean.

What sort of equal do you want?

There are already four different fees charged to participants that could be considered “equal,” and yet they add to very different costs for each participant.

Clearly, equal is not fair (or equitable) in these cases.

The SEC has approved four different “equal” fees:

1. SIP fees charged to retail

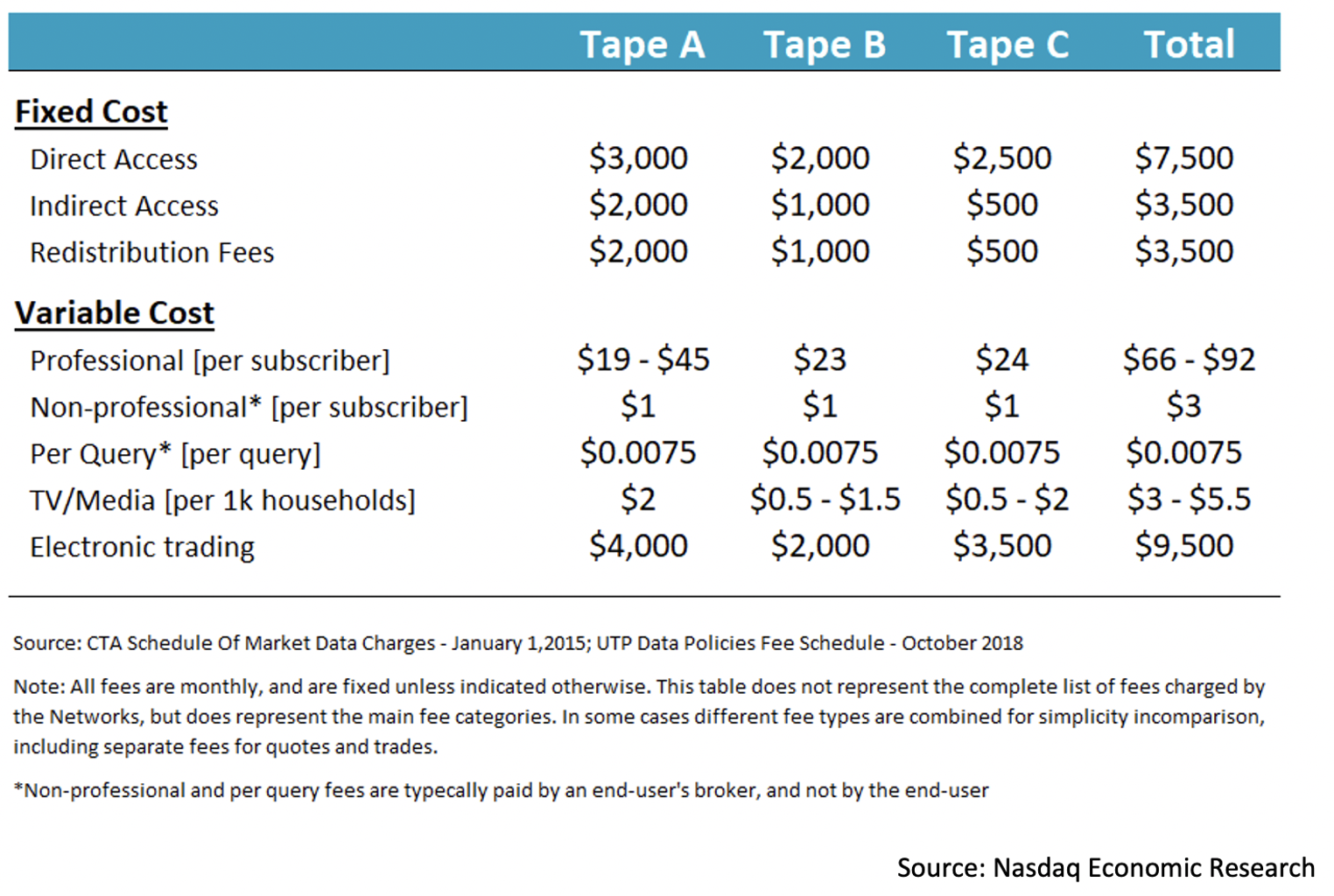

Admittedly, the full SIP rates sheet is tiered based on usage (Chart 1). Retail gets the same data cheaper than professionals, who get data cheaper than algorithmic traders. However, to many users, that makes sense – retail does a lot less trading and makes less money trading than professionals do – while algorithms do a lot more trading and can earn larger profits or commissions than professionals can.

Chart 1: SIP rates sheet costs actually vary by type of participant and level of activity

Focusing on the (non-professional) fees charged to retail traders using the SIP, there is a fixed “base rate” of $0.0075 per “view” of the NBBO. For simplicity in the charts below, we assume that each retail trader views the NBBO only once per trade. Although it’s possible that some request quotes many times before each trade or as they modify working limit orders.

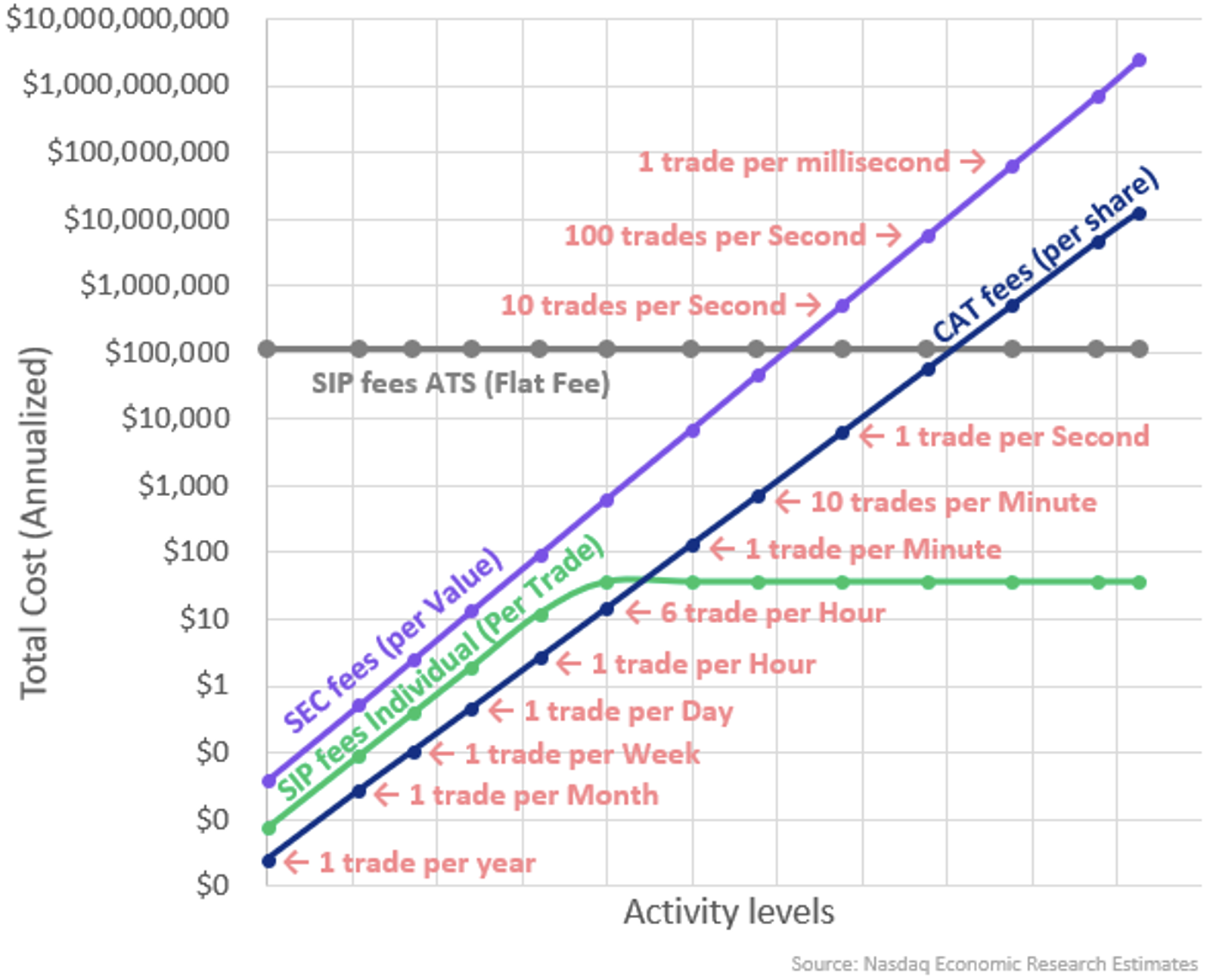

We also show (in Chart 2) that this per query rate caps at $3 per month, which helps a person making a lot of trades, like more than 400 trades per month, although they still pay more than other less active traders.

2. SIP fees charged to brokers

The SIP also has a completely different equal fee for brokers. For a fixed fee of $114,000 per year, most electronic traders (algo, dark pool or wholesaler) can consume the whole SIP all day, every day.

3. SEC fees

The SEC’s budget is also funded by an equal fee, which charges sellers a fixed fee of around 0.002% on each dollar traded.

SEC fees are also proof of how silly constant marginal, cost-based pricing is in our industry. That’s because each year, fees are set at around 0.0002% of all value sold, but as the year goes on, volumes change. The SEC almost always needs to change the fees (sometimes increasing as much as 800% in a low-volume year or decreasing 75% in high-volume years) to actually cover expenses.

4. New CAT fees

The SEC recently approved CAT fees for the industry. They are to be shared — in equal thirds between buyer, seller and venue — and equally between options and stocks based on underlying shares traded.

Many other options were discussed (including equal message-based charges) and discarded. As comment letters showed, someone always felt each version of equal was unfair. Some still think that.

Each equal is different

As the chart shows, none of these “equal” fees work the same.

In general, Chart 2 shows that total costs generally increase as activity rises. While chart 3 shows the “cost per value traded” is consistent across the board.

However, because the basis for what is “equal” changes – from trades to shares to value – and retail investors trade differently to institutional investors – even the average costs to trade aren’t the same for all investors (the lines in chart 2 are not parallel).

For example, retail tends to trade more in small-cap, low-priced stocks. That means their:

- Trade values are small, which reduces the relative impact of SEC fees on the left of the chart.

- Shares per trade are relatively high, which increases the impact of CAT fees (which will be mostly paid by wholesalers who facilitate retail trades).

Chart 2: Four different “equal” fees currently charged add to very different costs per participant

Retail is on the bottom left of the charts

Based on research we have done, we know that most retail investors trade relatively little. For many brokers, their typical retail client trades around 12 times a year (one trade per month). For them, total costs generally add to less than $1/year, with many fees absorbed by their brokers.

Even the more active retail traders, trading every day, likely incur just over $10 per year in costs (most of which are SEC fees).

However, if we review Chart 10 in this study, we see that there are a lot of self-directed retail traders. And we know that as a group, they add a material proportion of market liquidity to the market. However, we also know that most of their trades are executed off-exchange. So, in reality, retail benefits from the NBBO usually without helping to set it.

Professionals who trade a lot are on the top right of the charts

In general, a more concentrated group of participants who trade a lot pay much larger fees for participating in the same market.

However, that’s fair when you consider that those participants (who trade every second or more) are clearly professionals. Data shows they earn trading profits or commissions from participating in the market, which adds up to billions of dollars every year.

The most equal costs aren’t equal at all

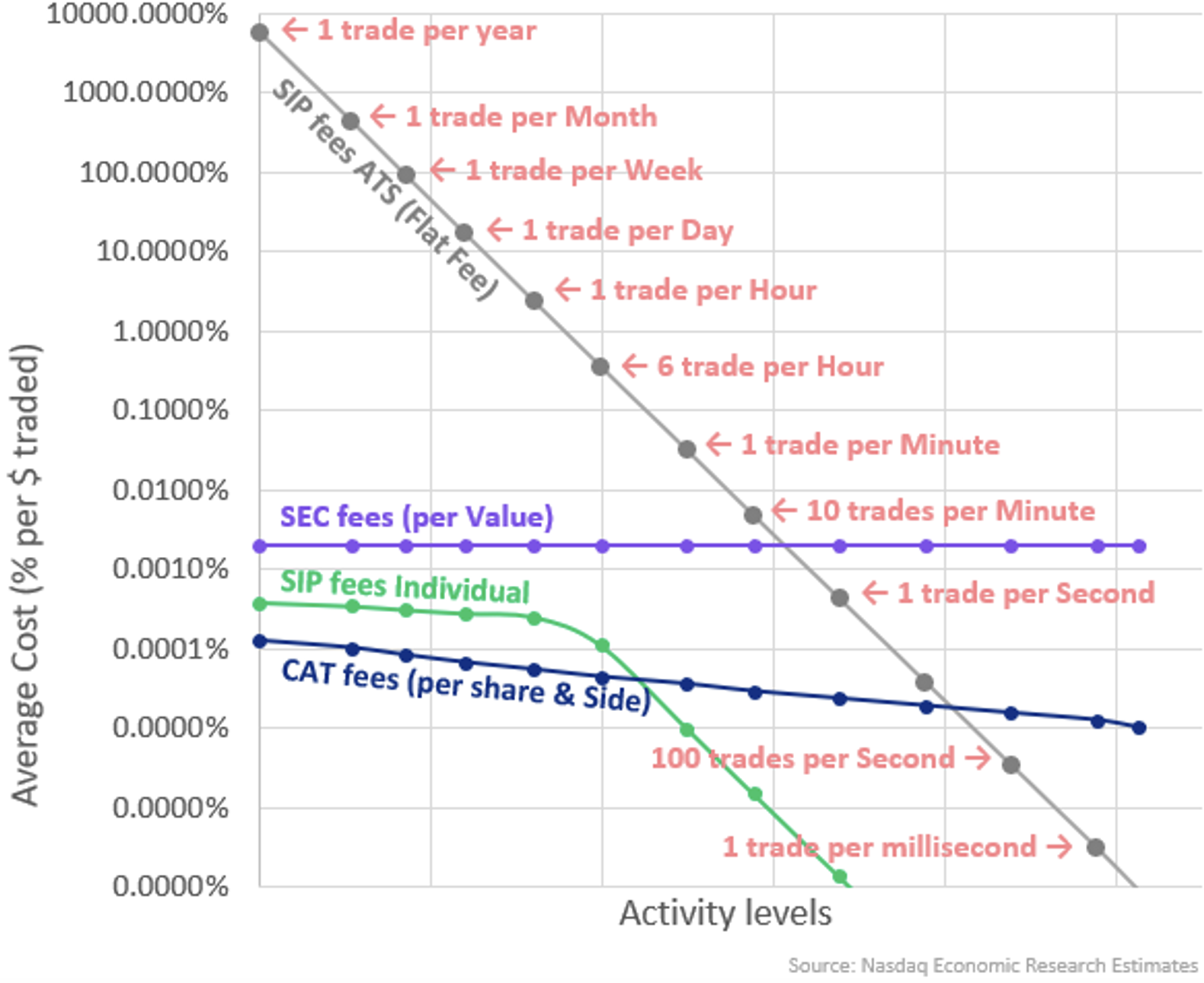

One fee that stands out is the flat ATS SIP fees. They may seem the most “equal” fees of all, with every ATS and broker algo generally paying the same amount for SIP every year. After all, each electronic broker needs to watch all prices for all securities every day, all year – regardless of how large they are.

But it also means that the average costs-per-trade declines as activity increases, which benefits brokers and dark pools that trade a lot (Chart 3).

Chart 3: Average costs to trade aren’t as equal as you think, either

Ironically,* that could make it harder for small brokers to compete with large brokers. Especially if, as Form ATS-N and research suggest, large brokers prefer their own ATSs and bundle execution costs into commissions while charging (smaller) third parties to trade. And that’s before we consider the economics of segmentation to attract orders to venues in order to increase market share.

*Given the SEC’s stated desire to level broker competition via a focus on flattening agency trading fees for exchanges.

Equal fees don’t account for how markets work

Of course, economies of scale aren’t new. Nor are they necessarily a bad thing. In many industries, they are a reality of how marketplaces work, where large customers “wholesale” products to smaller customers.

It’s also a natural outcome of how businesses manage their mix of fixed and variable costs. A company that can “outsource” high fixed costs can achieve profitability more easily on lower revenues.

Arguably, our industry, with hot-hot backup sites and data centers stacked with hardware built to withstand new record activity, has high fixed costs.

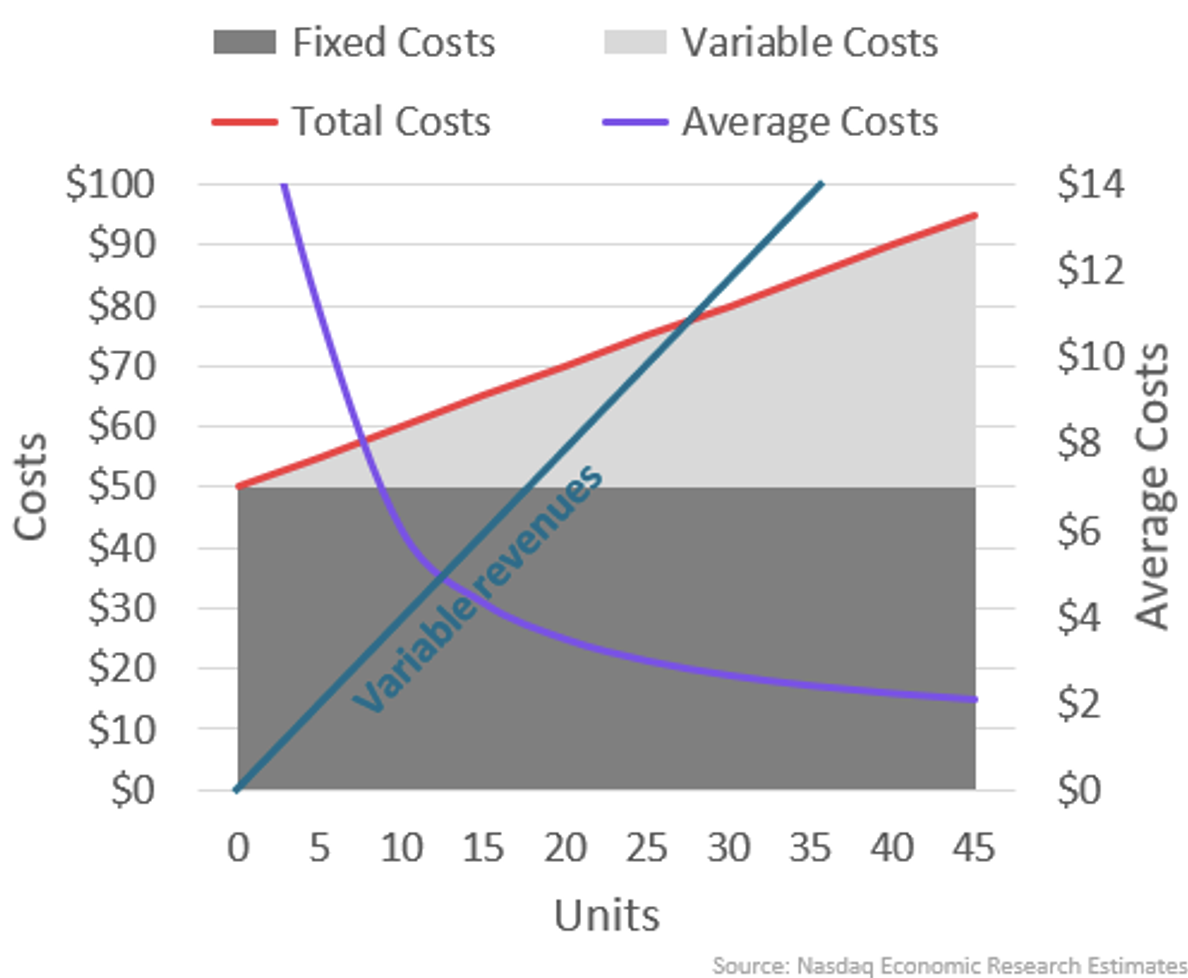

All of which makes the equal VARIABLE revenues unsuitable, and perhaps impractical, for our industry. As the stylized example in Chart 4 shows, they do a terrible job of helping cover fixed costs or appropriately adjusting for producers or customers achieving economies of scale.

Chart 4: Fixed and variable costs result in lower marginal costs at higher volumes

How our industry really works is even more complicated.

Some fixed costs depend on the level of activity and type of trading strategy being deployed.

For example, small brokers are able to use third parties for a number of services, from EMS to algos to co-location. That, in turn, reduces the amount of fixed costs they have to cover before they are profitable, even with a lower revenue base.

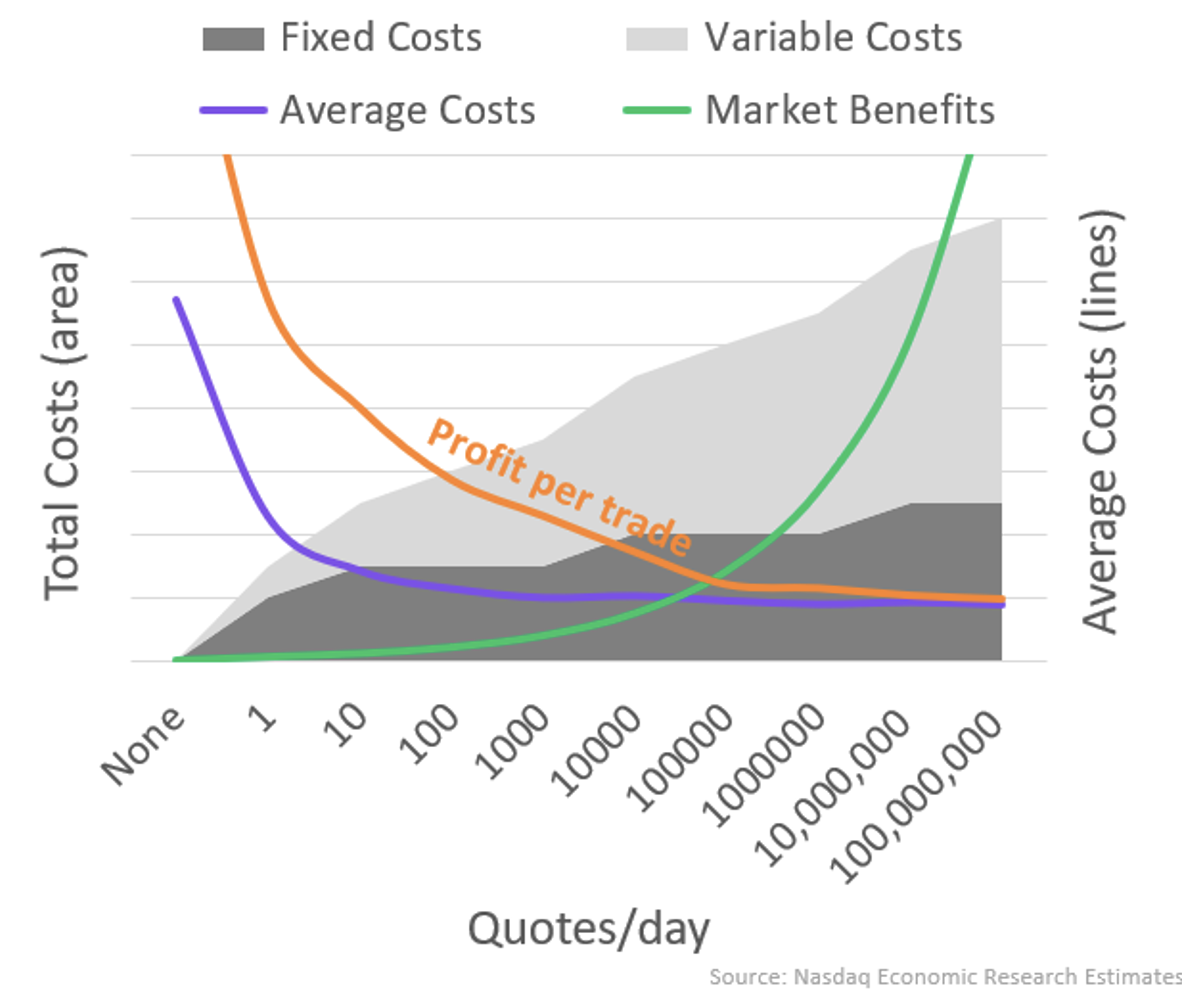

In contrast, market makers trade a lot. Our own research suggests, however, that they typically invest incrementally in hardware and bandwidth, making their “fixed costs” increase as their activity levels increase (shown as “jumps” in the fixed costs in the stylized example in Chart 5 below).

Importantly, academic research suggests that more active brokers and traders also make smaller profits per trade (orange line in Chart 5). We see this in the incredibly efficient pricing of ETFs and the selective use of inverted trading venues.

However, active traders are also more likely to improve market quality, which is important for all investors, even those trading off-exchange, by competing for spreads and providing two-sided liquidity across all 5000+ listed securities (green line in Chart 5).

In short, active traders' investments and costs are higher and their profits per trade are lower, but they are also adding the most incrementally to market quality and efficiency, also known to economists as “positive externalities.” (We show this trade-off in the stylized example in Chart 5 below.)

This seems to show that allowing active traders to generate economies of scale may benefit all traders with lower costs and more efficient markets. And that, in turn, improves how attractive U.S. markets are, adding to U.S. capital formation (another key SEC goal).

Chart 5: Fixed and variable costs result in lower marginal costs at higher volumes

Equal in the context of exchange tiers and competition

It's hard to allocate market economics effectively (and “fairly”) at the best of times. But this seems to show that “equal” fees don’t help.

Economies of scale are important to competitive markets. They also help offset the higher absolute costs of participants who trade a lot but for incrementally smaller per-trade returns. In return, active traders also mostly contribute more to positive externalities.

By keeping markets competitive and spreads tight, all investors benefit. That, in turn, encourages U.S. capital formation.

In short, when looking at trading economics, equal is far less fair than it first seems.

Latest articles

This data feed is not available at this time.

Data is currently not available